Q&A OF THE MONTH – SUDHIR PANIKASSERY, FOUNDER AND CHIEF EXECUTIVE OFFICER, AERIES TECHNOLOGY

We see public listing as the next logical step in our growth as an organization: CEO of Aeries

In an email conversation with AlphaStreet, Aeries Technology’s founder and chief executive officer Sudhir Panikassery spoke about the company and its operations.

Aeries Technology is a global services company providing technology, business process management and transformation services to some of the leading global organizations. The company, which was founded in 2012, currently has over 1,600 professionals on staff.

Earlier this year, Aark Singapore Pte Ltd. and its subsidiary Aeries Technology entered into a definitive agreement with Worldwide Webb Acquisition Corp. (NASDAQ: WWAC), under which Aeries Technology would become a publicly listed company. In an interview with AlphaStreet, Sudhir Panikassery, the company’s founder and chief executive officer, gave insights into the various aspects of the business.

Q: Can you provide an overview of Aeries Technology and its operations?

A: Aeries Technology is a global professional services and consulting partner for organizations in transformation mode and their stakeholders – including Private Equity sponsors and their portfolio companies. With a deep pool of over 1,600 global professionals specializing in technology services, business process management (BPM), and AI-driven digital transformation, we utilize engagement models designed to provide the right mix of deep vertical specialty, functional expertise, and the right systems, software, and solutions needed to scale, optimize and transform our client’s business operations.

The Aeries Way is purpose-built and future-ready, and the professionals we hire for our clients are deeply integrated and treated as if they are part of the client team. These teams are built to be agile and help transform the cost structure of portfolio companies – leading to a 65% annualized customer savings, on average. Founded in 2012, we’ve been cash flow positive since 2013 and our business model has led to a customer lifetime value (LTV) of $2.3M in 2022, up from $1.7M in 2021.

Q: How significant is the public listing, and where do you see Aeries Technology five years from now?

A: At the current state of our business evolution, the benefits of accessing the public markets are significant. Going public, and partnering with Daniel Webb and his team at Worldwide Webb Acquisition Corp., will enable Aeries to accelerate our innovation capabilities for our clients and capitalize on the momentum we’ve built. Unlike many of the companies that have experienced difficulty taking the SPAC route for a listing, Aeries has the established revenue, momentum, profitability, and growth needed to succeed as a public company. We believe our ability to be disruptive in our space will lead to 54% revenue growth and a 21% EBITDA margin for CY23E.

In the next five years, I hope to see Aeries continue to disrupt our industry and continue our momentum within the public markets. We see a public listing as the next logical step in our growth as an organization and that it will help us to achieve our goal of becoming a significant player in the outsourcing industry over the next five to ten years disrupting the established paths to outsourcing. The additional capital, resources, and opportunities made possible by the public markets should help to fuel our organic growth and expansion, as well as enable acquisitions and business collaborations in an accelerated manner.

Q: Can you talk about your expansion plans; are there any M&A deals in the cards currently?

A: While I can’t share any specifics with respect to our strategic plans – M&A or otherwise – I can say that Aeries will consider and vet all avenues toward expansion and growth in the coming years. Towards this end we are actively evaluating acquisition opportunities that fit into our growth strategy augmenting our service offerings, technological capabilities, customer base, and leadership and talent pools. We anticipate that every step we plan and execute will drive value and returns for our shareholders.

Q: What are the emerging trends in the business services market, and what are your expectations for the company?

A: Along with digital transformation, the trends we’re seeing within the industry are the rise and importance of automation, the hybrid work environment, importance of cybersecurity, need for cost-effective tech skills from top to bottom within an organization, acceleration in the adoption of AI (including generative AI) based tools and solutions and the continued emphasis on profit margins and revenue growth.

Aeries anticipated these trends within the market and we have been preparing our local and global teams, as well as our customers, for each of the eventualities. This is evident by the recent launch of our cyber security managed services offering in April. Given the preparation we’ve undertaken and the team we’ve put in place, I expect Aeries to continue to be a disruptive force within the industry and lead the evolution of the business services market. Our engagement model puts us in a unique position to capture and ride the emerging trends in the industry.

Q: How do you look at the ongoing economic uncertainty, in terms of its potential effect on the business?

A: We are aware that we will be going public at an uncertain and volatile time for the market overall due to geopolitical events and post-pandemic supply chain disruption. We, of course, keep a close watch over the market conditions and these market conditions were considered when we made the decision to enter into the merger with Worldwide Webb. We feel that, for a sound fundamental business like ours, there are additional opportunities to help organizations become future-ready by entering the market at this time.

Even during these times, we were able to drive $50MM in revenue for CY22 and are projecting a 60% revenue CAGR for CY22E – CY24E. While there could be delayed decision-making within organizations, the need for sustained cost savings and operational efficiencies with a collaborative partnership will drive businesses to consider our capabilities and engagement model to help drive their organizations’ growth in a sustained manner. We also provide the talent and expertise to assist with a general technological upgrade of an organization to help gear itself up for effectively meeting the challenges of short business cycles and competition within their industry.

