![]()

Vol 22 December 2, 2022

![]()

DEAL IN FOCUS: OCEAN BIOMEDICAL, INC. - AESTHER HEALTHCARE ACQUISITION CORP. (AEHA)

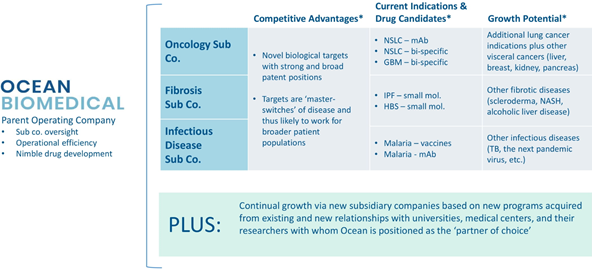

Ocean Biomedical, Inc. is a biopharma company with an innovative business model that accelerates the development and commercialization of scientifically compelling assets from research universities and medical centers. Ocean Biomedical deploys funding and expertise to move new therapeutic candidates efficiently from the laboratory to the clinic, and to the world. The company is currently pursuing programs in oncology, fibrosis, infectious disease, and inflammation. Its programs in oncology and fibrosis are based on exclusive licenses with Brown University. Its programs in infectious disease are based on exclusive licenses with Rhode Island Hospital. The company was co-founded by Dr. Chirinjeev Kathuria MD, an investor, physician, and entrepreneur who is a graduate of Brown University's Alpert School of Medicine, and Stanford University's Graduate School of Business. Around its core scientists and CEO, Ocean Biomedical has gathered a world-class biopharma management team to guide discoveries through clinical testing and continue building its diverse portfolio into adjacent diseases with similar biological pathways.

|

Chart 1: Ocean Biomedical at a Glance |

|

|

Source: Intro-act, Ocean Biomedical Investor Presentation. *Based on Ocean Biomedical's business plans, market analyses, and data from peer-reviewed and published in-vitro and in-vivo studies

|

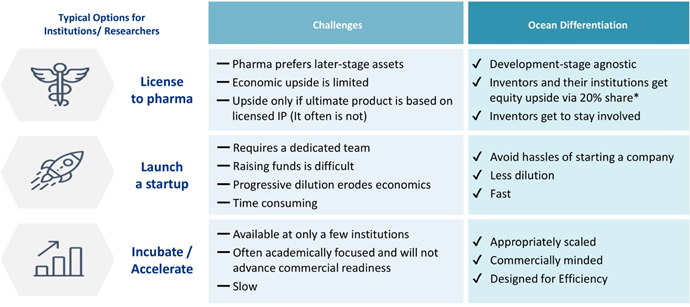

Chart 2: Ocean Biomedical Is Designed to Be The 'Partner of Choice' For Universities, Medical Centers, And Researchers |

|

|

Source: Intro-act, Ocean Biomedical Investor Presentation. *Applies to designated future subsidiaries dedicated to specific programs to be in-licensed

The company's main programs in oncology, fibrosis, and infectious diseases are all nearing IND applications.

n Oncology ' Ocean Biomedical's novel target in oncology is Chitinase 3-Like1 (CHI3L1), a key regulator of many visceral tumors regardless of the genetic mutations that drive them. Ocean's proprietary mono-specific and bispecific antibodies are the first to target CHI3L1. The efficacy proof of concept is an 85-95% reduction in primary and metastatic tumor burden in multiple animal models in the absence of adverse effects.

- Needs addressed: 1) Non-Small Cell Lung Cancer (NSCLC) is the leading cause of cancer death and second most diagnosed cancer in the US. NSCLC affects approximately 460,000 people in the U.S. and accounts for about 85% of new lung cancers. NSCLC continues to rank among the cancers with the lowest 5-year survival rates. Early diagnosis is essential, as 40%-50% of patients are diagnosed with Stage IV disease. 2) Glioblastoma multiforme (GBM) is a lethal type of brain tumor that affects approximately 28,000 people in the U.S. The median survival time is about 15 months, and 5-year survival is just 8% for those aged 45-54 and 5% for those aged 55-64.

n Fibrosis ' Ocean Biomedical's small molecule candidate in fibrosis addresses a novel target, Chitanse 1 (Chit1), a key regulator of tissue damage and remodeling, and has the potential to be disease-modifying. The small molecule candidate has demonstrated an 85-90% reduction in collagen accumulation in 4 animal models of pulmonary fibrosis.

- Needs addressed: 1) Idiopathic Pulmonary Fibrosis (IPF) is a progressive disease that results in irreversible loss of lung function, with high morbidity and mortality rates. IPF prevalence in the US has been reported to range from 10 to 60 cases per 100,000 while in Europe it ranges from 1.3 to 32.5 cases per 100,000 people. 2) Hermanksy-Pudlak Syndrome (HPS) is a rare, genetic disease. Symptoms are severe including highly penetrable pulmonary fibrosis, oculocutaneous albinism, and bleeding due to platelet dysfunction, and colitis.

n Infectious Diseases ' Ocean Biomedical's vaccine and therapeutic candidates use a groundbreaking approach to target Malaria, one of the world's most intractable diseases. Malaria is caused by parasites and transmitted through the bites of infected mosquitoes. The deadliest of these parasites is Plasmodium falciparum, and Ocean Biomedical's vaccine and therapeutic candidates target PfGARP and PfSEA-1 - novel targets discovered by Scientific Co-Founder Dr. Jake Kurtis - that are critical for this parasite's survival.

- Needs addressed: Malaria is a deadly disease with significant unmet therapeutic needs, with 2-3 billion people at risk of infection annually worldwide and 200-300 million infected annually worldwide. It remains the leading single-agent killer of children with more than 500,000 children under age 5 killed annually. There is high unmet public health need with no effective prophylactic vaccine and current Standard of Care therapeutics have potential risk from drug resistant strains.

|

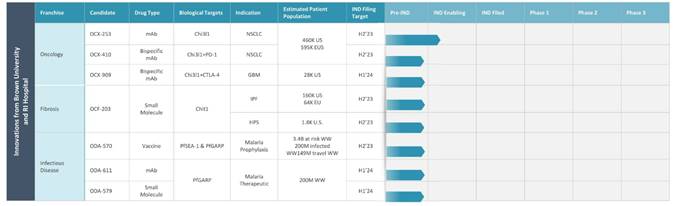

Chart 3: Ocean's Clinical Pipeline Presents Multiple 'Shots on Goal' |

|

|

Source: Intro-act, Ocean Biomedical Investor Presentation

|

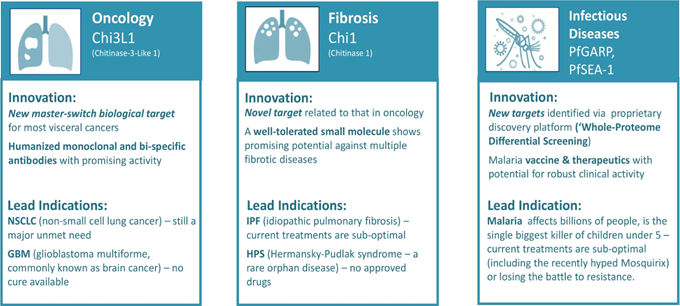

Chart 4: Ocean's Initial Portfolio Addresses High-Value and High-Impact Indications |

|

|

Source: Intro-act, Ocean Biomedical Investor Presentation

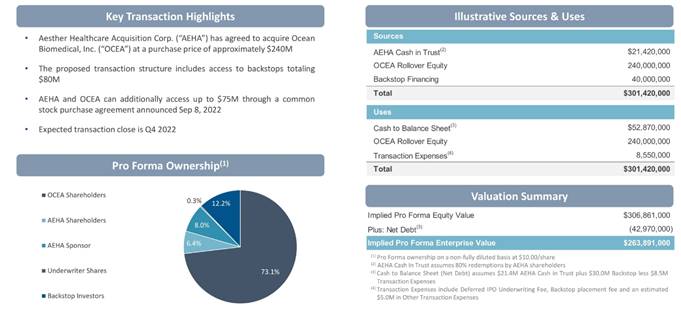

In August 2022, Ocean Biomedical announced a business combination with Aesther Healthcare Acquisition Corp. (NYSE: AEHA) that values the company at ~$264 million (pro forma implied enterprise value). The combined company will work to accelerate the development of Ocean's core assets in oncology, fibrosis, and infectious diseases, all based on new target discoveries enabling first-in-class drug and vaccine candidates and developed through past and ongoing grants totaling $123.9 million. Aesther has entered into two separate Backstop Agreements for a total of up to $80 million, with the addition of up to $40 million from Meteora Special Opportunity Fund I, LP, Meteora Select Trading Opportunities Master, LP, and Meteora Capital Partners, LP in connection with its proposed business combination with Ocean. Previously, Aesther had executed and announced an up to $40 million Backstop Agreement with Vellar Opportunity Fund SPV LLC-Series 3. Aesther Healthcare has also inked a common stock purchase agreement with White Lion Capital that will provide up to $75 million to its combination target Ocean Biomedical. The company's pro forma implied enterprise value is $263.8 million. The transaction is expected to close in 4Q22, and the combined company will be listed on the Nasdaq under the new ticker symbol 'OCEA.'

|

Chart 5: Transaction Overview |

|

|

Source: Intro-act, Ocean Biomedical Investor Presentation

Q&A OF THE MONTH - CHIRINJEEV KATHURIA, MD, MBA, CO-FOUNDER AND EXECUTIVE CHAIR, OCEAN BIOMEDICAL

Question: How did you come to work at Ocean Biomedical?

