![]()

Vol 138 April 06, 2022

![]()

|

|

|

|

STATE-BY-STATE MARIJUANA LEGALIZATION UPDATE – APRIL 2022 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Even though the MORE Act was passed by the House last week, it is unlikely to clear the Senate, implying that federal legalization of cannabis is still some time away. However, state-level legalization momentum remains strong as several states are moving forward with their respective initiatives to legalize adult or medical use cannabis in 2022. Last week, the U.S. House of Representatives once again passed the MORE Act by a 220-204 vote, more than a year after it was approved in the same chamber by a 228-164 vote. After its passage by the House in December 2020, the Act failed to gain traction in the Senate in 2021. This scenario is likely to play out again this year as the Act is expected to face resistance from the Senate and Senate Majority Leader Chuck Schumer (D-NY), who plans to file his own Cannabis Administration and Opportunity Act (CAOA) bill later this month. Separately, the Senate version of the COMPETES Act – which passed last week – did not contain the SAFE banking provisions, suggesting federal legalization is unlikely to become a reality anytime soon. On the other hand, following a busy 2021, state-level legalization momentum is expected to sustain this year as well. Moreover, since 2022 is a mid-term election year, state-level momentum could receive an additional boost since mid-term years have historically resulted in an increase in the number of states that legalize cannabis, primarily due to the ability to legalize cannabis through ballot initiatives. Given this backdrop, we provide a state-by-state update on cannabis legalization initiatives that are currently underway and the potential additional sales that these states can contribute to the industry total. Adult-use legalization: 1. Ohio. OH is working toward adult-use legalization through two legislative bills and an “initiated statute” backed by advocacy group Coalition to Regulate Marijuana Like Alcohol (CTRMLA). The two bills, which aim to legalize the recreational use of marijuana in OH through the legislative route, include one from Democrats (HB382, filed in July 2021) and the other from the GOP (HB498, filed in mid-October 2021). Both bills are similar and are currently in the House for discussion. The third route, the initiated statute, will allow citizens to submit proposed laws for a statewide vote. To qualify for the November 2022 ballot, the initiated statute requires 132,887 valid signatures from registered voters. In January 2022, CTRMLA met the 132,877-signature threshold and collected an additional 29,918 signatures to put its petition before state lawmakers, who have until May 28 to either adopt, reject, or accept and amend the measure. However, OH Senate President Matt Huffman (R) said he would not bring the CTRMLA’s proposal in his chamber and if lawmakers reject it, CTRMLA will need to gather an additional 132,887 signatures to place the proposal before voters on the November 2022 ballot. 2. Rhode Island. The Ocean State is also moving toward recreational marijuana legalization. On March 9, 2021, Senate leaders Michael McCaffrey (D) and Joshua Miller (D) filed a bill that would allow adults 21 and older to purchase and possess up to one ounce of cannabis. Two days later, Gov. Dan McKee (D) came out with his own legalization proposal. Another bill to legalize marijuana was introduced by Rep. Scott Slater (D) in late May 2021. However, lawmakers and administrative officials have indicated that they want to collaborate and iron out differences as they move through the process. Before the legislative session adjourned in June 2021, Miller’s bill was approved in the Senate. After months of discussion, in March 2022, Miller and Slater introduced a comprehensive bill (S2430 and H7593 – both bills are identical but were separately pitched in the Senate and House, respectively) to legalize, regulate, and tax recreational cannabis sales in the state. Both bills are currently under discussion in their respective chambers. The legislation would legalize the sale of up to one ounce of cannabis for those age 21 and up, with no more than 10 ounces for personal use kept in a primary residence, effective October 1, 2022. 3. South Dakota. In November 2020, South Dakotans voted in favor of legalizing adult-use and medical marijuana. However, the state’s Supreme Court struck down the referendum in November 2021, citing violation of a single-subject rule. While the legalization failed to materialize in 2021, marijuana advocates are attempting to reintroduce recreational marijuana reform back to voters in 2022 through a ballot initiative, instructing the legislature to legalize it. The campaign – South Dakotans for Better Marijuana Laws (SDBML) – has collected 20,000 signatures and needs 17,000 more valid signatures until May 8 to qualify for the 2022 ballot. A recreational cannabis bill, Senate Bill 3 introduced by lawmakers, was approved in the Senate in February 2022 but failed to clear the House in early March, leaving a ballot referendum as the sole route to legalize cannabis in South Dakota. 4. Missouri. In December 2021, a group called “Legal Missouri 2022” began an initiative petition to legalize recreational marijuana in MO. The group needs to collect approximately 170,000 voter signatures by May 3 to get the measure onto the November 2022 ballot. Campaign leader John Payne is confident that residents will approve recreational use for adults as Missourians approved medical marijuana legalization with nearly 66% of the votes in 2018. Separately, adult-use legalization efforts through the legislative route are also underway. In February 2022, Ron Hicks (R) filed an omnibus legislation HB 2704, titled the “Cannabis Freedom Act”, to tax and regulate adult-use marijuana in the state. It would provide opportunities for expungements, authorize social consumption facilities, and permit cannabis businesses to claim tax deductions with the state. In late March, the House’s Public Safety Committee narrowly approved the measure and it is now headed to the Rules Committee before it could potentially advance to the floor. 