DEAL IN FOCUS: ATLASCLEAR – QUANTUM FINTECH ACQUISITION CORP. (QFTA)

AtlasClear Holdings plans to build a cutting-edge technology enabled financial services firm that would create a more efficient platform for trading, clearing, settlement and banking, with evolving and innovative financial products that focus on financial services firms. Formed in October 2022, AtlasClear will be a fintech driven business-to-business platform that will power innovation in fintech, investing, and trading. It expects to be positioned to provide a modern, mission-critical suite of solutions to its prospective clients, enabling them to reduce their transactions costs and compete more effectively in their businesses. AtlasClear’s target client base for its prime banking and prime brokerage services will include financial services firms, generally with annual revenues up to $1 billion, including brokerage firms, hedge funds, pension plans, and family offices that are not adequately served by existing larger correspondent clearing firms and banks that have raised their minimums to a point where it is difficult for this segment of the market to meet the requirements for access to their clearing offerings. Smaller financial services firms are thus forced to find alternative solutions to continue to service their client bases. The practice of obtaining these services through intermediaries (often referred to as piggy-backing) results in additional fees and a loss of transparency and control for such financial services firms. As a result, such financial services firms are ideal clients for the “one stop shop” solutions Atlas’ integrated business model intends to provide. Per a 2022 IBIS World Industry Report, the estimated total revenue of the execution, clearing, and prime services industry is $159 billion.

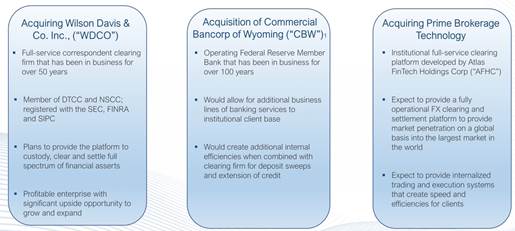

n Through the acquisitions of Wilson-Davis, a correspondent clearing company, and Commercial Bancorp, a federal reserve member, AtlasClear expects to acquire the capabilities to provide specialized clearing and banking services to financial services firms, with an emphasis on global markets currently underserviced by larger vendors. Once integrated, anticipated synergies between Commercial Bancorp and Wilson-Davis are expected to allow for lower cost of capital, higher net interest margins, expanded product development and greater credit extension.

n In addition, the technology platform that AtlasClear plans to develop and integrate following the acquisition of the Pacsquare Assets and the Fintech Assets will be cutting-edge, flexible, and scalable. Unlike other companies that are beholden to legacy technology stacks, that may struggle to keep pace with rapidly evolving client and customer expectations in an ever-increasing digital world, AtlasClear’s platform is anticipated to be modern, nimble, and unencumbered.

|

Chart 1: AtlasClear Management is Cultivating a Unique FinTech Opportunity |

|

|

Source: Intro-act, QFTA/Company Investor Presentation. 1 - Definitive agreement in place to acquire Commercial Bancorp and its bank subsidiary. Acquisition would occur after closing of Business Combination and is subject to, among other things, regulatory approval.

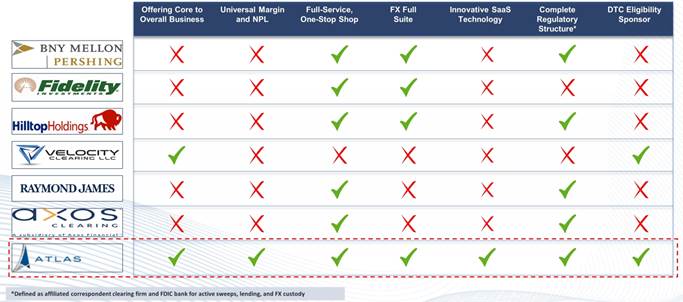

AtlasClear’s positioning as a one-stop-shop for Fintech and Regtech solutions differentiates the company from its competitors. Once integrated, AtlasClear’s technology platform and specialized clearing and banking services will be mission-critical to its clients, given the complexities of investing infrastructure, the complications around collateral and capital requirements, and the complicated regulatory landscape. The company expects to benefit as new fintech firms launch and existing firms scale, potentially outpacing legacy financial firms in their own categories. Consumer expectations for a one-stop shop for their investing, banking, spending, insurance and borrowing needs are driving the convergence of financial services. As a result, financial companies that traditionally operated as single-product specialists (e.g., savings-focused platform, lending-focused platform) are now seeking to integrate trading and investing capabilities into their broader offering. AtlasClear also anticipates increased interest from non-financial services firms (e.g., consumer retail firms) in leveraging their brand and customer reach to offer financial services as a means to drive incremental revenue and customer engagement. AtlasClear will be well positioned to provide the “investing-as-a-service” platform these firms require to develop such offerings. In addition, incumbents in the wealth ecosystem, such as traditional wealth advisors, are trying to modernize their investment management offerings and better meet the digital demands of their existing end customer and potential customers. Following its anticipated acquisitions, AtlasClear expects to have the technology stack to provide such solutions and help automate their legacy infrastructure and eliminate their existing paper-based processes.

|

Chart 2: AtlasClear Capabilities Would Answer Unmet Needs Compared to Competitors |

|

|

Source: Intro-act, QFTA/Company Investor Presentation

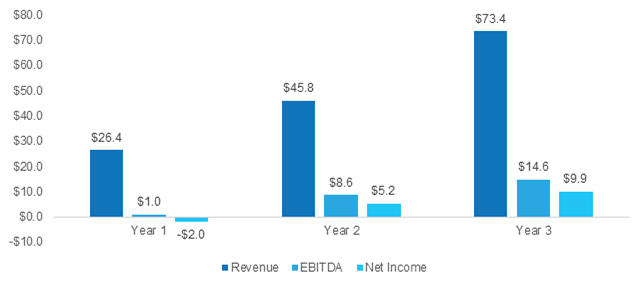

Strong competitive positioning and a well-rounded growth strategy is expected to drive rapid and profitable growth in fundamentals. AtlasClear’s growth strategy includes 1) growing its base of prospective clients organically and through channel partners; 2) growing its prospective clients’ revenue by providing them the tools to streamline the complex aspects of custody clearing and banking; 3) pursuing potential international expansion opportunities, starting with international clients seeking to access U.S. markets; and 4) identifying and executing strategic acquisitions to enhance its product capabilities, client reach, scale, etc. Through a combination of these factors, the company expects to grow its revenue from $26.4 million in Year 1 to $73.4 million in Year 3. EBITDA is anticipated to expand from ~$1 million to $14.6 million in the same time frame while net income is expected to reach ~$10 million by the end of Year 3. Thanks to its compelling business model, AtlasClear’s margins (EBITDA and net income) are expected to expand meaningfully between Year 1 and Year 3.

Chart 3: AtlasClear – Projected Financials ($ Millions) |

|

|

Source: Intro-act, Calculator New Pubco, Inc. form S-4 page 109 (May 5, 2023)

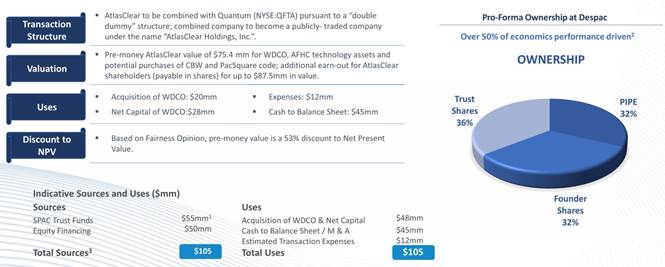

In November 2022, FinTech Acquisition Corporation (QFTA) entered into a definitive business combination agreement that is expected to result in Atlas FinTech Holdings Corp. transferring its trading technology assets to AtlasClear and the acquisition by AtlasClear of Wilson Davis & Co., Inc., a correspondent clearing broker-dealer, pending required regulatory approvals. AtlasClear has also entered into a definitive agreement to acquire Commercial Bancorp of Wyoming, a federal reserve member, following consummation of the initial business combination, which is expected to close in the second or third quarter of 2023, pending required regulatory approvals.

|

Chart 4: Transaction Summary – Mindful Structure for Potential Post Close Performance |

|

|

Source: Intro-act, QFTA/Company Investor Presentation. 1 - Assumes no redemptions, 2 - Does not give effect to the warrants, 3 - Does not include ELOC or similar products.