Answer: The history almost dates back three decades. My cofounders and I, who are all still leaders at the company, were classmates at Brown University and Stanford University. We went in various directions and have each been highly successful in business and in biopharma, and always stayed in touch.'

Elizabeth (Liz) Ng is our CEO. She is a pharma industry leader with very deep experience in identifying, advancing, and managing portfolios of biopharmaceutical assets at companies including Merck, Gilead, and BioMarin. Liz has evaluated hundreds of therapeutic candidates and led the advancement and development of several to market. She completed her undergraduate degree in physics at MIT, and her MBA at Stanford Business School.

Dr. Jack Elias is a founder and he chairs our scientific advisory board. Most recently he served as dean of medicine and biological sciences at Brown University, where he also was senior VP for health affairs. Jack is a physician scientist and a pre-eminent authority in the field of pulmonology. Prior to Brown he was at Yale where he served as chief of pulmonary and critical care, as chairman of the department of medicine, and as physician-in-chief. He also has served as president of the American Association of Physicians. Jack earned his M.D. at the University of Pennsylvania.

Dr. Jake Kurtis is our other scientific co-founder and our chief scientist. Jake is a physician scientist and the current chair of pathology and laboratory medicine at Brown, where he also directs the MD-PhD program. He is one of the world's leading authorities in the field of infectious disease and malaria. Jake earned his M.D. and his Ph.D. from Brown University.

Gurinder Kalra is our CFO. He is a finance professional with investment banking experience on both the buy-side and the sell-side at banks including Morgan Stanley, Bear Sterns, and Credit Suisse. Gurinder completed his undergraduate degrees in engineering and in economics at Brown, and he earned his MBA from Harvard Business School.

Together, we recognized a major issue where some of the most amazing biopharma and pharma discoveries at universities and medical centers can often get stuck in the 'Valley of Death' ' that period of transition when a discovery is deemed promising but is too new to validate commercial potential, and so the innovation doesn't receive the funding or capital needed to move forward and get fully developed.

My co-founders and I looked at this and came up with an innovative business model that would allow us to commercialize these biopharma assets by accelerating development and working with the medical and research centers where they originated to bring them past the stage of discovery, into clinical trials, and eventually into the hands of medical practitioners and patients that will benefit from them.

This model means that we are essentially the parent company to three biopharma companies, bridging the 'bench-to-bedside' gap by accelerating the development and, eventually, commercialization of innovative assets within a diversified and growing pipeline.

Question: In the long run, who will Ocean Biomedical be serving?

Answer: First and foremost, Ocean Biomedical is serving patients with some of the most devastating illnesses we face as humans today. That's why we get up in the morning and this will be our most important legacy.

We also will continue to serve universities and physician scientists to help them elevate, accelerate, and commercialize their biopharma drug discoveries, making the best use of the existing infrastructure at these universities and ensuring their advancements are moved forward to commercialization.

And, of course, as a publicly-traded biopharma company, we will have shareholders we need to serve and create wealth for. We take this responsibility very seriously and are confident in our business model, which is an engine for continual growth through preferred access to best-in-class biomedical innovations from the top universities and medical research centers.

Question: What diseases or indications are you working on / what is in Ocean's pipeline?

Answer: Our initial core portfolio is in three critical areas: oncology, pulmonary fibrosis, and infectious disease, all based on new target discoveries that will enable first-in-class drug and vaccine candidates-developed through past and ongoing grants totaling $123.9 million. These are very large markets with tremendous unmet medical needs.

Specifically, right now we're working on non-small cell lung cancer, the leading cause of cancer death and the second most diagnosed cancer; glioblastoma, a deadly type of brain tumor with very low survival rates; and finally, malaria, which many people may not realize is the single biggest killer of children under five in the world.

Scientific co-founder Dr. Jack A. Elias has discovered a master pathway that regulates multiple key cancer-inducing moieties, including critical immune checkpoint inhibitors in the lung. In turn, interventions based on this master pathway control the ability of tumor cells to develop, spread to the lung, and grow once they're in the lung. Based on these we have developed monoclonal antibodies and bi-specific antibodies that are extremely exciting potential therapeutics. For example, the discovery of bispecific antibodies that target Chitinase 3-like-1 and immune checkpoint inhibitors, kill glioblastoma cells and melanoma cells, and block the metastasis of malignant melanoma cells to the lung by over 90%.

Dr. Kurtis - team at Brown University has identified PfGARP as a target of human antibodies which kill up to 100% of parasites in vitro by inducing apoptosis or parasite programmed cell death - this discovery forms the basis of Ocean Biomedical's lipid encapsulated mRNA-based vaccine, therapeutic monoclonal antibodies, and a family of small molecule drugs. Small molecule drugs targeting PfGARP have an impressive ability to induce parasite cell death and represent a novel class of anti-malarials, which we so desperately need as artemisinin resistant parasites spread.

Question: How does your business model differ from others?

Answer: Ocean is three biotech companies in one - so we are not developing a single asset, we instead have three platform assets. We have a diversified pipeline that addresses high-value and high-impact indications, all of which are nearing the Investigational New Drug stage, which is followed by the clinical trial phase of development. Because of our business model, we'll continue to grow in our existing and new pipelines, with assets from universities and medical centers not only in the United States, but also in the EU and Asia.

IPOs and private financings reflect strong market interest in programs comparable to ours, but Ocean Biomedical really is a category of one as the parent company of three biotech companies.

Question: You recently announced the intention to go public as a SPAC - what was the motivation behind that?

Answer: We had already filed an S1 and we were ready to go public by a normal public offering. However, the SPAC transaction created further value because in these volatile markets for IPOs and biotech IPOs in particular, it was important to us to gain access to the public markets immediately. The SPAC has a significant amount of cash in trust, and we were able to sign two backstop agreements that protect us from redemptions and will allow us to keep moving forward no matter what.

For example, we have entered into two separate Backstop Agreements for a total of up to $80 million. The first is a $40 million from Meteora Special Opportunity Fund I, LP, Meteora Select Trading Opportunities Master, LP, and Meteora Capital Partners, LP. The second is a $40 million Backstop Agreement with Vellar Opportunity Fund SPV LLC-Series 3. We have also entered into a $75 million Common Stock Purchase Agreement with White Lion Capital LLC.

We structured the deal to give maximum value to investors, including a three-year earn out that if the stock price earns a certain value, there is value to the initial shareholders, which is beneficial to not only the stockholders of Ocean Biomedical, but also for the investors; something we weren't able to do that through a traditional IPO.

And on a personal note, some of the family members of our investment partners have been personally impacted by some of the diseases that we are trying to solve. They want these discoveries to advance as quickly as possible to clinical trial stage, to not only help their loved ones, but all patients suffering from these diseases. They want to propel medical innovation as quickly, responsibly, and efficiently as possible.

Question: 10 years from now, what will Ocean Biomedical look like?

Answer: 10 years from now, I believe we'll have helped change the course of humanity, and will have made the world better through better medical interventions and treatments. 10 years from now, the discoveries that we've already made within our platforms will prevent people from dying of cancer and will have solved malaria - the number one killer of young children around the world. And those are just two of the things that are currently in our pipeline. Because of our business model, everything from leukemia to scleroderma to diabetes will be investigated.

I would like to think that in 10 years, it would be unnatural for patients to suffer from these diseases - which we've been able to show in early stages through one of our projects - as well as slowing the aging process so humans will hopefully be able to live really long, healthy and productive lives.

Question: Why is Ocean a wise investment?

Answer: As a public company, you want to create wealth for your shareholders. Ocean Biomedical is a good investment today because it's the parent company of three biotech companies, and each individual platform could have a value from $345M to almost $3.62B so there is exceptional value creation as we file our Investigational New Drugs, do phase I clinical trials, and beyond. Not only that, but each of these platforms may be spun out into their own IPO, with Ocean Biomedical owning 100% of each.

For example, Ocean Biomedical's portfolio in oncology (NSCLC and GBM) could be comparable to Kinnate Biopharma (focused on specific kinase gene mutations) with a market capitalization of $345 million. Ocean Biomedical's portfolio in fibrosis (IPF and HPS) could be comparable to Pliant Therapeutics (focused primarily on IPF) with a market capitalization of $950 million. Ocean Biomedical's portfolio in infectious disease (Malaria and discovery platform for other infectious diseases) could be comparable to Vir Biotechnology (focused on COVID, HIV, HBV, Flu) with a market capitalization of $3.62 billion.

Also, M&A transactions in IPF and oncology highlight Ocean's potential for exceptional value creation. For example, in IPF the Phase 1 Samumed - United transaction in was valued at $350 million and the Phase 2 Roche - Promedior transaction was valued at $1.4 billion. In oncology, the Phase 1 Celgene - Avila transaction was valued at $925 million and the Phase 2 Roche - Ignyta transaction was valued at $1.7 billion.

Secondly, because of our innovative business model and the great management team we have to execute it, we're going to continue to develop biopharma assets from key universities and we're going to get the best assets and that's already shown to be true in oncology, fibrosis, and infectious disease. We're a preferred partner for the best investigators, because they know and respect our leadership, can continue to be involved in their discoveries, have personal and financial investment in their work, and they will continue to beat down our door to work with us.