5. Oklahoma. Recreational marijuana legalization is gathering momentum in the Sooner State with two competing recreational marijuana initiatives, one from Oklahomans for Responsible Cannabis Action (ORCA), filed in October 2021, and the other from New Approach PAC, filed in January 2022. Both petitions call for a 15% excise tax on adult-use marijuana sales and the existing Oklahoma Medical Marijuana Authority to regulate the adult-use and medical marijuana industry. However, a key difference between them is that ORCA’s petition would be a state constitutional amendment, which is more difficult to change, while New Approach’s petition would change the existing state law and could be amended through legislation. Because of this difference, both groups are fighting a legal battle in the state Supreme Court. If ORCA’s petition qualifies, it will appear on the ballot as State Question 819 and if New Approach’s petition qualifies, it will appear on the ballot as State Question 820. Proponents of SQ 819 are required to collect 177,957 valid signatures while SQ 820 backers need to collect only 94,910 signatures to be placed on the November ballot. 6. Maryland. After adult-use cannabis legalization efforts failed in MD last year, state lawmakers are making another attempt this year. In January 2022, MD delegate Luke Clippinger (D) filed HB 1, which is a constitutional amendment and is based on a plan first laid out by House Speaker Adrienne Jones in 2021. A month later, Clippinger filed HB 837 to serve as companion legislation to HB 1, which would refer the question of cannabis legalization to MD voters on the November 2022 ballot. If passed by a supermajority of the House of Representatives and Senate, both bills would allow voters to decide at the November 2022 general election polls on whether to legalize marijuana in the state. Both bills cleared the House of Delegates in March and are now headed to the Senate, but it is not clear if the Senate will agree on how or when to implement legalization. In addition, Sen. Brian Feldman (D) and Sen. Jill Carter (D) are sponsoring SB 833 and SB 692, respectively, with different paths toward adult-use legalization in the upper chamber. Both SB 833 and SB 692 are currently being discussed in the Senate. 7. Arkansas. The Natural State currently has three ballot initiatives to legalize adult-use marijuana. In September 2021, a marijuana activist group, Arkansas True Grass, filed an amendment on the November 2022 ballot to allow for recreational use of marijuana in AR. The group has been collecting signatures for the measure since November 2020 and had gathered more than 20,000 signatures of registered voters at the end of September 2021. A separate activist group, Arkansans for Marijuana Reform, also filed a reform initiative in November 2021 to put marijuana legalization on AR’s 2022 ballot. Aside from these two legalization ballot initiatives, former state lawmaker Eddie Armstrong also launched a campaign ‘Responsible Growth Arkansas’ in January 2022 to place cannabis legalization on AR’s 2022 ballot. While all three petitions call for the legalization of recreational marijuana, one of the key differences among them is the retail and cultivation licenses count. All three petitions are required to have 89,151 signatures to be placed onto the November ballot and the deadline to gather signatures is July 8, 2022. 8. Pennsylvania. With neighboring states NJ and NY enacting cannabis reforms in 2021, adult-use legalization momentum continues to gain momentum in PA. In October 2021, the bipartisan pair of Rep. Amen Brown (D) and Sen. Mike Regan (R) teamed up and announced their intent to reform cannabis. From early February through mid-March this year, a key Senate committee has held three public hearings on Regan’s and Brown’s cannabis plan, involving testimony from cannabis reform advocates, former regulators from other states, and industry stakeholders. The information collected at the hearings will be used to put together formal legislation that will be introduced later. On the flip side, two legalization bills – SB 473 from Shari Street (D) and Dan Laughlin (R), and HB 2050 from Jake Wheatley (D) and Dan Frankel (D) – submitted in 2H21 have not progressed and are currently in their respective chambers for discussion. If one of the three bills gets approved in both chambers, creation of an adult-use market in PA will be imminent as Gov. Tom Wolf (D) has been urging lawmakers to legalize recreational marijuana since 2020. An October 2021 survey by Franklin & Marshall College shows that 60% of PA voters back adult-use legalization. 9. New Hampshire. The Granite State is also heading toward legalizing marijuana for adult use in 2022. In late March, House lawmakers approved bill HB 1598, sponsored by Rep. Darryl Abbas (R), to legalize recreational marijuana through a state-run model. It now heads to the Senate. Notably, Gov. Chris Sununu (R), who has historically been an outspoken opponent of adult-use legalization, praised the proposal and said that the reform could be inevitable in the state and that HB 1598 is “the right bill and the right structure.” A University of New Hampshire poll released in February 2022 highlighted that more than two-thirds of NH voters support proposed legislation to legalize marijuana. 10. Minnesota. In January 2022, Gov. Tim Walz (D) called on lawmakers to pass legislation to legalize marijuana use in MN, as he proposed funds from his budget plan to launch a state authority to oversee a recreational marijuana program. He said the budget would set aside $25 million to create the new “Cannabis Management Office.” However, Senate Majority Leader Jeremy Miller (R) said that he does not “see a path” to passing legalization legislation in the Senate in the 2022 assembly session. Last year, the bill to legalize recreational marijuana passed through the House but failed in the Senate. A poll conducted by MN lawmakers last year indicated that 58% of MN residents support cannabis legalization. 11. Florida. Efforts to legalize recreational marijuana in the Sunshine State are moving slower than expected despite 76% of Florida voters supporting legalization of cannabis for adult use. Regulate Florida, the cannabis advocacy group that filed the legalization initiative for FL’s 2022 general election ballot in September 2021, has formally moved its effort to get adult-use legalization on the state’s 2024 ballot after it failed to submit the required 890,000+ signatures by February 1. The group encountered many significant roadblocks as it worked to qualify the reform initiative for this year’s ballot. For example, the state Supreme Court rejected the language of an earlier version, forcing the campaign to go back and rewrite the petitions. Medical-use legalization: 1. North Carolina. The Old North State is seeing growing optimism around medical marijuana legalization prospects. In April 2021, Chairman of the Senate Rules Committee Sen. Bill Rabon (R) – one of the highest-ranking Republicans in the NC legislature – introduced SB 711, or the Compassionate Care Act, which would legalize marijuana for medical use in the state. The Senate is expected to take up the bill during the state’s 2022 short legislative session that starts in May, but the bill already has cleared the Senate’s Judiciary, Finance, and Health Care committees. If it passes in the full Senate, it will move on to the House. A January 2021 survey by Elon shows that 73% of NC adults support the legalization of marijuana for medical purposes in the state. 