DEAL IN FOCUS: iLEARNINGENGINES – ARROWROOT ACQUISITION CORP. (ARRW)

Founded in 2010, iLearningEngines is the market leader in cloud-based, AI driven mission critical training for enterprises. Productizing enterprise knowledge has significant impact on business success in a globally distributed work environment and remains a fundamental challenge given the sheer volumes of content and data. This is the problem that iLearningEngines solves. Uniquely positioned at the intersection of two massive, rapidly growing global markets – global e-Learning and global AI systems, each with an estimated total addressable market of greater than $200 billion by 2025 according to Technavio and IDC MaturityScape – iLearningEngines leverages its AI and machine learning to build Intelligent “Knowledge Clouds” from an organization’s internal and external content and data, creating a central repository of all enterprise intellectual property, and then distributes knowledge into enterprise workflows to drive autonomous learning, intelligent decision making , and process automation.

The company has grown rapidly since its initial product launch with customers across a diverse set of industries and geographic regions. It currently serves 12 core verticals, including industrials, oil & gas, education, healthcare, and insurance. Key business and company highlights include:

n Powering over 1000 end-customers with over 3.2 million users

n $309 million in revenue in 2022, up 42% year over year, and positive adjusted EBITDA the past 3 years

n Net dollar retention of 119% with typical customer contract length of 3-5 years

n Proprietary AI platform and highly specialized learning and engagement data sets

n Over 100,000 research and development hours

n Top 20 in Deloitte Fast 500 for four years in a row, including #5 in 2019

n Rule of 40 software business consistently for the past 5 years

|

Chart 5: iLearningEngines (iLE) Overview and Platform |

|

|

Source: Intro-act, ARRW/Company Investor Presentation

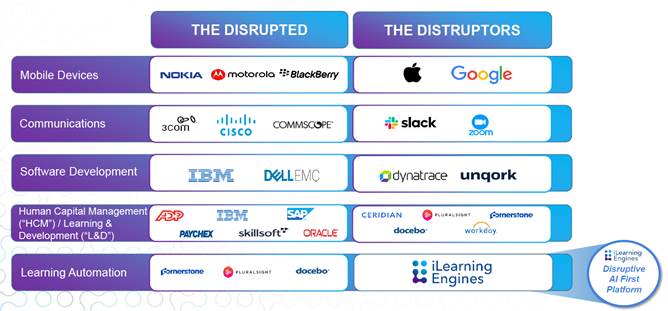

As an early pioneer in enterprise AI and its application in learning and process automation, iLearningEngines is in a strong position to disrupt the learning automation market. iLearningEngines occupies a unique space with first mover advantage and significant moats built around specialized learning and engagement data sets – the company has more than 10 years of experience in AI learnings and has over 100,000 engineering research and development hours invested in creating one of the biggest independent AI focused software platform companies in the world. It owns 40+ proprietary algorithms and has 3.2 million+ users, demonstrating iLE’s experience of operating at scale. Going forward, the company has multiple accelerators that will drive growth: 1) No Code AI Canvas, which streamlines enterprise integrations and delivers scale, and encompasses neural networks, among others, 2) Extensive Integrations across systems capturing event triggers, employee interactions and risk data,which form the basis of designing workflows, distributing learning automation and driving outcomes, 3) Document Augmentation, which enables AI-powered natural language understanding and drives automatic intent identification and disambiguation, 4) Video/Audio Content Augmentation, which generates text transcript for audio and video content, among other things, 5) Learnings Prescriptions – knowledge cloud and AI assist bots, and 6) data sets, event triggers, and engagement signatures. These accelerators will ensure that iLearningEngines remains at the forefront of disruption in the learning automation space.

|

Chart 6: iLearningEngines – Disrupting Industry with Legacy Players |

|

|

Source: Intro-act, ARRW/Company Investor Presentation

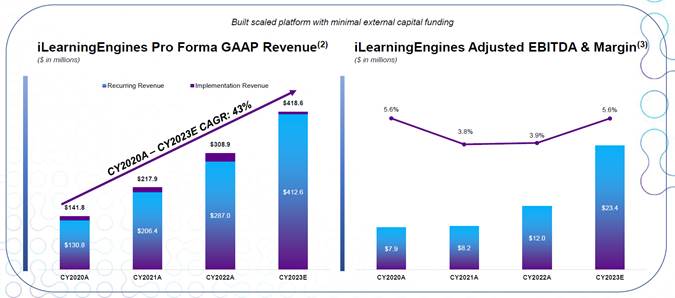

In addition to its technological expertise, the company also has a robust business model, reflected in the strong and profitable growth in the last few years – a standout feature among DE-SPACs going public. iLearningEngines ended 2022 with a topline of $308.9 million and is estimated to record $418.6 million in revenue this year, implying a CAGR growth rate of 43% between 2020 and 2023E. This growth is being driven by the company’s Annual Recurring Revenue (ARR) which has grown fast as the business further penetrates existing clients and verticals while expanding with new logo signings. ARR growth is expected to remain strong as the company expands its product pipeline, enters new verticals, expands geographically, grows in existing verticals, and benefits from significant growth in the digital learning market. This topline growth is being accompanied by improving profitability – the company’s EBITDA margin is expected to expand 170bps y/y to a four-year high of 5.6% and will benefit from operating leverage as iLearningEngines’ R&D spend (as a % of revenue) goes down. Future growth will be driven by a focused go-to-market strategy focused on 1) expanding direct sales infrastructure, 2) expanding target verticals, 3) proof of concept based selling, 4) contribution from acquisitions that can provide additional platforms to provide additional functionality to applications and penetrate additional markets and verticals, and 5) build of the iLE inside ecosystem.

|

Chart 7: iLearningEngines – Proven Profitable Revenue Growth Profile |

|

|

Source: Intro-act, ARRW/Company Investor Presentation

iLearningEngines is going public through a SPAC deal with Arrowroot Acquisition Corp. (ARRW), in a deal that values the company at $1.4 billion (3.3x 2023E revenue). On April 27, iLearningEngines announced that it has entered into a merger agreement with Arrowroot Acquisition Corp. (NASDAQ:ARRW), a publicly traded special purpose acquisition company sponsored by Arrowroot Capital, a 10 year old private equity firm specializing in enterprise software. The agreement includes a minimum cash requirement of $100 million that will be funded through several sources. The combined entity will receive approximately $43 million from Arrowroot Acquisition Corp.’s trust account, assuming no redemptions by Arrowroot Acquisition Corp.’s public stockholders. iLearningEngines will receive proceeds of a private convertible offering with participation from Arrowroot Capital and other institutional investors at the time the transaction is announced. iLearningEngines is also in discussions to raise additional capital via institutional investors. The intended use of cash is primarily for M&A and growth.

n Upon closing of the transaction, the combined company will be named iLearningEngines, Inc., and is expected to remain listed on the NASDAQ under the new ticker symbol, ‘AILE’.

n The combined company will continue to be led by iLearningEngines’ existing CEO and founder, Harish Chidambaran.

n The transaction has been unanimously approved by the Board of Directors of Arrowroot Acquisition Corp., as well as the Board of Directors of iLearningEngines, and is subject to the satisfaction of customary closing conditions, including the approval of the stockholders of Arrowroot Acquisition Corp.