Finally, I really see this as shareholders being able to do something good and have a significant impact on humanity - this almost becomes venture philanthropy. This company can solve some of the deadliest diseases we're facing - there is no one who hasn't been impacted by these diseases, whether it's them personally or a friend or family member. As a shareholder, what you'd be doing here is helping develop something that has already shown to have a significant impact on these diseases. So, not only can you do something good, but you can also do well financially by being involved - and who knows what other good we will do in the future together because of it.

Q&A OF THE MONTH - ELIOT BUCHANAN, CEO AND CO-FOUNDER OF PLASTIQ

Eliot Buchanan, Co-founder and CEO of Plastiq, talks about the company, its vision, flagship product, typical customers, and its merger with SPAC Colonnade Acquisition Corp. II (NYSE: CLAA).

Bio: Eliot is a Co-founder and the CEO of Plastiq, a B2B payments platform that offers bill pay and instant working capital access to businesses. Founded in 2012, Plastiq operates in the $9 trillion B2B payment market.

As an entrepreneur, Eliot is passionate about helping small businesses achieve their growth potential. As CEO, he is known as a transparent, driven, thoughtful, and compassionate leader. Under Eliot's leadership, Plastiq was named the Most Innovative Fintech Companies in Forbes' 2020 Fintech 50 and again in 2022 was named by Forbes as a top American fintech startup. Outside of Plastiq Eliot is a board advisor to various startups including Cardless, Kargo, and Grata.

Eliot holds a BA in Economics from Harvard University.

Question: What was the problem that you had personally that drove you to found Plastiq?

Answer: Back at Harvard, I decided to apply for a credit card and then tried to use that credit card to help me pay for my tuition at school. I was shocked at the fact that I could not pay my tuition with a credit card. At the time, I didn't know anything about payments or even credit cards, but it struck me as odd that I couldn't pay my tuition the way I wanted to pay.

Question: Can you tell us what Plastiq does and who it's for?

Answer: Plastiq started as a consumer-facing payment platform originally, helping consumers use a credit card to pay for anything they'd like - including tuition, rent, or even their taxes. We've since evolved into a solution for small-to-midsize businesses - helping them run all their accounts payable. We help businesses access working capital right in their payment workflows through credit cards and short-term financing. This helps improve cash flow so they can better operate their business. One of the ways we discovered this need was that we would analyze the credit cards that small businesses were using on our platform that had many of them had had no rewards. That meant that the people using these credit cards didn't care about what rewards the cards offered - they simply wanted to take advantage of the ability to use a credit card to make a payment. And as our relationships got deeper with our clients, we learned more about their needs - evolving our product and focus to help them with additional challenges like finding new sources of credit and more.

Question: Can you tell us more about the product?

Answer: Our flagship product is Plastiq Pay. As the name implies, it allows users to run all their accounts payable, all their vendors who don't take credit cards on Plastiq -giving them access to short term working capital by using their existing Visa or Mastercard, American Express. That's the dominant flagship product. We also offer payment acceptance for SMBs and embedded finance solutions for platforms and software companies that want to offer new B2B payment options to their customers..

We recently launched our own short-term financing product, allowing a business using Plastiq to select an installment or payment plan for that payment.

We also offer payment automation that helps automate the back office of a small-to-midsize business. For instance, invoice ingesting - users can snap a photo or send or forward an invoice to our system so that it automatically scans it, imports the bill to our system versus having to manually add vendors or invoices one by one. We're integrated with most of the major accounting providers like Quickbooks and many others so that a small to midsize business can import bills from Quickbooks, but also export all their payments back into Quickbooks so it's a bilateral sync designed to automate things that otherwise might be more manual to save the business time.

We help small-to-midsize businesses with automating their accounts receivable with our product Plastiq Accept. This allows them to invoice their customers or collect money from their customers and offer them a new payment choice.

Finally, we have a white label API product aimed at platforms who service SMBs and we call that Plastiq Connect.

Question: Can you tell us more about payment processing and navigating traditional credit card processing fees?

Answer: For five or six decades now, the credit card industry has been focused on one primary value proposition which is convincing merchants that in order to accept credit cards, they should be paying a fee of 3 - 4%. Our entire approach is the exact opposite. We believe that part of the reason the $9 trillion market of B2B payments does not run on credit cards is the reason that the merchant has no interest nor ability paying that type of fee - so we reverse the fee. Our belief is most of the ecosystem can support what we call a buyer-funded model versus a supplier-funded model. With our Plastiq Accept product, the ability to accept credit cards is free and the fee is managed by the buyer.

Question: Can you tell us more about your typical customer?

Answer: Our customer is your typical small-to-medium sized business, but we're probably a little more on the 'M' of the SMB spectrum versus the 'S.' These are businesses that have between $500k and $50 Million in revenue and they might have five to 100 employees. They're not a venture capital-funded startup, they've been around a few years, they have access to credit, but they still have constant short-term working capital needs. We don't have a heavy concentration in any particular industry, but most of our customers are in some form of e-commerce ' specifically wholesalers or retailers. Our customers have a heavy reliance on supply chains where they're buying inventory in bulk and then having to sell it which means that there's a revenue gap they have to manage ' and Plastiq helps them manage that gap.

Question: You recently announced the intention to go public via SPAC. What was the driver behind the decision to do it now?

Answer: We're excited about becoming a publicly traded company for many different reasons, but there were two primary drivers for us. First, we knew that if we found the right SPAC partner we could sufficiently capitalize the company, which would give us a competitive advantage in the market. Second, becoming a publicly traded company helps showcase our credibility in the market. It will help us attract new partners, talent and clients ' which will be incrementally valuable as we continue to grow.

Question: Once the deal closes, what are your plans for Plastiq ahead as a publicly traded company?

Answer: We plan to invest significantly into product and feature development ' helping our customers with new capabilities and solutions that make their businesses run more effectively. We're also going to explore some M&A opportunities, looking for companies that would complement and extend our current product portfolio. We'll also look to invest in additional go-to-market activity to increase awareness for Plastiq across the board.

Question: What's your vision for Plastiq, where do you see the company a decade from now?

Answer: It's hard to predict what's going to happen tomorrow, let alone 10 years from now. I do expect that Plastiq will continue to expand its product portfolio addressing new challenges that our customers face every day ' particularly as technology and the market evolves. When I think further down the road, I see Plastiq as more of an infrastructure solution for the accounts payable needs of any provider that wants to monetize their small-to-midsize business base, whether it be banks or payroll companies or insure-tech companies, etc.

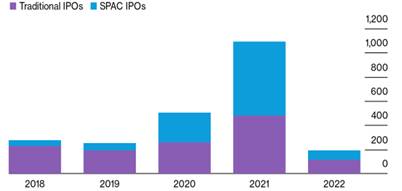

An in-depth look at SPAC activity throughout the third quarter and year-to-date. Now that the third quarter of 2022 has come to a close, we take a look back at year-to-date activity. Market conditions tied to inflation, Fed rate hikes, and geopolitical risk have all exerted their influence on the markets this year and anxiety continues to climb ever higher. However, regulatory risk thanks to the SEC's final SPAC rule proposal, which is due any day now, promises fresh challenges. Looking back at the third quarter, new SPAC issuance slowed to a trickle with only eight new IPOs priced raising a total of $678 million in gross public proceeds. This is a vast change from the third quarter of 2021, which priced 89 SPACs and raised $17.6 billion. Read More (SPACInsider)

|

Chart 6: Q3-2022 SPAC IPO Count and Total Gross Proceeds Raised by Month |

|

|

Source: Intro-act, SPACInsider

ICR, the leading SPAC communications and advisory firm, publishes Q3 2022 SPAC market update. ICR, a leading strategic communications and advisory firm, released its Q3 2022 SPAC Market Update report. The SPAC IPO market paused in Q3 2022 as SPAC sponsors await more regulatory clarity and deal with the high cost of capital. In the third quarter, eight SPACs raised $0.7 billion compared to the second quarter of 2022, when 16 SPACs raised $2.2 billion, given the challenging market backdrop. Despite the slowdown in new blank check companies, the SPAC market announced 48 new business combinations and closed 25 mergers in Q3. The third quarter was the slowest for new equity issuers in over a decade, with just 25 initial public offerings (IPO) raising $2.4 billion, of which only three IPOs raised $100 million or more. While there are some signs of life heading into the final stretch of 2022, IPO issuance is unlikely to begin normalizing until 2023. Read More (Business Wire)

Global IPO market continues to plummet as we round out Q3. Year-to-date (YTD) 2022, there have been a total of 992 IPOs raising $146 billion, a 44% and 57% decrease year-over-year (YOY), respectively, according to audit and advisory firm EY. This follows the trend for the year in which IPO companies and investors were faced with mounting macroeconomic challenges, market uncertainties, increasing volatility and falling global equity prices. Volatility (CBOE VIX average) increased from 19.7 in 2021 to 25.6 in YTD 2022. The third quarter (Q3) of 2022 saw the lowest special purpose acquisition company (SPAC) IPO proceeds since Q3 2016, along with de-SPACs struggling to find the right targets. Read More (TechNode Global)