2. South Carolina. SC is another state looking to legalize medical cannabis. In February 2022, state senators approved SB 150, or the Compassionate Care Act, on a 28-15 vote. It faces one more routine vote before going to the House where it has never been taken up on the floor. If the bill passes through the House and receives the governor’s approval, it would be among the strictest of the 37 other medical cannabis bills in the U.S. The bill would open access to medical cannabis only for those patients with a “debilitating medical condition.” In a February 2021 survey, 72% of SC voters supported legalizing medical marijuana. 3. Idaho. The state’s cannabis advocates have been working to bring medical cannabis reform since 2020. In 2021, there were two marijuana legalization ballot campaigns – Kind Idaho and the Personal Adult Marijuana Decriminalization Act of 2022 (PAMDA) – seeking to qualify for the 2022 ballot. However, in 2022, PAMDA decided to suspend its campaign due to complications arising from the COVID-19 pandemic and is instead focusing its efforts on the 2024 general election. On the other hand, Kind Idaho remains in the process of collecting signatures for the medical marijuana legalization initiative and has gathered about 10% of the required signatures to make the ballot. It faces a May 1 deadline to collect about 54,000 more signatures. 4. Nebraska. After a bill to legalize medical marijuana – sponsored by Sen. Anna Wishart (D) – was stalled in the 2021 legislative session, NE’s marijuana advocates – Nebraskans for Medical Marijuana (NMM) – are working on two medical cannabis legalization initiatives. Together, the initiatives will establish a system of access to medical cannabis for qualified patients. Each of the statutory petitions requires roughly 87,000 valid voter signatures and requires the campaign to collect signatures from 5% of registered voters in at least 38 of NE’s 93 counties by July 7, 2022. Wishart, a co-sponsor of the campaign, said each petition has about 25,000 signatures so far. On the other hand, a bill – LB 1275 – sponsored by Wishart that will allow marijuana for medicinal use in NE while imposing tight restrictions is receiving opposition from both legalization advocates and opponents. A November 2017 survey of Nebraska voters found that 77% of respondents would vote "yes" on a ballot question to allow medical cannabis. 5. Wisconsin. In January 2022, more than a dozen Republican lawmakers filed a bill to legalize medical marijuana in the state. The bill is fairly restrictive, as it prohibits smokable marijuana products and does not allow patients to grow cannabis for personal use. The bill is currently out for circulation, giving representatives and senators the opportunity to sign on and show their support. Gov. Tony Evers (D) tried to legalize recreational and medical marijuana through his proposed state budget in 2021, but a GOP-led legislative committee stripped the cannabis language from the legislation. Democrats tried to add the provisions back through an amendment, but Republicans blocked the move. In a March 2022 Marquette University Law School poll, 61% of Wisconsin voters favored marijuana legalization, compared to 31% who wanted to keep marijuana illegal. 6. Kansas. State lawmakers are on the verge of legalizing marijuana for medical use this year, but with stricter rules vs. the way cannabis has been cleared for use in other states. In March 2022, Sen. Robert Olson (R) introduced a new medical cannabis bill SB 560, or the “Medical Marijuana Regulation Act” in the Senate, after separate House-passed legislation stalled in the Senate earlier in 2022. The bill would provide patients diagnosed with a series of medical conditions with access to limited forms of cannabis. KS senators began a series of three planned committee hearings in mid-March to discuss the key provisions of the bill and take testimony from advocates and stakeholders. The bill sets several milestones for establishing the rules and regulations needed to make the program operational. If the measure passes and all those deadlines are met in 2022, medical marijuana would be available in KS by January 2024. 7. Kentucky. Efforts to legalize medical marijuana in the Bluegrass State appear to have hit a dead end in 2022. HB 136, sponsored by Rep. Jason Nemes (R), passed the House in mid-March by a 59-34 vote, moving over to the Senate. However, the Senate brought it up for a vote at the end of March and the state’s 2022 legislative session is scheduled to adjourn on April 14. Senate Majority Leader Damon Thayer said that the bill is “done for the year” because of a lack of support. The same thing happened in 2020, when the House passed a medical marijuana legalization bill, but the Senate declined to take it up. HB 136 would allow medical professionals to prescribe marijuana for qualifying conditions, including any type of cancer, chronic pain, epilepsy, multiple sclerosis, and nausea. 8. Wyoming. Wyomingites will have to wait until 2023 or 2024 to see medical marijuana legalized in the Cowboy State. In August 2021, cannabis activists placed two separate measures to legalize medical cannabis and decriminalize adult-use marijuana before voters on the November 2022 ballot. They faced several challenges, however, including delayed approval of the petitions by the state, and announced that they would not be able to submit the required number of signatures in time for the February deadline. Instead, activists will turn their attention toward qualifying their measures for the 2024 ballot while also focusing on reform through the state legislature in the meantime. A University of Wyoming survey in December 2020 found that 85% of voters support medical marijuana legalization and more than half back full legalization.