Q&A OF THE MONTH – TIMOTHY (TIM) P. MORAN, PRESIDENT AND CHIEF EXECUTIVE OFFICER, AVERTIX

Avertix President and CEO Timothy Moran talks about his background, the company’s history and target market, its pipeline, the SPAC deal with BIOS Acquisition Corporation (BIOS), and what makes Avertix a good investment.

Q: Tim tell about your background and how you became CEO of Avertix?

A: I have spent the last 25+ years in medical devices and technologies. I was introduced to the space at an early age by a close family member who spent many years in cardiology commercialization, and from there decided it would be an exciting career path. I spent my first 18 years at Covidien, a global medical device manufacturer, which was later acquired by Medtronic. I then moved to a smaller organization, and really enjoyed the entrepreneurial environment. For the past 4 plus years, I had been running a Nasdaq listed medical device company with about 50 employees. In a smaller company, you can really shape the culture of the organization and I find that to be very rewarding.

For additional background I went to The State University of New York (SUNY) at Geneseo. After graduation, my first job was as a sales representative for Pitney Bowes Corporation, selling digital dictation and transcription systems to hospitals and physicians.

When I was approached about the opportunity to lead Avertix, I was immediately attracted to the mission-driven culture. Avertix is a medical device and technology company, which I believe is poised to revolutionize patient monitoring and cardiac care. Heart disease continues to be a leading cause of death and places a tremendous burden on healthcare systems. Our goal is to change the standard of care for patients who have suffered a prior heart attack. We can help reduce the constant fear and anxiety they encounter, and allow them the peace of mind needed to live a normal life. It is a truly exciting mission to have the opportunity to lead.

Q: How did you build Avertix? And what is your background in science and healthcare?

A: Embarking on a mission to save lives, Avertix set out to develop a user friendly, patient specific platform for heart attack detection and alerting. Founded in the early 2000’s, Avertix has invested the time and resources necessary to bring the Guardian to market. Our product, the Guardian, is an implantable device designed to provide early detection and alerting for patients at risk of a recurrent acute coronary events, such as heart attack. Guardian continuously monitors key cardiac parameters and alerts patients and healthcare professionals in real-time when there are signs of potential cardiac events. Early detection enables early intervention potentially saving lives and preventing severe damage to the heart.

Following the development phase for class III implantable PMA devices, Avertix was approved by the FDA for the Guardian, its first “commercial ready” device in Q3 2021. Shortly thereafter, in January of 2022, the Centers for Medicare & Medicaid Services (CMS) reviewed the Guardian and awarded Avertix with reimbursement under the Transitional Pass-Through Payment. With these critical regulatory and reimbursement milestones secured, Avertix is now focusing on accelerating its investment in leadership and commercial footprint to deliver the Guardian to patients.

Q: Who will Avertix serve? / Tell me about your patient population?

A: In the U.S. alone there are over 8 million heart attack survivors. Additionally, 800,000 heart attacks, including first and repeat attacks, will occur annually in the U.S. While ALL patients who have previously experienced a heart, attack are considered high risk, about 25% are at even greater risk due to comorbidities such as diabetes, renal insufficiency, and obesity. We see that portion of the patient population as our initial target market.

Q: How big is the market?

A: We believe that the market for the Guardian is substantial because cardiovascular diseases, including heart attacks, are a significant global health concern and the cardiac monitoring market is projected to grow significantly in the coming years. We are initially targeting the high-risk segment I mentioned, which in of itself represents an opportunity exceeding $2 billion in U.S. alone. And, in terms of geographic expansion opportunities, we believe the opportunity outside of the U.S. is approximately 7.5x the size of the U.S. opportunity.

Q: Do you have direct competitors? Can you name them?

A: Because the Guardian is the only FDA-approved Class III implantable device designed to detect acute coronary syndrome (ACS) events, like heart attacks, we believe there is limited direct competition. The Guardian also provides a series of secondary functionalities, including cardiac monitoring. While there are several medical devices that have been cleared by FDA in the cardiac monitoring market, none are approved to monitor the ST segment or alert patients to detected potential coronary occlusions like the Guardian is. For those reasons we believe the Guardian is the only viable solution for continuous, ambulatory ACS and heart attack monitoring.

Q: What does the company’s pipeline look like?

A: Over the next few years, we expect sales to continue to grow quickly, and our management projects our pro forma revenue will reach $75 million by the end of 2025. This projection assumes the creation and deployment of a nationwide sales team covering 200+ accounts, made up of primarily Ambulatory Surgery Centers, or ASCs, and hospitals. In addition, we have already secured committed distribution agreements in select OUS geographies.

Q: Earlier this month Avertix signed a business combination agree with a SPAC, where Avertix will be listed as a publicly traded company at closing. What was the motivation to go public by a business combination with a SPAC?

A: The decision to pursue a business combination through a special purpose acquisition company (SPAC) was driven by several factors. We believe becoming a publicly listed company through a business combination with a SPAC will (i) allow us to access the capital markets efficiently, (ii) provide us with the necessary resources to accelerate our growth initiatives, (iii) expand our market reach, and (iv) allow us to invest in research and development. In addition to the benefits of becoming a publicly listed company though a business combination with a SPAC, I specifically like partnering with Bioplus Acquisition Corp. (“BIOS”) and Explorer Acquisitions. They have extensive experience and a proven track record in the medical device and biotech space. They are bringing strategic value and knowledge to help guide our business and they are looking to be our long-term partner beyond the closing to position Avertix to flourish and succeed as a public company. We believe becoming a publicly listed company through a business combination the SPAC offers flexibility, allowing us to focus on executing our business plans while creating long-term value for our shareholders, and we believe we found the optimal partners in the process.

Q: Prior to the announcement of the business combination, you rebranded – how did you turn the concepts and marketing materials around so quickly?

A: We achieved a rapid turnaround in our rebranding to Avertix by forming a dedicated team, led by Holly Windler, our talented Senior Vice President of Global Marketing. Holly led the charge, collaborating with select external partners, implementing an efficient project management plan, and quickly iterated on customer feedback. This collaborative approach allowed us to streamline the process, ensure alignment with our vision for the brand, and execute in rapid fashion.

Q: Why do you believe that Avertix a good investment?

A: I believe that Avertix is a compelling investment due to our innovative and disruptive technology, with first mover advantage of the Guardian being the first and only FDA approved Class III implantable heart attack detection and early warning system. We operate in a large and growing market, with a competitive advantage supported by advanced technology and a robust intellectual property portfolio. Avertix is led by a proven medical device leadership team.

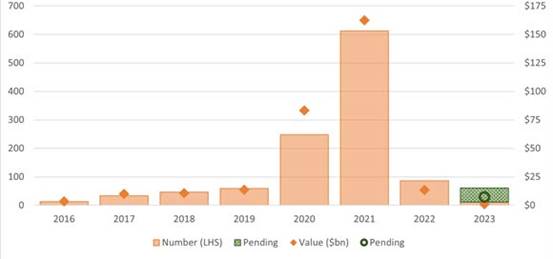

U.S. SPACs continue in the IPO slow lane. The slump in new IPOs for U.S.-based SPACs has stretched into the first quarter of 2023, according to a report by S&P Global Market Intelligence. Even though SPACs, have been around for decades, the method of taking a firm public boomed for a while, peaking during Q1 of 2021 when 278 firms went public via SPACs representing $278 billion in aggregate value. Things began to slow following the scrutiny of regulators followed by the flagging economy. The report shares that broader M&A activity is showing some signs of life after a slowdown in 2022. A recent count of 15 SPACs nearing their expirations included those targeting deals in Fintech, software, healthcare, and consumer spaces. The value of those offerings ranged from the $58.3 million offered by DILA Capital Acquisition Corp. to $345.0 million from Post Holdings Partnering Corp. Read More (Crowd Fund Insider)