Equity issuance, SPAC activity, IPO performance continue to slide in Q3. Activity in the global equity capital markets decelerated over the first three quarters of 2022, as market volatility, inflation, and contractionary monetary policies had an adverse impact on companies that were looking to raise equity capital. Through the first nine months of 2022, 3,377 offerings closed (39% lower than the same period last year) and $313 billion in total gross proceeds was raised (61% lower). Initial public offering (IPO) proceeds amounted to $125 billion in the first nine months of 2022, which was a 60% decline compared to the same period in 2021. The volumes of all offering types continued to decline year over year. Read More (S&P Global)

|

Chart 7: Global Special Purpose Acquisition Companies IPOs by Quarter |

|

|

Source: Intro-act, S&P Global

IPOs & SPACs: Where did they go? One of the fascinating developments during the COVID-19 pandemic was Wall Street's short-lived obsession with IPOs and SPACs.' What are they, why did they become so popular, and why did they drop off so quickly? Although 2021 was a record-breaking year for raising cash, the initial performance of those now-public companies paint a gloomier picture. High growth stocks experienced a broad selloff toward the end of 2021 that has continued through the first three quarters of 2022, and recent IPOs have not been excluded from the carnage. Two-thirds of the companies that went public in the U.S. in 2021 were trading below their IPO prices by the end of 2021. Moreover, through the first three quarters of 2022, nearly 90% of companies that went public in 2021 are trading below their initial offering prices, close to -50% on average. Read More (Inside INdiana Business)

SPAC managers emerge as clear winners of the SPAC boom and bust. With SPACs the house always wins ' even as investors lose their shirts. The blank-check companies behind the public listings of brand names like DraftKings, WeWork, and BuzzFeed often score big wins even as stock market investors get stung by instantly plummeting valuations after those companies go public, according to a forthcoming paper published in the Review of Financial Services. Read More (The Motley Fool)

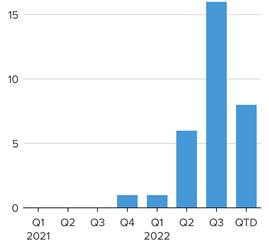

SPAC liquidations on the rise as companies struggle to find deals. Yahoo Finance's Alexandra Semenova discusses the troubled SPAC market as companies run out of time to find merger deals. SPAC liquidations are on the rise with these blank check companies really struggling to find targets for their deals. To close so far this year, 22 special purpose acquisition companies worth about $10 billion have been liquidated, according to a weekly report by SPAC Research. That's more than ' and more than half of those liquidations have occurred since August. And that's not even taking into consideration the liquidations that have been announced and haven't actually happened yet. Watch Video

U.S. market shivers in IPO winter; China feels fine. The U.S. IPO market has almost entirely frozen over, with very few companies even trying to navigate the treacherous environment of market volatility, rising interest rates, and low investor appetite for new issues. The poor performance of companies that have recently completed their initial public offering has only tightened this winter's grip. How much have U.S. IPOs fallen? Quite a lot. In the recently completed quarter, U.S. IPOs were down 87.5%, and raised nearly 98% less capital compared to the first quarter of 2021, when new issues peaked. Only 52 companies went public in the U.S. in Q3, raising $2.8 billion. Read More (Bloomberg Law)

|

Chart 8: IPO Deal Counts Drop Well Below 2018 Levels |

|

|

Source: Intro-act, Bloomberg Law

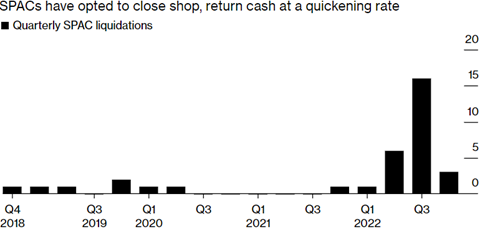

SPAC liquidations top $12 billion this year as sponsors grapple with tough market, new buyback tax. A new buyback tax has motivated more SPAC sponsors to close up shop before the year-end, adding another headwind to the blank-check space already roiled by a tough market environment, CNBC reports. A total of 27 SPAC deals, worth $12.8 billion, have been liquidated this year, according to data from SPAC Research. Under the new provision in the Inflation Reduction Act, SPAC sponsors could face a 1% exercise tax if they return cash to investors starting in 2023. Read More (CNBC)

|

Chart 9: Liquidation hit $12.8 billion in 2022 |

|

|

Source: Intro-act, CNBC

SPACs push to close up shop early as new U.S. tax targets share buybacks. SPAC sponsors, already grappling with Wall Street's lost appetite for their deals, are beginning to shut down operations early to avoid potential hits from a new U.S. tax that targets share buybacks. The bulk of the $165 billion held by special-purpose acquisition companies could face a 1% excise tax if they return cash to investors after the start of the new year, making them collateral damage of the new provision included in President Joe Biden's Inflation Reduction Act. Already, two SPACs have specified that they want to return the cash they raised to investors before year-end to avoid getting dinged, and that number is likely to grow. 'This is yet another hurdle for SPAC sponsors in an environment that's already very difficult for them to be successful,' said Julian Klymochko, who manages a SPAC-focused fund at Accelerate Financial Technologies. Read More (Bloomberg)

|

Chart 10: Sponsors Shutting Down |

|

|

Source: Intro-act, Bloomberg

SPACs and the 1% excise tax. The Inflation Reduction Act of 2022 imposes a 1% excise tax on the repurchase of corporate stock by a publicly traded U.S. corporation following December 31, 2022. For purposes of the Excise Tax, a 'repurchase' will generally include redemptions, corporate buybacks and other transactions in which the corporation acquires its stock from a shareholder in exchange for cash or property, subject to exceptions for de minimis transactions and certain reorganizations. Over the last two months, many SPACs have issued proxy statements and other SEC filings containing a disclosure about the risks associated with the Excise Tax. Read More (Lexology)

Not so SPAC-tacular anymore. When the special purpose acquisition corporation (SPAC) boom was in full swing, a number of VCs jumped in by sponsoring their own. Now, several have withdrawn from the market. Why it matters: Turns out, SPACs aren't everything to everyone. The broader market downturn has also affected SPACs, so at least a handful of firms have made a U-turn. "The great irony is that the market that finally allows attractively priced investments opportunities is also the same market that leads the tolerant investor to go to the sidelines," a general partner of a VC firm that pulled its SPACs tells Axios. Read More (Axios)

Lukewarm SPAC market's fate is intertwined with IPOs. It's clear now that modern reverse mergers between SPACs and low-revenue, high-growth companies are faring about the same as the IPO market: not well. That's largely due to the volatile public markets. PitchBook's VC-backed IPO and deSPAC indexes have each posted losses of more than 45% YTD. But interest from shareholders has also waned as they seek to de-risk their portfolios, and that sentiment led only 35 new SPAC vehicles to list on public exchanges during the third quarter. In latest analyst note, the Q3 2022 SPAC Market Update, Cameron Stanfill posits that the dropping activity levels in Q3 may have sounded the death knell of the SPAC renaissance. Read More (PitchBook)

What's on the horizon for SPACs? Bitter economic conditions, political unrest, repeat regulatory hits, the uncertainty of the proposed SEC rules, loudly touted examples of a few bad apples, and continued media negativity have left the SPAC market tattered and bruised. The wave of liquidations (33 so far in 2022 according to SPAC Research) should work itself out before year-end, and that will leave fewer teams competing for deals. This, however, will not be enough to move the needle on the economic situation in the U.S. and around the world. While we will continue to solve new problems that just keep on coming this year, it may take months before we see a recovery. Read More (JD Supra)

SPAC sponsors were winners even on losers. Since AEye Inc. went public by merging with a special-purpose acquisition company in August 2021, shareholders have had a rough go. The company that ran the SPAC has fared far better. The financial-services firm Cantor Fitzgerald LP invested less than $10 million in the deal but has since reaped at least $35 million in fees related to the listing, share sales and the value of remaining holdings, securities filings show. As the air has come out of the SPAC boom of recent years, a clear winner has emerged: the money managers who oversaw the blank-check companies and who kept making profits even in the face of significant losses to stock investors. Read More (The Wall Street Journal)

SPACs have less reliable financial reporting, UI study finds. Acquisitions made with a Special Purpose Acquisition Company (SPAC) are more likely to have mistaken in their financial statements than a traditional initial public offering (IPO), University of Iowa researcher Ryan Wilson said on The Voice of Corporate Governance podcast. Their study looked at data for post-merger SPAC firms and companies that went public from 2006 to 2020. They found that SPAC firms after an acquisition had a 9% higher likelihood of restatements due to errors, more amended returns, a higher percentage of internal control weaknesses identified by auditors and management teams, and more untimely filings. Read More (Corridor Business Journal)

Zukin Certification Services and Banyan risk bundle reasonable basis review of SPAC target projections with SPAC D&O insurance. Zukin Certification Services announced a partnership with specialty insurer Banyan Risk to offer discounted Directors' and Officers' insurance in combination with a subsidized Zukin Reasonable Basis Review ' a service designed to provide SPACs with an independent review of a target company's financial projections. Since receipt of a Zukin RBR Certification can serve to mitigate a transaction's risk profile, according to the press release, Banyan will offer its SPAC clients both a subsidized rate on the Zukin RBR service as well as discounted D&O insurance premiums. Read More (Business Wire)