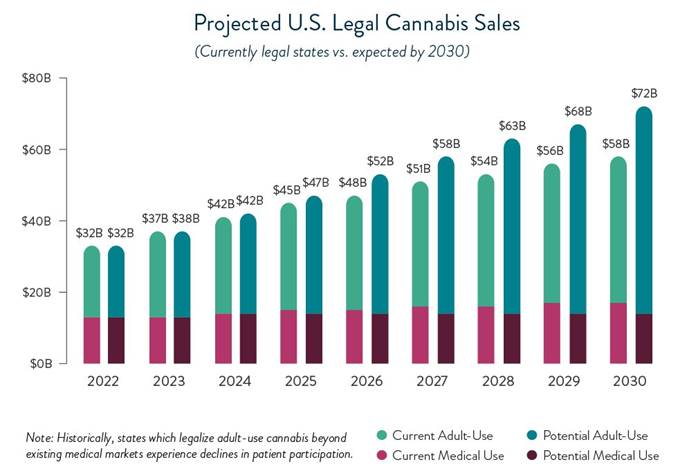

Source: Intro-act, MultiState’s Legislative Session Dates, Ballotpedia If the above states legalize marijuana for adult or medicinal use in the near future, it will add $14 billion to the estimated $58 billion legal cannabis industry in the U.S. by 2030, per New Frontier Data. Without taking into account any new states that may legalize cannabis for medicinal or adult use by 2030, total legal cannabis sales in the U.S. are expected to grow at an 11% CAGR, surpassing $58 billion by 2030. However, should the 18 states – nine potential medical states (ID, NE, KS, TX, WI, KY, GA, SC, and NC) and nine potential adult-use markets (SD, OK, MO, OH, FL, PA, RI, NH, and MD) – successfully pass cannabis legalization measures, legal sales in the U.S. are expected to expand at a 14% CAGR to $72 billion by 2030.

Source: Intro-act, New Frontier Data |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

CANNA EVENTS CALENDAR

|

Chart 26: Cannabis Company Events Calendar – Upcoming Conference Calls |

||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, New Cannabis Ventures

|

Chart 27: Cannabis Company Events Calendar – Recent Conference Calls |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, New Cannabis Ventures

|

Chart 28: Cannabis IPO Pipeline |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, New Cannabis Ventures

|

Chart 29: Cannabis SPAC Pipeline |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, New Cannabis Ventures

|

Chart 30: Cannabis Industry Events Calendar |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Cannabis Business Times

COMPARABLES & COMPANY PROFILE LINKS

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

4/4/2022 |

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

Peer Set |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Canadian LP - Cultivation, Processing (and Dispensing) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

1 |

TLRY |

7.45 |

3,581 |

4,086 |

217% |

-36% |

6% |

431 |

675 |

6.0 x |

27 |

65 |

62.9 x |

9.57 |

0.8 x |

||

|

2 |

CGC |

7.77 |

3,059 |

3,290 |

326% |

-28% |

-11% |

449 |

457 |

7.2 x |

(312) |

(166) |

- |

8.31 |

0.9 x |

||

|

3 |

ACB |

4.14 |

889 |

913 |

157% |

-30% |

-23% |

185 |

184 |

5.0 x |

(52) |

(13) |

- |

7.80 |

0.5 x |

||

|

4 |

CRON |

3.92 |

1,470 |

472 |

152% |

-25% |

0% |

74 |

123 |

3.8 x |

(162) |

(116) |

- |

3.57 |

1.1 x |

||

|

5 |

HEXO |

0.61 |

245 |

421 |

1146% |

-24% |

-13% |

131 |

181 |

2.3 x |

(33) |

2 |

249.9 x |

0.96 |

0.6 x |

||

|

6 |

SNDL |

0.67 |

1,383 |

345 |

122% |

-40% |

70% |

38 |

339 |

1.0 x |

6 |

31 |

11.1 x |

0.53 |

1.3 x |

||

|

7 |

OGI |

1.73 |

538 |

413 |

107% |

-27% |

-1% |

72 |

116 |

3.5 x |

(21) |

(1) |

- |

1.25 |

1.4 x |

||

|

8 |

CBWTF |

0.13 |

116 |

173 |

165% |

-22% |

-7% |

84 |

145 |

1.2 x |

(14) |

(1) |

- |

0.22 |

0.6 x |

||

|

9 |

CNTMF |

0.33 |

73 |

125 |

304% |

-11% |

-50% |

62 |

112 |

1.1 x |

17 |

33 |

3.8 x |

0.26 |

1.3 x |

||

|

10 |

FLGC |

1.88 |

121 |

102 |

1041% |

-30% |

6% |

12 |

54 |

1.9 x |

(3) |

6 |

17.3 x |

0.58 |

3.3 x |

||

|

11 |

ALEAF |

0.09 |

30 |

67 |

500% |

-44% |

-11% |

36 |

61 |

1.1 x |

(23) |

(6) |

- |

0.03 |

2.7 x |

||

|

12 |

ROMJF |

0.95 |

53 |

51 |

198% |

-5% |

-37% |

21 |

40 |

1.3 x |

(11) |

2 |

34.3 x |

0.56 |

1.7 x |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

|

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

13 |

ETRGF |

0.07 |

20 |

72 |

382% |

-25% |

1% |

37 |

(45) |

0.18 |

0.4 x |

||||||

|

14 |

TGODF |

0.10 |

78 |

89 |

289% |

-33% |

39% |

39 |

45 |

2.0 x |

(20) |

(13) |

- |

0.18 |

0.6 x |

||

|

15 |

ETRGF |

0.07 |

20 |

72 |

382% |

-25% |

1% |

37 |

(45) |

0.18 |

0.4 x |

||||||

|

16 |

FLWPF |

0.06 |

25 |

66 |

367% |

-37% |

36% |

10 |

18 |

3.6 x |

(20) |

(13) |

- |

0.17 |

0.3 x |

||

|

17 |

VVCIF |

0.06 |

23 |

17 |

130% |

-25% |

6% |

0.31 |

0.2 x |

||||||||

|

18 |

REZN-CA |

0.01 |

2 |

2 |

930% |

-52% |

-32% |

0.01 |

1.0 x |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

US - Cultivation, Processing (and Dispensing) - MSO & SSO |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