State of the SPAC market. The volume of SPAC IPOs and mergers has reverted to pre-hype levels. Funding from public and private investors has plunged, while redemptions by existing investors have increased sharply. The outlook for SPACs is far more muted than in the past few years, according to Seeking Alpha. They expect a return to a far smaller level of issuance, deal making and execution as the space bears more scrutiny from sponsors, investors and regulators alike. There will still be opportunities – albeit a fraction of recent volume – for seasoned, sophisticated investors to take advantage of in 2023, due to the smaller market size, a decrease in competition for deals, fewer sponsors and stronger companies coming to market. Read More (Seeking Alpha)

|

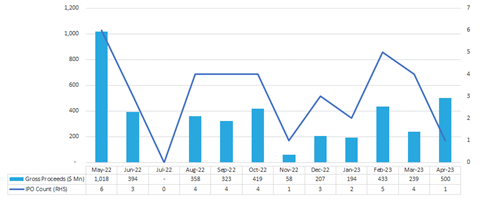

Chart 8: U.S.– SPAC IPOs |

|

|

Source: Intro-act, Seeking Alpha

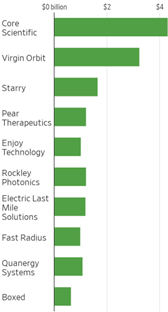

SPACs delivered easy money, but now companies are running out. The SPAC boom took hundreds of risky companies to the stock market. The next stop for many is bankruptcy court. Dozens of companies that merged with SPACs are running out of cash, joining at least 12 that have already gone bankrupt after combining with special-purpose acquisition companies. More than 100 companies, including electric-scooter firm Bird Global Inc., smart-sock baby-monitor maker Owlet Inc. and electric-car startup Faraday Future Intelligent Electric Inc. are running out of cash, according to an analysis of the companies’ cash and cash flow from operations data disclosed in regulatory filings. Shares of many of these companies’ trade under $1, more than 90% below where they did when they went public, and are in danger of being delisted. Read More (The Wall Street Journal)

|

Chart 9: Approximate Valuation of Now Bankrupt Companies at Time of SPAC Merger |

|

|

Source: Intro-act, The Wall Street Journal

As SPAC boom subsides, some de-SPACed companies seek Chapter 11 protection. The boom in SPAC IPOs in 2020 and 2021 led to hundreds of de-SPAC mergers. Many were early-stage tech or biotech enterprises that had not yet achieved profitability and have struggled to remain viable as capital markets tightened. Some of those companies with debt or other significant liabilities have turned to Chapter 11 bankruptcy for its flexibility in restructuring their obligations and preserving the value of their businesses as a going concern. Read More (Lexology)

Branson’s rocket-launch firm Virgin Orbit files for bankruptcy. Virgin Orbit Holdings filed for bankruptcy after the satellite launch firm tied to British billionaire Richard Branson failed to secure the funding needed to keep operating and cut about 85% of its staff. The company listed $243 million in assets and $153.5 million for its total debt in a Chapter 11 petition filed in Delaware. Virgin Orbit merged with NextGen II in December 2021. That deal netted just $67.8 million for the company, significantly less than expected, CEO Dan Hart said in a court filing. In fact, the deal was expected to fetch up to $383 million of cash held in the NextGen II trust, which assumed no redemptions, and a $100 million fully committed PIPE. Read More (Bloomberg)

Online bulk retailer Boxed files for chapter 11 bankruptcy a year after SPAC deal. Boxed, an online bulk retailer that thrived during the pandemic, filed for bankruptcy. The New York-based firm listed as much as $102.6 million in assets and up to $190.4 million in liabilities in a Chapter 11 petition filed in the district of Delaware. Founded in 2013, the company went public in December 2021 by combining with Seven Oaks Acquisition. At deal announcement in June 2021 the company was valued at $900 million. Read More (Bloomberg)

BuzzFeed news shutting down 16 months after SPAC deal. BuzzFeed News is being shuttered, with HuffPost remaining as the only news brand for the media company BuzzFeed, according to multiple news reports. The company went public via a SPAC just 16 months ago. CEO Jonah Peretti sent a memo to staff, outlining the shutdown of BuzzFeed News, saying the company can “no longer afford to fund” the news section as a “standalone organization” and cutting the workforce by 15%, or 180 staffers, across its business, content, tech and admin teams. Additionally, the company’s chief revenue officer Edgar Hernandez and COO Christian Baesler will both leave the company. BuzzFeed president Marcela Martin will take over all revenue functions effective immediately. Read More (DealFlow’s SPAC News)

SPAC mergers with public companies: A new trend? Bull Horn Holdings Corp., a special purpose acquisition company, merged with Coeptis Therapeutics, Inc., a publicly traded biopharmaceutical company developing cell therapy platforms for cancer, in October 2022. In January 2023, TKB Critical Technologies 1, a SPAC focused on investing in critical technologies, announced a merger with an already public company, Wejo, which had gone public via an earlier merger with another SPAC. The fact that some SPACs are acquiring public companies is a topic that comes with interesting and timely questions. To sort out some of these legal, financial, and insurance issues, we sat down with two experts in the industry: James Hu, a partner in White & Case’s Global Mergers & Acquisitions Practice, and Mark Deters, an audit partner and SPAC team leader in Withum’s Financial Services Group. Read More (JD Supra)

SPAC to square one: The boom and bust of the blank cheque market. A morbid anniversary of sorts is upon us. Two years on from the SPAC boom of early 2021, and the chickens are coming home to roost for one of the costliest fads in recent history. SPACs were a major driving force behind the 2021 IPO boom, accounting for 61% of U.S. public listings in the year compared to 25% in 2020. By 2022, SPACs had already dwindled to 8% of new IPOs, leaving a trail of underperforming acquisitions and liquidated shell companies in their wake. One of the repercussions of the SPAC drain is the current boom in the take-private market, as PE managers sniff out devalued companies with the potential to turn them around as we head into the rebound stage of the bottomed-out capital markets. Read More (Proactive Investors)

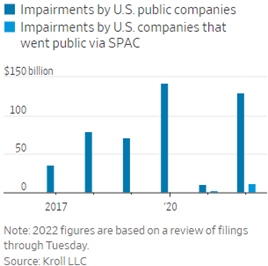

Companies that went public via SPACs log billions of dollars in goodwill write-downs. Companies that went public through mergers with special-purpose acquisition companies in recent years booked billions of dollars in goodwill write-downs in 2022, reflecting in part a reckoning of the heady premiums paid to secure deals during the SPAC boom. Some of the biggest goodwill impairments in 2022 came from SPAC-backed companies like cryptocurrency platform Bakkt Holdings Inc., business-services provider Advantage Solutions Inc., 3-D printing firm Fathom Digital Manufacturing Corp., self-driving vehicle startup Aurora Innovation Inc. and now-bankrupt bitcoin miner Core Scientific Inc., according to financial and risk advisory firm Kroll LLC. Each of these five companies’ pretax impairments exceeded $1 billion last year. Read More (The Wall Street Journal)

|

Chart 10: Writing it Down |

|

|

Source: Intro-act, The Wall Street Journal

Deal-needy SPACs scour the globe for targets as deadlines loom. SPAC sponsors are looking around the world for target companies as they scramble to meet deadlines amid the ongoing drought in the market for traditional initial public offerings. Nearly 300 SPACs face deadlines in the coming six months before dozens of sponsors may opt to throw in the towel and return cash to investors. Read More (Mergers&Acquisitions)

Can a deSPAC be used to combat counterfeit shares and naked short selling? One of the benefits of a stock acquisition is that it can help identify counterfeit shares in the market. Counterfeit shares are shares that are sold to investors but do not actually exist. This can happen when a short seller sells shares that they do not own, hoping to buy them back later at a lower price and pocket the difference. This practice, known as naked short selling, is illegal. When a company acquires another, it needs to buy the shares from the shareholders of record. This means that shareholders of record would have to reveal their identity in order to get the stock for the merger. This process can help identify counterfeit shares because the company can verify that the shareholders of record actually exist and that their shares are valid. Read More (The Basile Law Firm P.C.)