How post De-SPAC companies can prepare for a tidal wave of proxy fights, hostile M&A, and short attacks. Post De-SPAC public companies saw an unprecedented number of shareholder activism campaigns during the 2021 and 2022 proxy seasons. The vast majority of these campaigns took the form of short attacks and proxy fights against post de-SPAC public companies to replace directors. As market capitalizations of these companies continue to plunge, a rise in another form of activism ' hostile M&A ' is expected. Vinson & Elkins offered a webinar presentation and discussion of these issues. Read More (Vinson & Elkins)

Big four shunned SPAC IPOs but now flock to audit new companies. When SPACs became Wall Street's favorite way to take companies public, the Big Four accounting firms steered clear, leaving audit work to smaller outfits churning out hundreds of fast, cheap audits of the blank-check vehicles. For those freshly minted public companies that emerged from the boom, it's been a different story. The largest firms ' Deloitte & Touche, PricewaterhouseCoopers, KPMG, Ernst & Young and their affiliates ' audit almost two-thirds of the approximately 330 companies that went public through special purpose acquisition companies since 2020 and are still trading today, according to Bloomberg data. Read More (Bloomberg Tax)

SEC reopens comment periods for some SPAC rules after tech glitch. The SEC said it has reopened the public comment periods for 11 of its rulemaking releases, some of them viewed as controversial, due to a technical glitch that led to a number of comment letters being lost. The majority of the comments affected by the technological error, which affected the SEC's internet submission form, were submitted in August, though some may go back as far as June 2021, the regulator said. The affected releases include rulemaking on SPACs, climate disclosure, money market funds and short positions. Read More (Reuters)

Managing litigation risks in De-SPAC transactions. As SPAC litigation continues to proliferate, it is more important than ever that officers and directors of companies undertaking a de-SPAC transaction be mindful of litigation risks and adopt strategies for managing them. After all, a de-SPAC transaction ' by definition ' thrusts a formerly private enterprise into the more litigious world of publicly traded companies. The presentation will survey the different types of securities and M&A litigation arising from de-SPAC transactions ' including Delaware fiduciary duty litigation, federal securities class actions, derivative lawsuits, SEC investigations, and de-SPAC counterparty litigation. Read More (Vinson & Elkins)

Chamath Palihapitiya: 'I massively benefited' from Fed policy. Investors in risky asset classes 'massively benefitted' from years of ultra-easy monetary policy, Chamath Palihapitiya, founder and CEO of Social Capital. Chamath made his name as a boastful memelord, leading a crowd of retail investors into SPACs and crypto. Now he's wearing a dark suit, talking about risk-adjusted returns and intellectual rigor, and remorsefully saying that he was blinded by zero interest rates. Everything he did at the height of the boom, he now says, was just an 'experiment' in terms of generating returns for his investors. With inflation perched near 40-year highs, the Federal Reserve is embarked on its most aggressive tightening campaign in decades ' reversing years of zero interest rates that fueled massive speculative bubbles, Palihapitiya acknowledged. Read More (Axios)

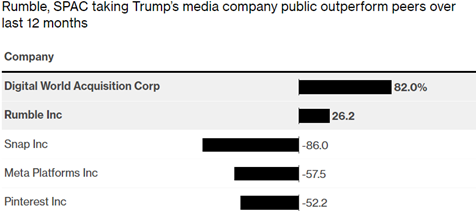

Trump-tied SPAC, Rumble show power of hardcore followers. Legions of followers betting on conservative social-media platforms have helped stocks like Rumble Inc. and the blank-check firm taking Donald Trump's media company public to outperform peers, a sign that speculative fervor in the market is still high. The pair are, respectively, one of the best performers this year among firms that merged with a special-purpose acquisition company and the top-gaining SPAC since listing that hasn't yet completed a combination. That outperformance ' at a time when shares of established social-media companies mostly are in free fall ' has been fueled in part by retail traders. Read More (Bloomberg)

Chart 11: New Kids on the Block |

|

|

Source: Intro-act, Bloomberg

Defund the S.E.C.' becomes a rallying cry on Trump's social media site. The Securities and Exchange Commission is corrupt. The S.E.C. is politically motivated. Defund the S.E.C. Some shareholders of Digital World Acquisition Corp. have had it with the commission, the nation's top securities cop, and they are airing their views loudly. People claiming to be angsty shareholders have taken to posting the social media equivalent of hate mail on Truth Social, attacking the S.E.C. and calling its investigation a political move. The hashtag #DWACtheSEC, a reference to Digital World's stock symbol and a play for some on the word 'whack,' is trending. There are calls to 'defund the S.E.C.' Shareholders are preparing to petition the commission to end the 'garbage' inquiry and approve the deal. There is even a call to pray for Digital World on a weekly video show on Rumble, a right-wing streaming media site that is a business partner of Trump Media. Read More (The New York Times)

Pot banking firm Safe Harbor Financial targets talent, M&A following SPAC deal. Safe Harbor Financial completed its special-purpose acquisition corporation (SPAC) deal with Northern Lights Acquisition Corp., a deal its CEO said will position the cannabis financial services provider to tap executive-level talent and pursue strategic acquisitions. 'What we really want to accomplish is to be a one-stop financial service provider to the cannabis industry that is as reliable as the Safe Harbor reputation has become over the last eight years,' Safe Harbor CEO Sundie Seefried said. Since its inception, the cannabis banking services provider, which has operations in 20 states, says it has assisted in onboarding more than $12 billion in deposit transactions for customers. Read More (Banking Dive)

SPAC deal in limbo: Gaming tycoon vows to keep up Philippine casino fight after arrest. Gaming tycoon Kazuo Okada has vowed to fight for his interests in Okada Manila ' the multibillion-dollar Philippine casino that bears his name ' after his arrest in Manila opened a new chapter in the drawn-out dispute over the company. The dispute has delayed indefinitely Okada Manila's plans to list on Nasdaq by merging with 26 Capital Acquisition in a deal that would value the casino at $2.5 billion. The listing had planned to capitalize on the revival of the tourism industry, but the dispute has turned off some U.S. investors, Jason Ader, head of 26 Capital. Okada is facing charges of 'grave coercion' in relation to the physical takeover of the Okada Manila integrated resort and casino by his associates in May. Read More (Nikkei Inc.)

Investing in Space: Cash crunch. After a dozen space ventures rushed through the gates to go public via SPACs, a market downturn and the pinch of rising inflation have been ruthless to the fresh stocks. We're now in the final quarter of the year, and for several space companies, it's survival time. 'It's not because they're necessarily bad businesses. They weren't proven businesses, and the tide went out,' a banker familiar with the sector told me about the environment for space stocks. 'How many can bleed their way through to the market reopening?' While not a definitive metric, the cash burn rates of de-SPAC space companies ' from AST SpaceMobile to Redwire and more ' give a window into the urgency of the situation. Among the group, the burn rates for the first half of the year meant the average company, as of August, had roughly enough cash to last another three quarters. Read More (CNBC)

Thematic Times: SPACs in the Thematic Space. In 2020, over 50% of new publicly listed companies were SPACs, with a large portion being in disruptive technology and growth-oriented industrial manufacturing stocks, including electric vehicle, space, and biotechnology companies. Many of these became constituents within thematic indexes and ETFs and contributed to high performance throughout 2020 and early 2021. But with both higher interest rates and higher risk aversion, many companies that have gone public through SPAC mergers are now trading below their initial offering prices, and there are also less SPACs mergers occurring in 2022. However, thematic sectors are not necessarily anchored to growth in SPAC mergers'many new public companies still prefer the IPO process, while many of the largest players in thematic sectors are actually older companies adapting toward a new trend. This note provides a brief overview of what SPACs are, how they have changed, and how they relate to thematic investing. Read More (Vettafi)

Top 3 SPAC targets ' Consumer/Retail. As fun as it was in 2020 and 2021 when SPACs were saving the world with their investments in EVs and green power, it's clear that for now, SPACs need to be focused on providers of the stuff that people will buy no matter what shape the world is in. For consumer companies that are ready for a step-up and would rather remain independent, this would indicate that a straight IPO is not going to be the way to go. Year-to-date, the five consumer goods companies that have IPO'd are down -57.5%. Had these firms instead opted for SPAC deals, they could have at least lined up earn-out provisions that would have locked in upside value for when the market turns up again. Read More (SPAC Insider)

TASE's only SPAC to merge with food co Baladi. ISPAC 1 Ltd. (TASE: ISPC), the only special purpose acquisition company (SPAC) to have held an offering on the Tel Aviv Stock Exchange (TASE) has found a target company to merge into - food manufacturer Baladi, currently owned by hotelier Erez Dahabani. ISPAC 1, which raised NIS 400 million in August 2021, announced that it had signed a non-binding memorandum of understanding (MoU) to acquire Baladi. Baladi is headquartered in Beer Tuvia next to Kiryat Malakhi, with a manufacturing plant in the Izrael Valley. The company, which imports, manufactures and markets food products with an emphasis on meat, was founded in 1916 as a family owned butcher in Tel Aviv's Carmel market. Read More (Globes)

FinAccel becomes Singapore's newest unicorn after canceling SPAC merger, U.S. IPO plans. Singapore-based FinAccel'the parent of Indonesia's buy now, pay later (BNPL) platform Kredivo ' has become the city-state's newest unicorn after raising almost $140 million in a funding round months since the firm canceled a SPAC merger and IPO plans due to unfavorable market conditions. The Series D funding was led by existing investor Mirae Asset with participation from Cathay Innovation, Endeavor Catalyst, GMO Global Payment, Jungle Ventures, Open Space Ventures, and Square Peg, according to data from research firm VentureCap Insights. The deal values FinAccel at $1.66 billion, more than thrice the $451 million valuation when it last raised funding in 2019. Read More (Forbes)