19 |

CURLF |

7.12 |

4,379 |

5,626 |

123% |

-25% |

-21% |

1,210 |

1,458 |

3.9 x |

298 |

398 |

14.1 x |

2.38 |

3.0 x |

||

|

20 |

GTBIF |

18.97 |

3,856 |

4,670 |

85% |

-22% |

-14% |

894 |

1,073 |

4.4 x |

308 |

354 |

13.2 x |

6.92 |

2.7 x |

||

|

21 |

TCNNF |

20.62 |

2,651 |

3,848 |

130% |

-18% |

-21% |

938 |

1,356 |

2.8 x |

385 |

479 |

8.0 x |

6.35 |

3.2 x |

||

|

22 |

VRNOF |

9.84 |

1,984 |

3,263 |

114% |

-10% |

-22% |

636 |

966 |

3.4 x |

296 |

434 |

7.5 x |

5.39 |

1.8 x |

||

|

23 |

CRLBF |

6.10 |

1,543 |

2,482 |

124% |

-15% |

-9% |

822 |

948 |

2.6 x |

194 |

263 |

9.5 x |

1.98 |

3.1 x |

||

|

24 |

CCHWF |

2.93 |

1,086 |

1,338 |

137% |

-17% |

2% |

474 |

643 |

2.1 x |

78 |

131 |

10.2 x |

1.87 |

1.6 x |

||

|

25 |

AYRWF |

12.73 |

709 |

1,179 |

150% |

-13% |

-16% |

358 |

622 |

1.9 x |

98 |

178 |

6.6 x |

15.26 |

0.8 x |

||

|

26 |

TRSSF |

5.85 |

1,473 |

1,616 |

105% |

-22% |

-4% |

210 |

411 |

3.9 x |

69 |

115 |

14.1 x |

1.17 |

5.0 x |

||

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

|

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

27 |

AAWH |

4.01 |

695 |

991 |

294% |

-8% |

-38% |

332 |

429 |

2.3 x |

80 |

108 |

9.2 x |

1.07 |

3.8 x |

||

|

28 |

VFF |

5.50 |

486 |

520 |

158% |

-24% |

-14% |

268 |

325 |

1.6 x |

14 |

27 |

19.5 x |

4.63 |

1.2 x |

||

|

29 |

FFNTF |

0.75 |

468 |

571 |

93% |

-25% |

-26% |

133 |

143 |

4.0 x |

34 |

40 |

14.3 x |

0.09 |

8.6 x |

||

|

30 |

GDNSF |

2.10 |

174 |

363 |

33% |

-43% |

23% |

54 |

99 |

3.7 x |

(9) |

14 |

26.9 x |

0.34 |

6.3 x |

||

|

30 |

ACRHF |

1.67 |

125 |

286 |

276% |

-30% |

-1% |

2.63 |

0.6 x |

||||||||

|

31 |

RWBYF |

0.29 |

64 |

284 |

338% |

-14% |

-14% |

107 |

0.47 |

0.6 x |

|||||||

|

31 |

MRMD |

0.75 |

251 |

282 |

60% |

-47% |

-13% |

138 |

2.0 x |

45 |

6.2 x |

0.11 |

6.6 x |

||||

|

32 |

ITHUF |

0.13 |

22 |

234 |

230% |

-31% |

34% |

(0.13) |

-1.0 x |

||||||||

|

33 |

UNRV |

0.19 |

85 |

166 |

134% |

-26% |

-28% |

0.31 |

0.6 x |

||||||||

|

34 |

GRAMF |

1.21 |

117 |

119 |

602% |

-17% |

-14% |

173 |

189 |

0.6 x |

(65) |

(69) |

- |

0.18 |

6.9 x |

||

|

35 |

FLOOF |

0.05 |

21 |

106 |

564% |

-56% |

44% |

70 |

82 |

1.3 x |

(90) |

(7) |

- |

0.01 |

7.8 x |

||

|

36 |

DBCCF |

0.09 |

35 |

63 |

243% |

-19% |

-12% |

50 |

77 |

0.8 x |

6 |

14 |

4.6 x |

0.10 |

0.9 x |

||

|

37 |

BMMJ |

0.21 |

24 |

32 |

186% |

-21% |

-33% |

0.29 |

0.7 x |

||||||||

|

38 |

YOURF |

0.13 |

35 |

32 |

150% |

-38% |

-5% |

30 |

110 |

0.3 x |

4 |

12 |

2.7 x |

0.06 |

2.1 x |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

|

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

Medical Cannabis |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

39 |

JAZZ |

160.73 |

9,923 |

15,491 |

18% |

-27% |

26% |

3,094 |

3,585 |

4.3 x |

1,353 |

1,592 |

9.7 x |

64.34 |

2.5 x |

||

|

40 |

ARNA |

99.99 |

4,982 |

|

0% |

-54% |

-13% |

0 |

0 |

10.94 |

9.1 x |

||||||

|

41 |

CARA |

12.56 |

672 |

509 |

136% |

-23% |

3% |

23 |

60 |

8.4 x |

(89) |

(80) |

- |

4.25 |

3.0 x |

||

|

42 |

IHL-ASX |

0.38 |

466 |

451 |

44% |

-60% |

-15% |

0.01 |

31.8 x |

||||||||

|

43 |

DOCRF |

0.67 |