Perspectives: Special purpose acquisition companies – A closer look at recent lawsuits. In the early days of the COVID-19 pandemic, investors were drawn to special purpose acquisition companies. But just as the traditional IPO process raises the prospect of a new risk to the newly public company and associated federal securities litigation brought by its investors, the same is true for SPAC-related IPOs. As each suit is likely to be accompanied by a claim submitted to the SPAC’s directors and officers’ liability insurer, these investment vehicles represent significant exposure for both SPAC investors and D&O insurers. The surge of SPAC-related lawsuits and enhanced regulation materially detract from the appeal of a SPAC as an investment vehicle. Further, with the recent Delaware Superior Court ruling that a SPAC’s post-merger runoff policy provides coverage for the defense fees of former directors of the premerger target for alleged wrongful acts, the courts have interpreted D&O insurance coverage well beyond what was intended when the policies were priced. Read More (Business Insurance)

Corvex settles with SEC over SPAC activities. Corvex Management has agreed to pay $1 million to settle a Securities and Exchange Commission complaint related to the activities of three SPACs co-sponsored by the hedge fund. The regulator accused the activist hedge fund firm of failing to disclose conflicts of interest regarding its personnel’s ownership of sponsors controlling SPACs into which Corvex advised its clients to invest. Without admitting or denying the findings, Corvex agreed to a cease-and-desist order, a censure, and the $1 million civil penalty to settle the charges. Read More (SEC)

Southern district of New York dismisses putative class action arising from SPAC Merger, holding that plaintiffs lacked standing. Judge Ronnie Abrams of the US District Court for the Southern District of New York dismissed a putative class action arising out of a SPAC transaction that resulted in a consignment-to-retail used car marketplace becoming publicly traded. Plaintiffs asserted claims under the Securities Act of 1933 and the Securities Exchange Act of 1934 against the marketplace, the SPAC entity (Acamar Partners Acquisition), and related entities and individuals, alleging that they made misrepresentations regarding the marketplace’s business model. Read More (Lexology)

SPAC audits were hit-or-miss, oversight board inspections find. Nearly half of the audits of special purpose acquisition companies inspected by the U.S. accounting oversight board fell short of basic standards, the regulator said Wednesday. The Public Company Accounting Oversight Board reviewed 115 audits for SPACs and companies created through the merger of a SPAC with a private operating company as part of its reviews of U.S. auditors over the past two years. Inspectors found issues in 53 audits. In some cases, auditors missed material misstatements and failed to test assumptions that affected the valuation of certain liabilities known as warrants. Read More (Bloomberg Law)

PCAOB says firms are screwing up SPAC audits. A new report from the Public Company Accounting Oversight Board sheds light on an area where PCAOB inspectors have observed relatively high rates of audit deficiencies: SPACs. In recent years, the PCAOB has considered SPAC-related risks to investors as it has planned its inspections. PCAOB inspectors have once again included SPACs among their list of priorities for 2023 inspections, reports CPA Practice Advisor. From 2021 to 2022, PCAOB inspectors reviewed more than 100 audits of companies that were either considered SPACs or that were formed through a de-SPAC transaction. Read More (CPA Practice Advisor)

Digital World rushes to complete Trump Media deal. Nearly 18 months ago, an obscure investment banker unveiled a blockbuster deal: His SPAC would bankroll a social media outfit that former President Donald J. Trump planned to start with hundreds of millions of dollars. Today, the social media platform Truth Social has millions of users, including the former president, the New York Times notes. But the company that was supposed to bankroll it has been swarmed by federal investigators. In late March, the deal’s architect, Patrick Orlando, was ousted as CEO of Digital World Acquisition. Read More (The New York Times)

SPAC King Chamath Palihapitiya says higher rates have created ‘Wave of Destruction’ across whole sectors. Higher interest rates are sowing chaos across businesses and whole sectors of the market, according to “SPAC king” Chamath Palihapitiya. In an annual letter to investors, the Social Capital CEO leveled more criticism at the Federal Reserve over its aggressive rate hikes over the past year. The policy move has weighed heavily on risk assets, and helped burst the bubble in so-called blank-check firms that Palihapitiya rode during the pandemic boom of 2020 and 2021. “The amount of absolute value destruction, not just in companies, but entire sectors … was alarming,” Palihapitiya said, pointing to the decline in areas like crypto and special purpose acquisition companies, shell companies that raise capital to expedite the IPO of an existing company. Read More (Market Insider)

Billionaire Gores sued over United Wholesale Mortgage SPAC deal. An investor sued private equity billionaire Alec Gores and other architects of United Wholesale Mortgage’s SPAC merger, claiming they sold out ordinary shareholders because the deal’s lopsided structure gave them a windfall no matter how it fared. The lawsuit targets Gores Group affiliates backing Gores Acquisition IV that combined with the lender to take it public as UWM Holdings. It doesn’t name UWM or its billionaire CEO Mat Ishbia – who recently bought the NBA’s Phoenix Suns and the WNBA’s Phoenix Mercury – as defendants. The transaction’s backers “hastily negotiated the merger through a flawed and unfair process,” according to the suit filed in Delaware. Read More (Bloomberg Law)

AI-linked De-SPAC CXApp surges 1,480% in blistering three-day rally. CXApp extended its three-day surge to as much as 1,480%, riding a wave of retail investor interest after listing via a SPAC merger with KINS Technology Group. Formely Inpixon, now renamed CXApp Holding, the business combination was approved by KINS stockholders on March 10. The artificial intelligence-powered enterprise software company has jumped from $1.33 to as high as $21 without having released any new updates with the SEC in the period as it becomes the latest stock to ride the AI wave that’s boosted multiple companies this year. It was the most-mentioned stock over the past day in Stocktwits. Read More (Yahoo! Finance)

SeatGeek files confidentially for IPO following collapse of SPAC deal. Event ticketing company SeatGeek filed confidentially with regulators this month for an initial public offering. SeatGeek’s planned IPO follows its previous attempt to go public via a SPAC merger with RedBall Acquisition. Both parties agreed to terminate the deal last June due to market conditions. That merger would have valued SeatGeek at $1.35 billion and included investments from Kevin Durant’s Thirty-Five Ventures and Utah Jazz owner Ryan Smith. SeatGeek recently signed a reported $100 million deal to become MLB’s official ticket reseller. Read More (The Information)

Marley Spoon joining Frankfurt Stock Exchange via SPAC deal. Meal delivery service Marley Spoon and its advisers at Greenhill & Co have laid out a three-course meal for investors, serving a buyout bid from a Frankfurt-listed SPAC, an equity raising and debt relaxations. On the debt side, Marley Spoon’s primary lender Runway Growth Finance has extended maturities and agreed to an interest-only period. Marley Spoon and Greenhill have hammered out a takeover from a Frankfurt Stock Exchange-listed SPAC that’s related to its current investor 468 Capital. Read More (Financial Review)

IPO a No-Go: Volatile market leaves brands gun shy. Far from IPO fever, it seems fashion firms are being left out in the cold. According to experts, clothing brands and retailers aren’t expected to be big players in 2023’s initial public offering market. That’s no surprise given the tough market conditions. Moreover, the declines in valuation for fashion startups that have gone public could have investors thinking twice about making big bets in the sector. In the U.S. IPO market, Renaissance Capital in a report that the first quarter of 2023 didn’t deviate from 2022, which represented the slowest year in decades. It cited “hawkish signals from the Fed, renewed recession fears, and turmoil within the banking industry” as stumbling blocks. Read More (Yahoo! Finance)