Former Rusal Chief launches London's first mining SPAC. One of the most prominent Anglo-Russian executives in the metals industry is seeking to raise $125 million for a new mining venture through a London-listed SPAC. Artem Volynets, former chief executive of EN+ Group, believes now is a good time for mining deals, particularly for critical metals such as copper and cobalt, despite difficult market conditions. 'This is a great time. The valuations are depressed,' Volynets said. 'The next 12 months is a terrific time to negotiate a transaction . . . It has been placed into our hands.' Read More (Financial Times)

Regulatory challenges to allowing SPAC IPOs in Indonesia. Regardless of the benefits that a SPAC provides, the current regulatory framework in Indonesia presents several regulatory challenges that will need to be addressed before SPAC IPOs (and de-SPACs) can be implemented in Indonesia. An important provision under the Indonesian Company Law that needs to be observed concerns merger requirements. The law requires a joint merger plan document to include, among other things, the financial report of each merging company for the past three years. This is quite different from an acquisition transaction, where the law only requires the latest financial report of each of the acquiring and target companies. Read More (IFLR)

Investing in Indian companies via SPAC: Does it pose any risks for the investors? Indian car rental platform Zoomcar Inc said it would go public in the U.S. through a blank-check merger valuing the combined company at $456 million including debt, as it seeks to expand into new markets. SPACs come with risks for investors, just like any investment. The management of the SPAC's skill in navigating the market of the target firm is one of the primary concerns. SPAC management teams often comprise professionals, and the majority of them have solid investing backgrounds. However, if SPAC management lacks knowledge of the target firm's market niche, this might have unfavorable effects on both the target company and its shareholders. Read More (Mint)

Dragonfly Energy Corp. (DFLI) and Chardan NexTech Acquisition 2 Corp. complete business combination. Dragonfly Energy Corp., an industry leader in energy storage and producer of deep cycle lithium-ion storage batteries, has completed its business combination with Chardan NexTech Acquisition 2 Corp on October 7, 2022. The combined company will operate under the name Dragonfly Energy Holdings Corp. Commencing October 10, 2022, Dragonfly's common stock and warrants are expected to trade on the Nasdaq Stock Exchange under the symbols 'DFLI' and 'DFLIW,' respectively. The company will continue to be led by Dr. Denis Phares, Chief Executive Officer, alongside the rest of the current Dragonfly management team. Dragonfly intends to use the proceeds to accelerate the market penetration of its existing business and commercialize its proprietary and patented All-Solid-State-Battery technology that will dramatically reduce reliance on the power grid. Read More (GlobeNewswire)

Granite Ridge Resources, Inc. (GRNT), Grey Rock Investment Partners, and Executive Network Partnering Corporation complete business combination. Grey Rock Investment Partners, a Dallas-based investment firm, and Executive Network Partnering Corp. (NYSE: ENPC), a special purpose acquisition entity, announced that they have successfully closed business combination resulting in the formation of publicly traded Granite Ridge Resources, Inc. Granite Ridge's common stock and warrants started trading on the NYSE under the ticker symbols 'GRNT' and 'GRNT WS', respectively, on October 25, 2022. Granite Ridge is led by President and Chief Executive Officer Luke Brandenberg and Chief Financial Officer Tyler Farquharson. As a result of the business combination, Granite Ridge owns the non-operated working interests previously held by Grey Rock's Fund I, Fund II and Fund III portfolios, and such Grey Rock funds and/or their limited partners own equity in Granite Ridge. Read More (Business Wire)

Cardio Diagnostics Holdings, Inc. (CDIO) and Mana Capital Acquisition Corp. complete business combination. Cardio Diagnostics Holdings, Inc., a pioneering precision cardiovascular medicine company at the intersection of epigenetics and artificial intelligence whose products enable improved prevention, early detection, and treatment of cardiovascular disease, completed its business combination with Mana Capital Acquisition Corp. (Nasdaq: MAAQU; MAAQ; MAAQW; MAAQR), a publicly traded special purpose acquisition company. The transaction was approved at a special meeting of Mana Capital stockholders held on Tuesday, October 25, 2022. Mana Capital's stockholders also voted to approve all other proposals presented at the special meeting. Read More (Business Wire)

Selina (SLNA) and BOA Acquisition Corp. complete business combination. Selina, the fast-growing lifestyle, and experiential hospitality company targeting millennial and Gen Z travelers whose mission is centered on building meaningful connections, and BOA Acquisition Corp. (NYSE: BOAS), a publicly traded special purpose acquisition company, closed their business combination. The business combination was approved by BOA stockholders at a special meeting held on October 21, 2022. Samba Merger Sub, Inc., a subsidiary of Selina, merged with and into BOA, with BOA surviving the merger and, as a result of that merger, BOA became a direct, wholly owned subsidiary of Selina, with the securityholders of BOA becoming securityholders of Selina. Selina's ordinary shares and public warrants started trading on the Nasdaq under the ticker symbol 'SLNA' and 'SLNAW', respectively. Read More (Business Wire)

SatixFy Communications Ltd. (SATX) and Endurance Acquisition Corp. complete business combination. SatixFy Communications Ltd., a leader in next-generation satellite communication systems based on in-house-developed chipsets, has completed its business combination with Endurance Acquisition Corp. following the approval of the business combination by Endurance's stockholders on October 25, 2022, and satisfaction of customary closing conditions. The combined company's shares and warrants started trading on the NYSE American under the symbols 'SATX' and 'SATX WSA,' respectively, Friday, October 28, 2022. SatixFy develops end-to-end next-generation satellite communications systems, including satellite payloads, user terminals and modems, based on powerful chipsets that it develops in house. Read More (SatixFy)

SeaStar Medical, Inc. (ICU) and LMF Acquisition Opportunities, Inc. complete business combination. SeaStar Medical, Inc., a medical technology company developing proprietary solutions to reduce the consequences of hyperinflammation on vital organs, has completed its business combination with LMF Acquisition Opportunities, Inc. (NASDAQ: LMAO), a special purpose acquisition company sponsored by LM Funding America, Inc. (NASDAQ: LMFA). The business combination closed on October 28, 2022. Following the closing of the business combination, LMF Acquisition Opportunities, Inc. was renamed SeaStar Medical Holding Corp. and will operate under the same management team as SeaStar Medical, which is led by Eric Schlorff, CEO. Caryl Baron will serve as interim CFO. The common stock and warrants of SeaStar Medical Holding Corporation are expected to begin trading on Nasdaq on October 31, 2022, under the new ticker symbols 'ICU' and 'ICUCW,' respectively. Read More (SeaStar Medical)

Perfect Corp. (PERF) and Provident Acquisition Corp. complete business combination. Perfect Corp., a global leader in providing augmented reality and artificial intelligence Software-as-a-Service solutions to beauty and fashion industries, and Provident Acquisition Corp. (Nasdaq: PAQC), a special purpose acquisition company, announced the completion of business combination. The listed company resulting from the Business Combination will be called Perfect Corp., and its shares and warrants started trading on the New York Stock Exchange under the ticker symbols 'PERF' and 'PERF WS,' respectively, on October 31, 2022. Utilizing facial 3D modeling, and AI deep learning technologies, Perfect empowers beauty brands with product try-on, facial diagnostics, and digital consultation solutions to provide consumers with an enjoyable, personalized, and convenient omnichannel shopping experience. Read More (Business Wire)

Coeptis Therapeutics, Inc. (COEP) and Bull Horn Holdings Corp. complete business combination. Coeptis Therapeutics, Inc., a biopharmaceutical company developing innovative cell therapy platforms for cancer, completed its business combination with Bull Horn Holdings Corp. (Nasdaq: BHSE), a special purpose acquisition company.' In connection with the Business Combination, the combined company has been renamed "Coeptis Therapeutics Holdings, Inc." and its public shares and warrants started trading on the Nasdaq Global Market under the ticker symbols "COEP" and "COEPW," respectively, on, October 31, 2022.' The Company will continue to focus primarily on the development of innovative cell therapy platforms for patients with cancer. Read More (Coeptis Therapeutics)

$3.6 billion SPAC merger falls apart for blockchain payments startup Roxe. The public debut for blockchain payments startup Roxe has been scrapped after its special purpose acquisition company (SPAC) merger with Goldenstone Acquisition was mutually terminated. Since the move to end the agreement was equally decided by both parties, there are no termination fees, according to the most recent SEC filing. No reasons were given for ending the deal and few details were offered in the notice. The merger was originally scheduled to close in the first quarter of 2023 as Roxe Holding Group Inc and be listed on the Nasdaq under the ticker ROXE. Headquartered in New York, New York, Roxe powers payments and digital commerce solutions for merchant remittances and consumer purchases. Read More (PYMNTS)

G Squared and Transfix call off $1.1 billion deal. G Squared Ascend I and freight platform Transfix terminated their merger agreement by mutual decision, citing current public market conditions. G Squared and New Enterprise Associates (NEA) will instead lead a private round of investment to support Transfix's continued growth. As part of this financing, G Squared's Founder & Managing Partner, Larry Aschebrook, will join the Transfix board. NEA initially partnered with Transfix during the Series B round in 2016. In tandem with that extension, funds affiliated with the SPAC will provide $50 million of guaranteed financing to Transfix on an accelerated timeline on or before Sept. 30, under a Forward Purchase Agreement. In addition, G Squared agreed to provide Transfix with up to an additional $50 million of committed capital whether or not the proposed merger closed. Read More (PR Newswire)