195 |

180 |

181% |

-29% |

-28% |

55 |

140 |

1.3 x |

(2) |

(1) |

- |

0.73 |

0.9 x |

||

|

44 |

COPHF |

0.07 |

88 |

83 |

195% |

-66% |

23% |

0.02 |

4.1 x |

||||||||

|

45 |

MJNA |

0.03 |

97 |

97 |

177% |

-100% |

37% |

0.02 |

1.2 x |

||||||||

|

46 |

EMD-ASX |

0.25 |

67 |

62 |

47% |

-50% |

-12% |

0.03 |

9.1 x |

||||||||

|

47 |

XPHYF |

0.68 |

53 |

55 |

240% |

-32% |

-21% |

0.04 |

16.9 x |

||||||||

|

48 |

SOLCF |

1.32 |

69 |

46 |

203% |

-20% |

-44% |

6.25 |

0.2 x |

||||||||

|

49 |

CRDL |

1.51 |

94 |

27 |

228% |

-19% |

-18% |

0 |

0.97 |

1.5 x |

|||||||

|

50 |

AQSZF |

0.06 |

8 |

8 |

199% |

-23% |

-29% |

0.01 |

5.2 x |

||||||||

|

51 |

CRBP |

0.51 |

64 |

(7) |

345% |

-42% |

-16% |

1 |

1 |

-10.3 x |

0.55 |

0.9 x |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

|

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

CBD/Hemp |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

52 |

CWBHF |

1.10 |

160 |

167 |

344% |

-29% |

8% |

96 |

109 |

1.5 x |

(16) |

(10) |

- |

0.90 |

1.2 x |

||

|

53 |

GRVI |

5.64 |

93 |

88 |

66% |

-32% |

40% |

1.80 |

3.1 x |

||||||||

|

54 |

EPWCF |

0.16 |

56 |

56 |

296% |

-8% |

-32% |

0.01 |

15.2 x |

||||||||

|

55 |

BTTR |

2.54 |

74 |

56 |

283% |

-17% |

-21% |

46 |

63 |

0.9 x |

(8) |

(6) |

- |

1.99 |

1.3 x |

||

|

56 |

YCBD |

1.05 |

62 |

47 |

302% |

-33% |

-3% |

41 |

1.45 |

0.7 x |

|||||||

|

57 |

OCTHF |

0.03 |

33 |

17 |

635% |

-41% |

-83% |

0.02 |

2.0 x |

||||||||

|

58 |

CVSI |

0.12 |

16 |

15 |

311% |

-19% |

6% |

20 |

24 |

0.6 x |

(9) |

(5) |

- |

0.10 |

1.2 x |

||

|

59 |

CBDHF |

0.11 |

19 |

14 |

1660% |

-39% |

-21% |

0.14 |

0.8 x |

||||||||

|

60 |

IWINF |

2.94 |

4 |

11 |

70% |

-66% |

-7% |

0.04 |

71.0 x |

||||||||

|

Downstream - Distribution/Brand/Marketing/Retail/Delivery |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

61 |

TPB |

33.20 |

607 |

911 |

65% |

-13% |

-12% |

445 |

452 |

2.0 x |

108 |

107 |

8.5 x |

7.14 |

4.6 x |

||

|

62 |

PLNHF |

2.52 |

555 |

517 |

192% |

-25% |

-15% |

120 |

146 |

3.5 x |

18 |

31 |

16.5 x |

0.87 |

2.9 x |

||

|

63 |

LQSIF |

7.26 |

263 |

458 |

11% |

-36% |

32% |

726 |

3.69 |

2.0 x |

|||||||

|

64 |

HITI |

4.74 |

288 |

331 |

131% |

-23% |

12% |

215 |

370 |

0.9 x |

11 |

21 |

16.0 x |

2.31 |

2.1 x |

||

|

65 |

NBEV |

0.53 |

78 |

85 |

463% |

-4% |

-49% |

449 |

457 |

0.2 x |

(6) |

13 |

6.3 x |

1.51 |

0.3 x |

||

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

|

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

66 |

FFLWD |

4.41 |

163 |

192 |

136% |

-28% |

12% |

176 |

206 |

0.9 x |

9 |

8 |

23.8 x |

29.16 |

0.2 x |

||

|

67 |

MMNFF |

0.14 |

171 |

123 |

211% |

-34% |

-14% |

0.20 |

0.7 x |

||||||||

|

68 |

GNLN |

0.52 |

48 |

81 |

1132% |

-23% |

-46% |

166 |

221 |

0.4 x |

(22) |

(7) |

- |

2.18 |

0.2 x |

||

|

69 |

SLGWF |

0.22 |

16 |

25 |

864% |

-38% |

-37% |

41 |

0.64 |

0.4 x |

|||||||

|

70 |

DLTNF |

0.26 |

27 |

58 |

100% |

-24% |

11% |

62 |

0.21 |

1.2 x |

|||||||

|

71 |

CHALF |

0.32 |

20 |

30 |

398% |

-84% |

23% |

0.28 |

1.2 x |

||||||||

|

Extraction, Genetics, Canna Science, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