Lower space company price tags pave the way to more acquisitions. A drop in space company valuations could open the door to more transactions in the industry, according to an April 17 Space Symposium panel on the outlook for deals, as long as they can navigate increasing regulatory scrutiny. “There were a lot of deals that we haven’t participated in over the last five years because the companies were overvalued,” said Megan Crawford, co-founder of venture capital firm SpaceFund. “I like to refer to this as the magic space sprinkles,” she said, “you add space, or AI, or blockchain to the name of your company and all of a sudden the valuation goes up by 100x.” She said this issue was compounded by a spurt of early-stage space companies that went public in recent years by merging with a special purpose acquisition company (SPAC), often with lofty business projections despite a lack of current revenues. Read More (SpaceNews)

Europe’s biggest SPAC will dissolve. The biggest blank-check company in Europe, backed by LVMH founder and world’s richest man Bernard Arnault, and former UniCredit chief Jean Pierre Mustier, is set to be wound up after failing to find a target in the financial services sector. Pegasus Europe announced that it will cease operations and is preparing to return capital to its investors at the beginning of May, subject to approval by shareholders. The SPAC floated on the Amsterdam exchange in December 2021, raising 200 million euros ($226 million). Read More (Financial Times)

First SPAC set up under new UK rules to close after failing to find merger target. The first company launched under newly relaxed rules to attract SPACs to London after Brexit has said it will shut down, without finding a suitable merger target. Hambro Perks Acquisition said in a statement that it had ceased all operations except for the purposes of winding up the company and returning money to shareholders. Sir Anthony Salz, the chair of the tech investment company, blamed “challenging circumstances” for stock market listings. In autumn 2021 Hambro Perks said it had raised £143.5 million ($178 million) from the stock market to find an investment target, slightly shy of the £150 million ($186 million) it had hoped for. However, Salz said the company would probably be unable to find a suitable target for acquisition before the end of a two-year deadline in November, after talks fell through this year with the drug developer Istesso. Read More (The Guardian)

Indonesian fintech DigiAsia Bios looks abroad after SPAC merger. Indonesian financial technology startup DigiAsia Bios is gearing up to expand to other Southeast Asian countries with similar demographics and regulations, including Vietnam, Cambodia and the Philippines, after its combination with a special purpose acquisition company (SPAC) and Nasdaq listing this year, a senior executive said. In an interaction with DealStreetAsia, DigiAsia founder Alexander Rusli said the business-to-business (B2B) company plans to complete its combination with StoneBridge Acquisition Corporation, a publicly traded special purpose acquisition company, this April and raise around $200 million. The money will allow DigiAsia to grow inorganically. Read More (Nikkei Asia)

Hong Kong SPAC pioneer calls for looser rules to revive market. One of the pioneers of blank-check companies in Hong Kong is urging local regulators to relax rules in order for more listings to happen, acquisitions to materialize and liquidity to improve. Jason Wong, one of the first financiers of special purpose acquisition companies in the Asian financial hub, said Hong Kong should align its SPAC rulebook to that in the more lightly regulated U.S. market, so as to attract stronger foreign demand. Changes needed include allowing retail investors to access SPAC offerings, boosting the proportion of embedded warrants and providing more clarity about who qualifies as a promoter. Trading in Hong Kong SPACs has been tepid. Only five blank-check firms listed in the city, and they barely trade. Read More (Bloomberg)

Mexico’s Covalto quietly delays Nasdaq listing via SPAC to 2024. Mexican digital and banking services platform Covalto has pushed back its much-anticipated plans to list on the Nasdaq exchange through a SPAC to 2024, according to an SEC filing. The company had initially sought to go public in the first quarter, seeking to be the first Mexican fintech to trade publicly on a U.S. exchange. The filing shows that Covalto and LIV Capital Acquisition II have agreed to extend the deadline for the merger from May 10 to Feb. 10, 2024. A source close to Covalto told Reuters that the merger is still in the works, with the delay simply down to lengthy regulatory processes with the SEC. Read More (Yahoo! Finance)

Bitdeer Technologies Group (BTDR) and Blue Safari Group Acquisition Corp. complete business combination. Bitdeer Technologies Group, a world-leading technology company for the cryptocurrency mining community, and Blue Safari Group Acquisition Corp. (NASDAQ: BSGA), a special purpose acquisition company, completed their announced business combination. Bitdeer’s Class A ordinary shares started trading on the Nasdaq under the ticker symbol “BTDR” on April 14, 2023. Bitdeer handles complex processes involved in mining such as miner procurement, transport logistics, mining datacenter design and construction, mining machine management and daily operations. Bitdeer has mining datacenters deployed in the U.S. and Norway. Read More (Globe Newswire)

Zapp Electric Vehicles Limited (ZAPP) and CIIG Capital Partners II, Inc. complete business combination. CIIG Capital Partners II, Inc., a Delaware corporation and a former U.S. publicly-listed special purpose acquisition company, closed its business combination with Zapp Electric Vehicles Limited, a private company limited by shares registered in England and Wales and a UK-based, high-performance two-wheel electric vehicle company. The combined company, Zapp Electric Vehicles Group Limited, a Cayman Islands exempted company, started trading of its ordinary shares and warrants on the Nasdaq Stock Market under the ticker symbols “ZAPP” and “ZAPPW”, respectively, on May 1, 2023. The business combination was approved by CIIG II stockholders at a special meeting held on April 14, 2023. Read More (Globe Newswire)

dMY Technology Group VI abandons Rainwater Tech deal, will liquidate instead. dMY Technology Group VI announced that its directors decided it would not be in the best interests of shareholders to proceed with a proposed merger with Rain Enhancement Technologies. Instead, the SPAC intends to dissolve and liquidate. No other details were offered. The news comes just days after the SPAC announced a forward purchase agreement for six million shares in support of the deal. In January, dMY launched a tender offer to purchase up to 24.15 million Class A shares to shore up the Rainwater Tech deal. The Austin, Texas-based target is engaged in the development and commercialization of rainfall generation technology. Read More (Business Wire)

DUET acquisition terminates AnyTech365 deal. Malaysia-based DUET Acquisition announced that it terminated a merger agreement with Anteco Systems, S.L (dba AnyTech365). DUET in a statement said it will seek an alternative business combination. AnyTech365 is engaged in IT security and support. The $287 million deal was announced last July. DUET raised $86.25 million in a January 2022 IPO to focus on disruptive change-maker technology enterprises that are capitalizing on the digital shift. Read More (Globe Newswire)

Cascadia acquisition terminates RealWear deal. Cascadia Acquisition announced that its business combination agreement with RealWear has been terminated. The press release disclosing the dead deal did not state whether the decision was mutual or what Cascadia’s next move might be. However, following a deadline extension vote in February, Cascadia disclosed that 14,710,805 shares were redeemed. That wiped out 78% of the 18.75 million shares outstanding. The $375.5 million deal was announced just two months ago. Cascadia at that time had $150 million of cash in trust, which it raised in an August 2021 IPO. Proceeds for the transaction were expected to consist of the remaining cash in trust following any redemptions and up to $35 million of additional financing. RealWear is a hands-free wearable tablet company that provides assisted-reality solutions for industrial use. Read More (Business Wire)

Flexjet agrees to terminate business combination with Horizon Acquisition Corp. II. Flexjet, Inc., a global leader in subscription-based private aviation has agreed to terminate its business combination agreement with Horizon Acquisition Corporation II, a publicly traded special purpose acquisition company, that would have resulted in Flexjet becoming a publicly listed company. As a result of the termination, Flexjet will remain a private company. Flexjet, Inc., a global leader in subscription-based private aviation, first entered the fractional jet ownership market in 1995. Read More (Business Wire)

Evo Acquisition Corp. announces termination of business combination agreement with 20Cube Logistics Pte. Ltd. Evo Acquisition Corp.(Nasdaq: EVOJ) announced that Evo, 20Cube Logistics Solutions Pte. Ltd., Hollis Merger Sub, Inc., 20Cube Logistics Pte. Ltd. and certain holders of outstanding shares of 20Cube Logistics Pte. Ltd. have mutually agreed to terminate their announced business combination agreement, effective as of April 25, 2023. The business combination agreement was signed on October 18, 2022. The parties have signed an agreement terminating the business combination agreement on mutually acceptable terms, which also makes void the ancillary documents. Read More (Globe Newswire)