OceanTech Acquisitions I terminates $224 million Captura Biopharma deal. OceanTech Acquisitions I announced that its merger agreement with Captura Biopharma has been terminated by mutual agreement. The SPAC said it will seek an alternative business combination. Few days ago, OceanTech filed a preliminary proxy in which it proposed a merger deadline extension from Dec. 2 until June 2, 2023. The SPAC in the proxy said it needed more time to finalize the Captura deal. Announced in August, the deal was to deliver $120 million to Captura, minus any debt on the target's books and assuming no SPAC share redemptions. Captura shareholders also stood to gain 2 million pay out shares if the FDA approves the company's radionuclide decorporation agent under development. Read More (Business Wire)

eCombustible walks away from Benessere Capital Acquisition deal. Benessere Capital Acquisition in an 8-K filing said its merger partner eCombustible has terminated the deal. No reason was given. The SPAC's stockholders in July approved an extension date for the merger deadline to Jan. 7, 2023. The deal was valued at $805 million. eCombustible Energy provides customizable hydrogen-based fuel for thermal industrial applications. Benessere CEO Patrick Orlando also leads Digital World Acquisition, the SPAC struggling to take Donald Trump's social media company public. Read More (SEC)

Dish Network chairman-backed SPAC in talks to buy wireless business unit. Blank-check firm CONX Corp, backed by Dish Network Corp (DISH.O) Chairman Charles Ergen, has begun preliminary discussions to acquire Dish's retail wireless unit, Boost Mobile. The special-purpose acquisition company (SPAC) said it will appoint a special committee of independent and disinterested directors to evaluate and approve the terms of any deal with the pay-TV and wireless carrier. Dish acquired Boost Mobile in 2020 as part of the T-Mobile (TMUS.O) and Sprint merger after the companies agreed to divest some assets including some wireless spectrum to create a new wireless competitor. Read More (Reuters)

Everton FC takeover plotted by SPAC led by George Soros' nephew. Everton FC is drawing takeover interest from a SPAC co-led by George Soros' nephew. LAMF Global Ventures I has held preliminary talks with the English Premier League football club about a deal. LAMF is led by Jeffrey Soros and Simon Horsman, both Los Angeles-based producers. It counts veteran football dealmaker and former Everton director, Keith Harris, as a senior adviser. Read More (Bloomberg)

Canadian airline Flair said to be in merger talks with New Vista Acquisition. Flair Airlines Ltd., a low-cost Canadian airline, is in talks to go public through a merger with New Vista Acquisition, which is backed by a former Boeing CEO. New Vista may seek to raise additional financing to support a transaction. The SPAC is led by Dennis Muilenburg, Boeing's CEO from 2015 to 2019. Muilenburg was fired as Boeing's CEO for fostering a culture that prioritized profits over safety, having led the company during the 737 Max rollout. Read More (Bloomberg Law)

CVS in exclusive talks to acquire Cano Health. CVS is currently conducting due diligence on the Miami, Florida-based company that focuses on seniors and underserved populations. Cano, which operates 141 primary care facilities for seniors in California, Florida, Texas, Nevada, Illinois, New Mexico, and Puerto Rico, went public in June 2021 after completing a $4.4 billion business combination with special purpose acquisition company (SPAC) Jaws Acquisition Corporation, which is sponsored by Starwood Capital founder, chair and CEO Barry Sternlicht. The reported talks come after CVS announced last month that it would acquire home health care company Signify Health in a deal valued at about $8 billion. CVS previously acquired Aetna for $68 billion in 2018 and Caremark for $27 billion in 2007. Read More (Yahoo! Finance)

|

Chart 12: SPAC Events ' November 2022 |

|

S. No |

Event Name |

Date |

Time |

|

1 |

HTAQ: Expected Liquidation |

11/1/2022 |

|

|

2 |

MAQC Deadline extension vote |

11/1/2022 |

10AM EST |

|

3 |

BHSE Deadline extension vote |

11/2/2022 |

10AM EST |

|

4 |

HAAC: Expected Liquidation |

11/3/2022 |

|

|

5 |

HPX Deadline extension vote |

11/3/2022 |

9AM EST |

|

6 |

DWAC Deadline extension vote |

11/3/2022 |

10AM EST |

|

7 |

ESSC & NTWN Merger Vote |

11/7/2022 |

9AM EST |

|

8 |

VCXA Deadline extension vote |

11/9/2022 |

9AM EST |

|

9 |

MCAE Deadline extension vote |

11/9/2022 |

10AM EST |

|

10 |

NOVV Deadline extension vote |

11/9/2022 |

10AM EST |

|

11 |

OXAC Deadline extension vote |

11/9/2022 |

10AM EST |

|

12 |

VCKA & Scilex Merger Vote |

11/9/2022 |

10AM EST |

|

13 |

AGBA & TAG Merger Vote |

11/10/2022 |

10AM EST |

|

14 |

LAX & EUDA Health Merger Vote |

11/10/2022 |

10AM EST |

|

15 |

GACQ & Luminex, GP Global Merger Vote |

11/10/2022 |

11AM EST |

|

16 |

DKDCA: Extension Vote |

11/11/2022 |

|

|

17 |

ENCP Deadline extension vote |

11/11/2022 |

9AM EST |

|

18 |

LMACA Deadline acceleration vote |

11/14/2022 |

9:30AM EST |

|

19 |

FLAC: Merger Vote: NewAmsterdam Pharma Holding B.V. |

11/15/2022 |

|

|

20 |

ARBG Deadline extension vote |

11/15/2022 |

10AM EST |

|

21 |

KWAC Deadline extension vote |

11/15/2022 |

10AM EST |

|

22 |

IRRX Deadline extension vote |

11/15/2022 |

10AM EST |

|

23 |

IACC: Liquidation Vote Date |

11/17/2022 |

|

|

24 |

GLBL & Tiedemann Group & Alvarium Investments Merger Vote |

11/17/2022 |

10AM EST |

|

25 |

PTIC: Merger Vote: Appreciate |

11/18/2022 |

|

|

26 |

OHPA Accelerated Liquidation Vote |

11/21/2022 |

12PM EST |

|

27 |

POND: Merger Vote: MariaDB Corp AB |

11/22/2022 |

|

|

28 |

CNGL Deadline extension vote |

11/22/2022 |

10AM EST |

|

29 |

GBRG Deadline extension vote |

11/23/2022 |

10AM EST |

|

30 |

OTEC Deadline extension vote |

11/23/2022 |

10AM EST |

|

31 |

CRU Accelerated Liquidation Vote |

11/28/2022 |

12PM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

|

Chart 13: SPAC Activity by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

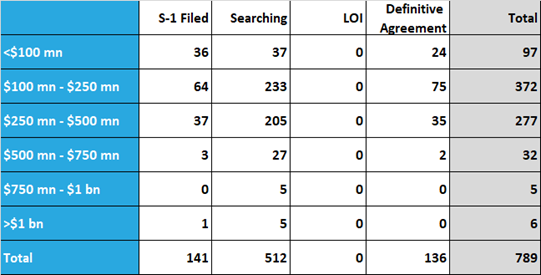

Chart 14: Current Status of the SPAC Universe |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 15: Current Status of SPAC Universe by Trust Size |

|

|

Source: Intro-act, Boardroom Alpha

|

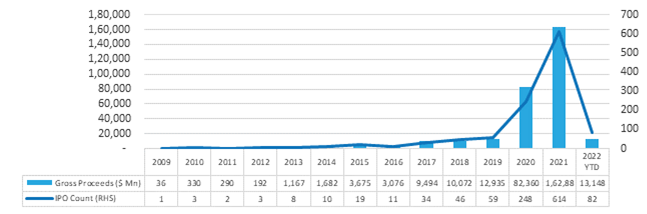

Chart 16: SPAC Transactions by Year |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 17: Average SPAC IPO Size ($ Mn) |