72 |

XXII |

2.38 |

388 |

341 |

155% |

-22% |

-23% |

31 |

38 |

9.0 x |

(31) |

- |

0.41 |

5.9 x |

|||

|

73 |

VLNS |

1.62 |

106 |

110 |

513% |

-1% |

-34% |

78 |

119 |

0.9 x |

(27) |

(34) |

- |

2.98 |

0.5 x |

||

|

74 |

CNVCF |

0.28 |

127 |

126 |

79% |

-46% |

-22% |

0.01 |

32.8 x |

||||||||

|

75 |

NEPT |

0.21 |

36 |

55 |

638% |

-7% |

-48% |

42 |

71 |

0.8 x |

(53) |

(16) |

- |

0.47 |

0.5 x |

||

|

76 |

HCANF |

0.27 |

8 |

25 |

3929% |

-6% |

-72% |

4.29 |

0.1 x |

||||||||

|

77 |

NWVCF |

0.73 |

80 |

75 |

81% |

-14% |

-5% |

25 |

41 |

1.8 x |

(1) |

4 |

20.6 x |

0.16 |

4.5 x |

||

|

78 |

APDN |

2.12 |

16 |

13 |

370% |

-5% |

-47% |

12 |

13 |

1.0 x |

1.12 |

1.9 x |

|||||

|

79 |

MEDIF |

0.14 |

38 |

12 |

238% |

-29% |

-4% |

22 |

30 |

0.4 x |

(23) |

(14) |

- |

0.31 |

0.5 x |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

|

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

Input Materials - Nutrients, Hydroponic Equipment, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

80 |

SMG |

128.97 |

7,169 |

10,698 |

97% |

-14% |

-20% |

4,742 |

4,746 |

2.3 x |

807 |

822 |

13.0 x |

15.12 |

8.5 x |

||

|

81 |

HYFM |

15.69 |

702 |

1,618 |

352% |

-20% |

-45% |

479 |

579 |

2.8 x |

47 |

63 |

25.7 x |

(3.18) |

-4.9 x |

||

|

82 |

GRWG |

9.66 |

586 |

551 |

491% |

-30% |

-26% |

423 |

426 |

1.3 x |

34 |

30 |

18.6 x |

6.20 |

1.6 x |

||

|

83 |

MBII |

1.07 |

195 |

213 |

95% |

-49% |

49% |

44 |

56 |

3.8 x |

(9) |

(3) |

- |

0.16 |

6.6 x |

||

|

84 |

MARY-CA |

0.14 |

6 |

5 |

588% |

-18% |

-39% |

0.03 |

4.6 x |

||||||||

|

Testing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

85 |

PMD |

7.04 |

39 |

42 |

26% |

-12% |

0% |

2.19 |

3.2 x |

||||||||

|

86 |

EVIO |

0.00 |

0 |

13 |

1700% |

-75% |

-60% |

(0.00) |

-0.1 x |

||||||||

|

87 |

FLURF |

0.04 |

5 |

1 |

954% |

-21% |

28% |

0.05 |

0.7 x |

||||||||

|

Technology, Ancillary Products and Services |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