Biometric start-up Elenium reportedly eyes $185 million SPAC deal. Elenium Automation is plotting a Nasdaq listing with help from a home-grown SPAC in a deal that the Melbourne digital identification start-up hopes will boost its valuation by 54% to $185 million. Elenium – which has developed software and hardware to check identities using face and palm biometrics deployed at 25 airports round the world – did not have to look far from home to find its blank-check backer in Integral Acquisition 1. Read More (Financial Review)

|

Chart 11: SPAC Events – May 2023 (1/2) |

|

S. No |

Event Name |

Date |

Time |

|

1 |

TMTC Unit Split |

5/1/2023 |

- |

|

2 |

ACAX Deadline extension vote |

5/1/2023 |

9AM EST |

|

3 |

VSAC Deadline extension vote |

5/1/2023 |

9AM EST |

|

4 |

LIVB Deadline extension vote |

5/1/2023 |

11AM EST |

|

5 |

BWAQ Deadline extension vote |

5/2/2023 |

9AM EST |

|

6 |

JUN Deadline extension vote |

5/2/2023 |

10AM EST |

|

7 |

JWAC & Chijet Motor Company Merger Vote |

5/2/2023 |

10AM EST |

|

8 |

INTE Deadline extension vote |

5/3/2023 |

9AM EST |

|

9 |

CNDB Deadline extension vote |

5/4/2023 |

11AM EST |

|

10 |

TGVC Deadline extension vote |

5/4/2023 |

12PM EST |

|

11 |

APGB Deadline extension vote |

5/5/2023 |

9AM EST |

|

12 |

VMGA Deadline extension vote |

5/5/2023 |

10AM EST |

|

13 |

PTWO Deadline extension vote |

5/5/2023 |

10AM EST |

|

14 |

NPAB Deadline extension vote |

5/5/2023 |

10:30AM EST |

|

15 |

MAQC Deadline extension vote |

5/5/2023 |

12PM EST |

|

16 |

HHLA Deadline extension vote |

5/9/2023 |

9:30AM EST |

|

17 |

RCFA Deadline extension vote |

5/9/2023 |

10:30AM EST |

|

18 |

DPCS Deadline extension vote |

5/10/2023 |

9AM EST |

|

19 |

VCXA Deadline extension vote |

5/10/2023 |

9AM EST |

|

20 |

CCVI Deadline extension vote |

5/11/2023 |

10AM EST |

|

21 |

NETC Deadline extension vote |

5/11/2023 |

1PM EST |

|

22 |

EGGF Deadline extension vote |

5/12/2023 |

10AM EST |

|

23 |

MCAG Deadline extension vote |

5/12/2023 |

1PM EST |

|

24 |

SLAC Deadline extension vote |

5/12/2023 |

2PM EST |

|

25 |

AXAC Deadline extension vote |

5/15/2023 |

10AM EST |

|

26 |

CREC Deadline extension vote |

5/16/2023 |

10AM EST |

|

27 |

FWAC Deadline extension vote |

5/17/2023 |

10AM EST |

|

28 |

ROCL Deadline extension vote |

5/17/2023 |

11AM EST |

|

29 |

ROCG & Tigo Energy Merger Vote |

5/18/2023 |

10AM EST |

|

30 |

PWUP Deadline extension vote |

5/18/2023 |

11:30AM EST |

|

31 |

PACI Deadline extension vote |

5/19/2023 |

10AM EST |

|

32 |

BLEU Deadline extension vote |

5/19/2023 |

10AM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

Chart 11: SPAC Events – May 2023 (2/2)

|

S. No |

Event Name |

Date |

Time |

|

33 |

GFOR Deadline extension vote |

5/22/2023 |

11AM EST |

|

34 |

CMCA Deadline extension vote |

5/23/2022 |

10AM EST |

|

35 |

MEOA & Digerati Technologies Merger Vote |

5/24/2023 |

10AM EST |

|

36 |

VMCA Deadline extension vote |

5/25/2023 |

8AM EST |

|

37 |

BRD Deadline extension vote |

5/25/2023 |

9AM EST |

|

38 |

GSRM Deadline extension vote |

5/25/2023 |

10AM EST |

|

39 |

FGMC & iCoreConnect Merger Vote |

5/26/2023 |

10AM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

|

Chart 12: SPAC Activity by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 13: Current Status of the SPAC Universe |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 14: Current Status of SPAC Universe by Trust Size |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 15: SPAC Transactions by Year |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 16: Average SPAC IPO Size ($ Mn) |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 17: SPAC Transactions by Month (LTM) |

|

|

Source: Intro-act, Boardroom Alpha

|

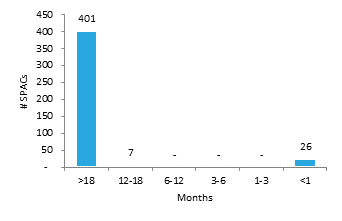

Chart 18: Time to Liquidation – By Volume |

|

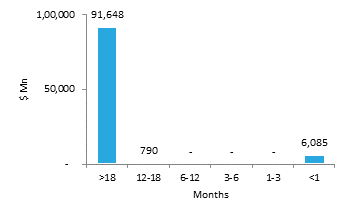

Chart 19: Time to Liquidation – By Trust Value |

|

|

|

|

Source: Intro-act, Boardroom Alpha

|

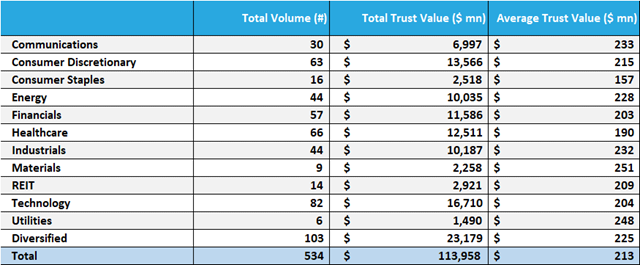

Chart 20: Active SPACs By Sector (As of Month Ending April 2023) |

|

|

Source: Intro-act, Boardroom Alpha

|

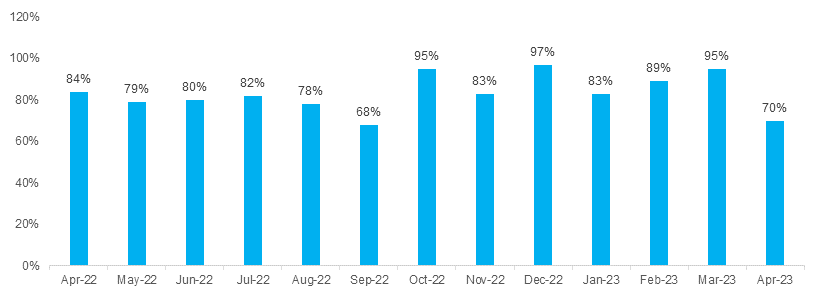

Chart 21: Average Redemption Rate by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 22: SPAC Redemption Detail – April 2023 |

||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 23: Monthly SPAC Activity – April 2023 |

|

|

Source: Intro-act, Boardroom Alpha. Searching figures ($Mn and Count) are as of month end.