|

|

Source: Intro-act, Boardroom Alpha

|

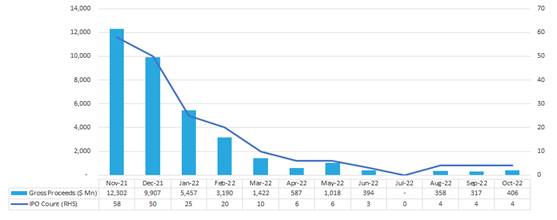

Chart 18: SPAC Transactions by Month (LTM) |

|

|

Source: Intro-act, Boardroom Alpha

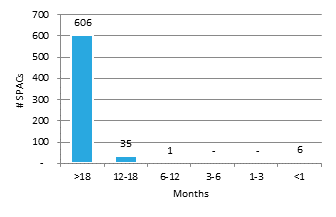

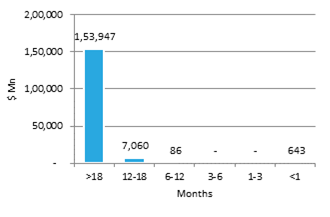

|

Chart 19: Time to Liquidation ' By Volume |

|

Chart 20: Time to Liquidation ' By Trust Value |

|

|

|

|

Source: Intro-act, Boardroom Alpha

|

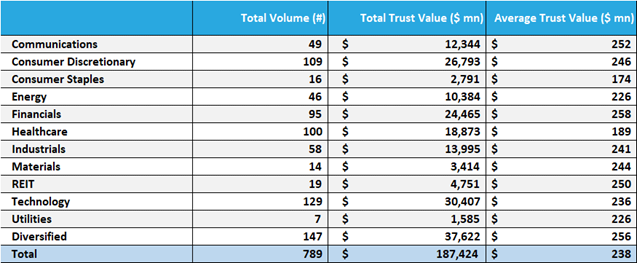

Chart 21: Active SPACs By Sector (As of Month Ending October 2022) |

|

|

Source: Intro-act, Boardroom Alpha

|

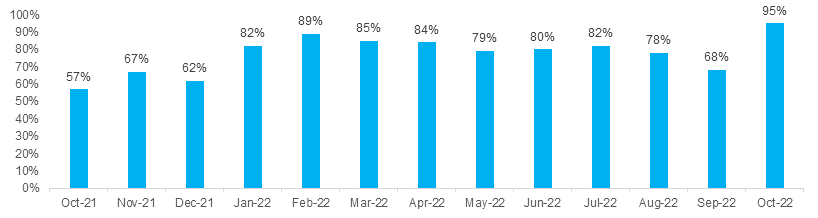

Chart 22: Average Redemption Rate by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 23: SPAC Redemption Detail ' October 2022 |

||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 24: Monthly SPAC Activity ' October 2022 |

|

|

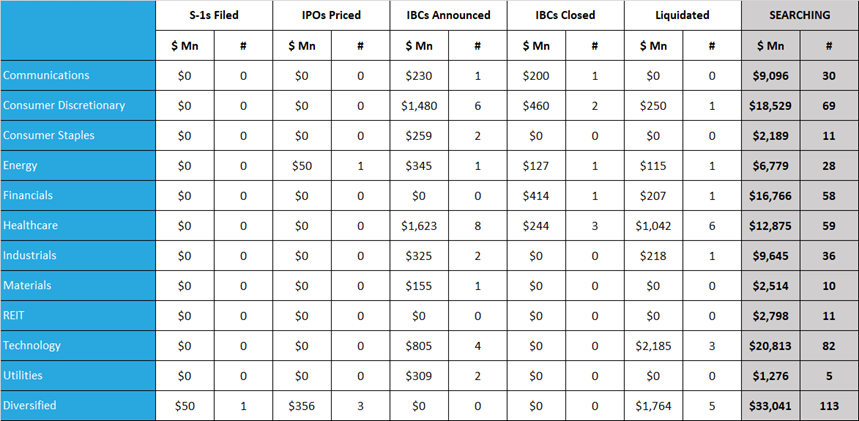

Source: Intro-act, Boardroom Alpha. Searching figures ($Mn and Count) are as of month end.

|

Chart 25: SPAC IBC Announcements by Target Sector ' October 2022 (1/3) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 25: SPAC IBC Announcements by Target Sector ' October 2022 (2/3) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 25: SPAC IBC Announcements by Target Sector ' October 2022 (3/3) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

The SPAC and New Issue ETF (SPCX). SPCX gives investors exposure to a broad portfolio of SPACs with the familiar attributes of an exchange traded fund's diversity, tax efficiency and liquidity. SPCX is the first actively managed SPAC ETF. Why active? As the SPAC market is rapidly evolving, we believe that the portfolio management approach should equally reflect the dynamic nature of this burgeoning capital-raising alternative. This is no place for a rigid rules-based index strategy.

|

Chart 26: SPCX Summary Data |

|

Chart 27: SPCX Top 10 Holdings |

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

Source: Intro-act, ETF.com. Data as of 10/31/22.

|

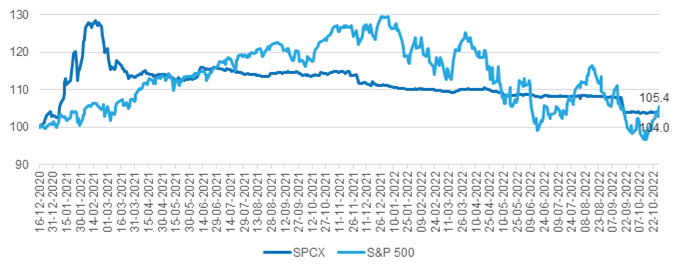

Chart 28: SPCX Performance |

|

|

Source: Intro-act, Yahoo! Finance. Data as of 10/31/22.

|

Chart 29: Relative-SPAC Index vs Russell 3000 |

|

|

Source: Intro-act, FactSet

|

Chart 30: Relative-IBC Index vs Russell 3000 |

|

|

Source: Intro-act, FactSet

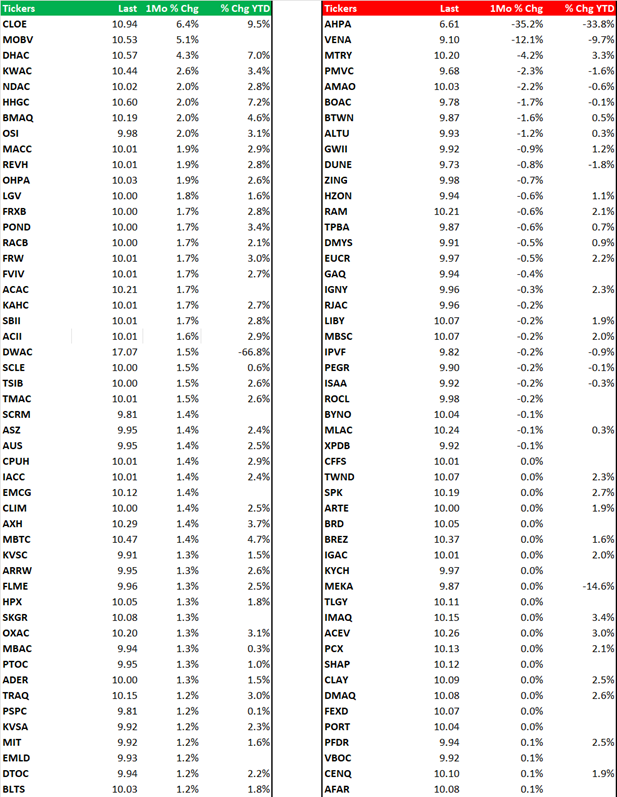

|

Chart 31: Gainers and Losers in the Broader SPAC Universe (% Change) |

|

|

Source: Intro-act, FactSet

|

Chart 32: SPAC IPO Pricings by Sector ' October 2022 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 33: SPAC S-1 Filings by Sector ' October 2022 |

||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 34: SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 35: DE-SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 36: SPAC Underwriter League (YTD 2022 ' As of October End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Bookrunner Volume ($ Mn) is based on the total amount of the offering sold, including over-allotment. Full credit is awarded to the sole book-runner or split equally among joint book-runners.

|

Chart 37: Top De-SPAC Advisors (YTD 2022 ' As of October End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Advisor credit is shared equally among all advisors on a given deal, as a proportion of the enterprise value of the target company acquired by the SPAC. Firms with multiple advisory roles receive credit for each role.

|

Chart 38: SPAC Legal League (YTD 2022 ' As of October End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Volume ($ Mn) is awarded to both Issuer and Underwriter Counsel.

|

Chart 39: SPAC Auditor League (YTD 2022 ' As of October End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research

|

Chart 40: ICR ' The Leading SPAC Communications and Capital Markets Advisor |

|

113 Transactions / $267 Billion in Transaction Value Since 2021

|

Source: Intro-act, ICR. Announced SPAC transactions since 2021, All Announcements not shown. Data as of April 2022.

Analyst Certification

I, Peter Wright, certify that the views expressed in the research report accurately reflect my personal views about the subject securities or issues. I also do not receive direct or indirect compensation based on my recommendations or views.

Intro-act, Inc. (Intro-act) issued this report and may seek fees for the assistance with investor targeting, access, and further investor preparation services. Intro-act, Inc. will not seek renumeration for any investment banking service or investment advice.

Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources who are believed to be reliable. However, the issuer and related parties, as well as Intro-act, do not guarantee the accuracy or completeness of this report, and have not sought for this information to be independently verified. Opinions contained in this report represent those of the Intro-act analysts at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, and estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties, and other factors that may cause the actual results, performance, or achievements of their subject matter to be materially different from current expectations.

Exclusion of Liability: To the fullest extent allowed by law, Intro-act, Inc. shall not be liable for any direct, indirect, or consequential losses, loss of profits, damages, or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this note.

No personalized advice: The information that we provide should not be construed in any manner whatsoever as personalized advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Intro-act's solicitation to affect, or attempt to affect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors.

Investment in securities mentioned: Intro-act has a restrictive policy relating to personal dealing and conflicts of interest. Intro-act, Inc. does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees, and contractors of Intro-act may have a position in any or related securities mentioned in this report, subject to Intro-act's policies on personal dealing and conflicts of interest.

Copyright: Copyright 2022 Intro-act, Inc. (Intro-act).

Intro-act is not registered as an investment adviser with the Securities and Exchange Commission. Intro-act relies upon the 'publishers' exclusion' from the definition of investment adviser under Section 202(a) (11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Intro-act does not offer or provide personal advice, and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell, or hold that or any security, or that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.