88 |

MAPS |

8.12 |

572 |

617 |

174% |

-48% |

36% |

193 |

258 |

2.4 x |

32 |

16 |

38.0 x |

0.97 |

8.4 x |

||

|

89 |

SLHG |

1.19 |

47 |

57 |

484% |

-40% |

-10% |

38 |

39 |

1.5 x |

(11) |

(13) |

- |

0.71 |

1.7 x |

||

|

90 |

KERN |

1.11 |

34 |

40 |

405% |

-14% |

-37% |

21 |

27 |

1.5 x |

(13) |

(11) |

- |

2.26 |

0.5 x |

||

|

91 |

NEXCF |

0.75 |

75 |

70 |

392% |

-9% |

-26% |

21 |

18 |

4.0 x |

(10) |

- |

0.21 |

3.6 x |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

|

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

92 |

AGFY |

4.46 |

111 |

57 |

706% |

-17% |

-52% |

60 |

140 |

0.4 x |

(20) |

(18) |

- |

6.32 |

0.7 x |

||

|

93 |

FORA |

6.28 |

200 |

189 |

129% |

-11% |

-30% |

0.79 |

7.9 x |

||||||||

|

94 |

UGRO |

10.62 |

114 |

80 |

63% |

-36% |

1% |

62 |

111 |

0.7 x |

5 |

15.6 x |

4.49 |

2.4 x |

|||

|

95 |

VEXTF |

0.47 |

32 |

67 |

82% |

-22% |

-7% |

43 |

1.6 x |

15 |

4.4 x |

0.42 |

1.1 x |

||||

|

96 |

BLOZF |

0.50 |

57 |

49 |

162% |

-22% |

19% |

0.07 |

7.2 x |

||||||||

|

97 |

AUSAF |

0.09 |

25 |

29 |

287% |

-14% |

-37% |

0.16 |

0.5 x |

||||||||

|

Real Estate & Investors |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

98 |

IIPR |

205.24 |

5,285 |

5,215 |

40% |

-21% |

-22% |

205 |

278 |

18.7 x |

256 |

20.4 x |

62.38 |

3.3 x |

|||

|

99 |

CODI |

24.44 |

1,697 |

3,431 |

36% |

-11% |

-20% |

1,992 |

2,072 |

1.7 x |

361 |

387 |

8.9 x |

11.75 |

2.1 x |

||

|

100 |

AFCG |

19.30 |

381 |

443 |

32% |

-6% |

-15% |

38 |

72 |

6.2 x |

72 |

6.1 x |

16.61 |

1.2 x |

|||

|

101 |

POWER REIT |

PW |

37.61 |

125 |

147 |

118% |

-7% |

-45% |

8 |

12 |

12.3 x |

15.79 |

2.4 x |

||||

|

102 |

CNPOF |

1.19 |

170 |

(74) |

68% |

-24% |

4% |

1.93 |

0.6 x |

||||||||

|

103 |

SILVER SPIKE INVESTMENT CORP |

SSIC |

13.50 |

121 |

145 |

14% |

-11% |

7 |

21.4 x |

(0.06) |

-233.0 x |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

|

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

SPACs |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

104 |

SPKC.USD-CA |

|

|

|

(0.58) |

||||||||||||

|

105 |

SPKBU |

9.97 |

287 |

|

5% |

-3% |

0% |

|

|||||||||

|

106 |

CERAF |

9.82 |

118 |

27 |

15% |

-10% |

0% |

(0.22) |

-44.3 x |

||||||||

|

107 |

GNRSU |

3.93 |

69 |

69 |

239% |

0% |

-3% |

|

|||||||||

|

108 |

TUSCAN HOLDINGS CORP. II |

THCAU |

11.96 |

263 |

263 |

6% |

-26% |

15% |

|

||||||||

|

109 |

TCACU |

10.01 |

200 |

200 |

5% |

-9% |

-1% |

|

|||||||||

|

110 |

CHOICE CONSOLIDATION CORP |

CDXXF |

|

|

|

|

|||||||||||

|

111 |

MCMJ |

8.45 |

349 |

349 |

37% |

-38% |

-15% |

53 |

6.6 x |

(31) |

- |

7.49 |

1.1 x |

||||

|

112 |

ACKIU |

10.50 |

145 |

145 |

8% |

-22% |

1% |

|

|||||||||

|

113 |

BGPPF |

9.66 |

1,111 |

33 |

935% |

-100% |

4% |

2.15 |

4.5 x |

||||||||

|

114 |

CANNA-GLOBAL ACQUISITION CORP |

CNGLU |

10.11 |

233 |

|

11% |

-6% |

-4% |

|

||||||||

|

115 |

CLOEU |

10.28 |

142 |

|

19% |

-13% |

-1% |

|

|||||||||

|

116 |

NORTHERN LIGHTS ACQUISITION CORP. |

NLITU |

10.20 |

123 |

|

12% |

-3% |

0% |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share Price |

Mkt Cap (Mns) |

Ent Val (Mns) |

Price Performance |

Sales |

EBITDA |

Book Value |

||||||||

|

|

|

|

% to High |

% to Low |

% YTD |

LTM |

NTM |

EV/Sales |

LTM |

NTM |

EV/ EBITDA |

Book/ Share |

P/ |

||||

|

Diversified |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

117 |

MO |

52.72 |

95,806 |

119,306 |

2% |

-19% |

11% |

21,111 |

21,036 |

5.7 x |

11,832 |

12,363 |

9.7 x |

(0.88) |

-59.8 x |

||

|

118 |

STZ |

229.71 |

37,750 |

53,356 |

12% |

-10% |

-8% |

8,671 |

9,223 |

5.8 x |

3,158 |

3,423 |

15.6 x |

60.03 |

3.8 x |

||

|

119 |

INCR-TAE |

7.08 |

319 |

285 |

31% |

-21% |

6% |

3.16 |

2.2 x |

||||||||

|

120 |

TLLTF |

0.28 |

92 |

190 |

110% |

-39% |

24% |

203 |

258 |

0.7 x |

22 |

29 |

6.6 x |

0.73 |

0.4 x |

||

|

121 |

CLVR |

2.26 |

67 |

55 |

449% |

-60% |

-18% |

15 |

23 |

2.4 x |

(25) |

(22) |

- |

2.74 |

0.8 x |

||

|

122 |

SHWZ |

2.11 |

97 |

139 |

40% |

-40% |

19% |

108 |

162 |

0.9 x |

42 |

3.3 x |

2.65 |

0.8 x |

|||

|

123 |

LOWLF |

0.38 |

38 |

72 |

314% |

-40% |

19% |

67 |

84 |

0.9 x |

(16) |

1 |

52.4 x |

0.72 |

0.5 x |

||

|

124 |

PCLOF |

0.56 |

77 |

75 |

177% |

-5% |

-27% |

2 |

0.12 |

4.6 x |

|||||||

|

125 |

KHRNF |

0.20 |

36 |

25 |

137% |

-38% |

24% |

12 |

20 |

1.3 x |

(16) |

(10) |

- |

0.24 |

0.8 x |

||

Important Disclosures

Analyst Certification: I, Peter Wright, certify that the views expressed in the research report accurately reflect my personal views about the subject securities or issues. I also do not receive direct or indirect compensation based on my recommendations or views. Intro-act, Inc. (Intro-act) issued this report and may seek fees for the assistance with investor targeting, access, and further investor preparation services. Intro-act, Inc. will not seek renumeration for any investment banking service or investment advice.

Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources who are believed to be reliable. However, the issuer and related parties, as well as Intro-act, do not guarantee the accuracy or completeness of this report, and have not sought for this information to be independently verified. Opinions contained in this report represent those of the Intro-act analysts at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, and estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties, and other factors that may cause the actual results, performance, or achievements of their subject matter to be materially different from current expectations.

Exclusion of Liability: To the fullest extent allowed by law, Intro-act, Inc. shall not be liable for any direct, indirect, or consequential losses, loss of profits, damages, or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this note.

No personalized advice: The information that we provide should not be construed in any manner whatsoever as personalized advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Intro-act’s solicitation to affect, or attempt to affect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors.

Investment in securities mentioned: Intro-act has a restrictive policy relating to personal dealing and conflicts of interest. Intro-act, Inc. does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees, and contractors of Intro-act may have a position in any or related securities mentioned in this report, subject to Intro-act’s policies on personal dealing and conflicts of interest.

Copyright: Copyright 2022 Intro-act, Inc. (Intro-act).

Intro-act is not registered as an investment adviser with the Securities and Exchange Commission. Intro-act relies upon the “publishers’ exclusion” from the definition of investment adviser under Section 202(a) (11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Intro-act does not offer or provide personal advice, and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell, or hold that or any security, or that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.