|

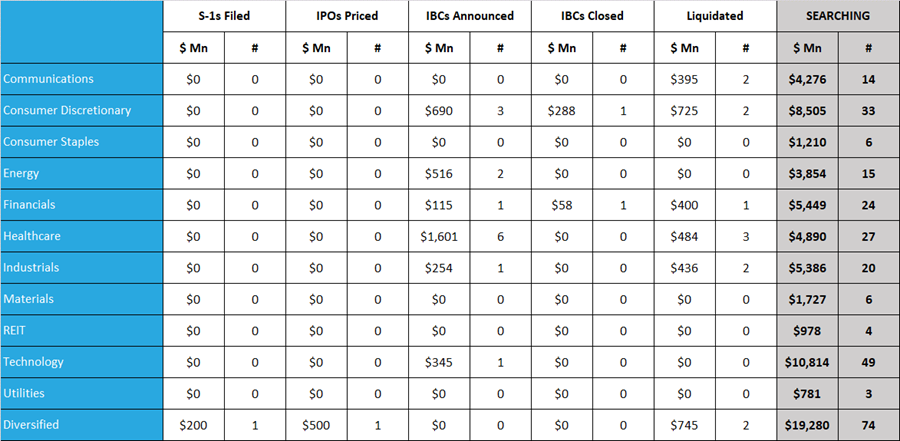

Chart 24: SPAC IBC Announcements by Target Sector – April 2023 (1/2) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

Chart 24: SPAC IBC Announcements by Target Sector – April 2023 (2/2) |

||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

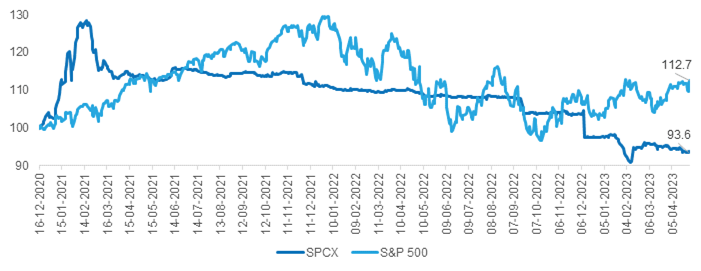

The SPAC and New Issue ETF (SPCX). SPCX gives investors exposure to a broad portfolio of SPACs with the familiar attributes of an exchange traded fund’s diversity, tax efficiency and liquidity. SPCX is the first actively managed SPAC ETF. Why active? As the SPAC market is rapidly evolving, we believe that the portfolio management approach should equally reflect the dynamic nature of this burgeoning capital-raising alternative. This is no place for a rigid rules-based index strategy.

|

Chart 25: SPCX Summary Data |

|

Chart 26: SPCX Top 10 Holdings |

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

Source: Intro-act, ETF.com. Data as of 4/30/23.

|

Chart 27: SPCX Performance |

|

|

Source: Intro-act, Yahoo! Finance. Data as of 4/30/23.

|

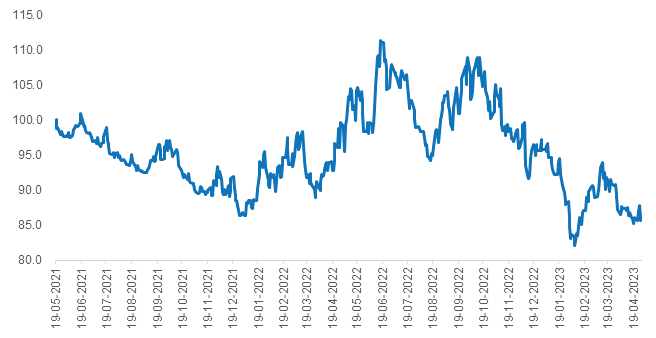

Chart 28: Relative-SPAC Index vs Russell 3000 |

|

|

Source: Intro-act, FactSet

|

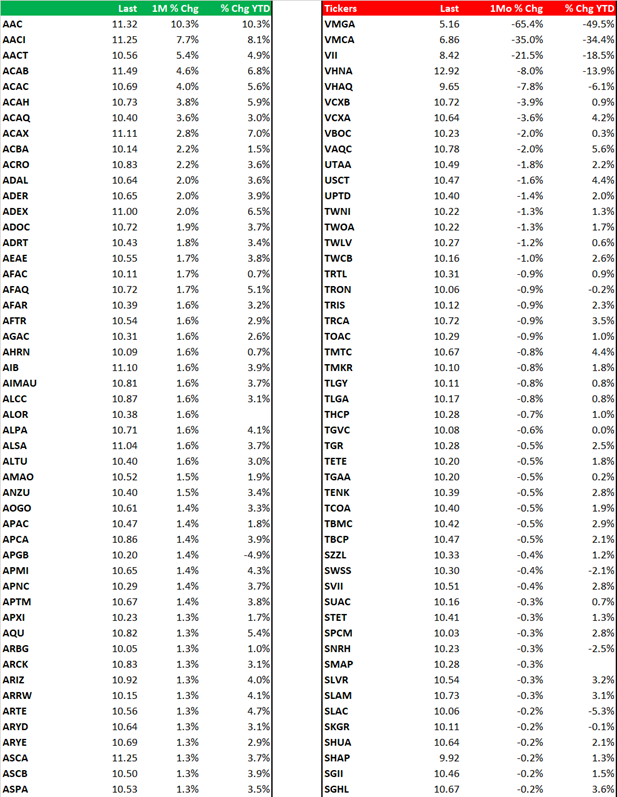

Chart 29: Gainers and Losers in the Broader SPAC Universe (% Change) |

|

|

Source: Intro-act, FactSet

|

Chart 30: SPAC IPO Pricings by Sector – April 2023 |

||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 31: SPAC S-1 Filings by Sector – April 2023 |

||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 32: SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 33: DE-SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 34: SPAC Underwriter League (YTD As of April 2023 End) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Bookrunner Volume ($ Mn) is based on the total amount of the offering sold, including over-allotment. Full credit is awarded to the sole book-runner or split equally among joint book-runners.

|

Chart 35: Top De-SPAC Advisors (YTD As of April 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Advisor credit is shared equally among all advisors on a given deal, as a proportion of the enterprise value of the target company acquired by the SPAC. Firms with multiple advisory roles receive credit for each role.

|

Chart 36: SPAC Legal League (YTD As of April 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Volume ($ Mn) is awarded to both Issuer and Underwriter Counsel.

|

Chart 37: SPAC Auditor League (YTD As of April 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research

|

Chart 38: ICR – The Leading SPAC Communications and Capital Markets Advisor |

|

113 Transactions / $267 Billion in Transaction Value Since 2021

|

Source: Intro-act, ICR. Announced SPAC transactions since 2021, All Announcements not shown. Data as of April 2022.

Analyst Certification

I, Peter Wright, certify that the views expressed in the research report accurately reflect my personal views about the subject securities or issues. I also do not receive direct or indirect compensation based on my recommendations or views.

Intro-act, Inc. (Intro-act) issued this report and may seek fees for the assistance with investor targeting, access, and further investor preparation services. Intro-act, Inc. will not seek renumeration for any investment banking service or investment advice.

Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources who are believed to be reliable. However, the issuer and related parties, as well as Intro-act, do not guarantee the accuracy or completeness of this report, and have not sought for this information to be independently verified. Opinions contained in this report represent those of the Intro-act analysts at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, and estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties, and other factors that may cause the actual results, performance, or achievements of their subject matter to be materially different from current expectations.

Exclusion of Liability: To the fullest extent allowed by law, Intro-act, Inc. shall not be liable for any direct, indirect, or consequential losses, loss of profits, damages, or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this note.

No personalized advice: The information that we provide should not be construed in any manner whatsoever as personalized advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Intro-act’s solicitation to affect, or attempt to affect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors.

Investment in securities mentioned: Intro-act has a restrictive policy relating to personal dealing and conflicts of interest. Intro-act, Inc. does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees, and contractors of Intro-act may have a position in any or related securities mentioned in this report, subject to Intro-act’s policies on personal dealing and conflicts of interest.

Copyright: Copyright 2023 Intro-act, Inc. (Intro-act).

Intro-act is not registered as an investment adviser with the Securities and Exchange Commission. Intro-act relies upon the “publishers’ exclusion” from the definition of investment adviser under Section 202(a) (11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Intro-act does not offer or provide personal advice, and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell, or hold that or any security, or that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.