Link to the original interview published in AlphaStreet on June 30, 2023: https://news.alphastreet.com/we-see-public-listing-as-the-next-logical-step-in-our-growth-as-an-organization-ceo-of-aeries/

Q&A OF THE MONTH – JAKE DINGLE, CHIEF EXECUTIVE OFFICER, CARBON REVOLUTION

About Carbon Revolution: Carbon Revolution is a global technology company and Tier 1 OEM supplier, which has successfully innovated, commercialized and industrialized the supply of lightweight carbon fibre wheels to the global automotive industry. The Company was founded in 2007 with the purpose of bringing disruptive efficiency technology to all vehicles. Carbon Revolution has progressed from single prototypes to designing and manufacturing wheels at commercial scale for some of the most prestigious brands in the world. With over 60,000 Carbon Revolution wheels on the road, Carbon Revolution is the recognized leader in the sector. Carbon Revolution has penetrated the performance and premium end of the market with OEM programs for Ford, Ferrari, General Motors and Renault. Carbon Revolution was recently awarded its first EV wheel program with a North American OEM, and has more EV programs in development.

Jake Dingle is the CEO of carbon fiber wheel maker Carbon Revolution, which has announced plans to list on Nasdaq through a merger with Twin Ridge Acquisition Corp. (NYSE: TRCA). The Company is a Tier 1 OEM supplier and a leading global manufacturer of lightweight advanced technology carbon fiber wheels. In June the company announced that its backlog has more than doubled to $680 million since October 2022 due primarily to new programs. Nearly 50% of the backlog is for electric vehicle (EV) programs.

Recent awards of new programs take Carbon Revolution’s total lifetime awarded programs with global automakers Ford Motor Company, Ferrari NV, General Motors Company, Renault Group (“Renault”) and Jaguar Land Rover Automotive Plc to 16 with another 3 programs in progress under engineering agreements. These are awards over the Company’s lifetime, of which 6 are in production, 5 are in development and 5 are in aftersales.

The Company has said that total revenue is forecast to grow from $28.5 million in calendar year 2022 to $90.1 million in 2024 for a compound annual growth rate (CAGR) of 78%..

[Backlog as of 5/29/2023, Backlog (remaining lifetime gross program projected revenue) is based on awarded programs and excludes programs that are contracted for engineering. See Projection Methodologies here for important details.]

The following has been adapted from a SPAC Insider podcast. The complete podcast is accessible here.

Question: Car enthusiasts have been bolting carbon fiber wheels onto high performance vehicles for years, but hitherto luxury add-on brings real benefits to vehicle weight and energy economy, both of which have a new importance in the age of EVs. Carbon Revolution is working to scale up its carbon fiber wheel production to provide the wheels as a mass produced staple in the industry. They announced a 270 million dollar combination with Twin Ridge Capital in November to accelerate these plans.

Some may not consider the wheels to be the part of the vehicle that is going through a lot of technological advancement right now, but Carbon Revolution has racked up 58 patents so far with 31 more pending, all focused on the wheels. So what are some of the innovations that you've been able to generate there?

Jake Dingle: Well, firstly, wheels have not really progressed very much since the introduction of aluminum wheels back in the '70s. This really is a big step forward. Our wheels are made from carbon fiber, which is a very sophisticated, complex material to work with, but it's extremely light and extremely strong, and it enables us to take up to 50% of the weight out of a wheel versus a conventional aluminum wheel. Even more if you compare it with a steel wheel. But it's a really challenging material to work with, so in order to do what we've done, you need to have advanced engineering capabilities and advanced manufacturing capabilities to do that. But yes, it really is the next step change in wheel technology, having really seen no major step forward since the advent of aluminum wheels some 40 to 50 years ago.

Question: And it seems like carbon fiber wheels, they've been around for a little bit, but they've long been considered a nice aftermarket add on for car enthusiasts, but it wasn't something that was coming stock on vehicles off the line very often. But that seems like that's changing now. What are you seeing there?

Jake Dingle: Well, we set this business up to be a disruptor. Our focus right from the outset was on the OEMs, so the car manufacturers rather than aftermarket. Even though, like a lot of new technologies that are introduced and taken up and ultimately become mainstream, this has started at the premium performance luxury end of the market, and that's still an enormous part of the market. Automotive wheel market is around about $38 billion a year, so it's an enormous market. We've come in at the top end, but we'll trickle down as aluminum wheels did.

By setting the business up to be a disruptor and to be a high volume supplier to the automotive OEMs, we've enabled ourselves to set up to scale and to take cost out and to facilitate that expansion and growth. That's really the difference in terms of how we've approached this versus anybody else that's tried to do carbon fiber wheels, and that's why we are really the only company in the world that has these multiple programs and a scale manufacturing facility to be able to do the sort of volumes that we're already doing and then into the future to be able to be a real disruptor.

Question: Many of your competitors are still aftermarket focused. With that in mind, can you dive a bit deeper into what your strategy has been for getting integrated with the major OEMs?

Jake Dingle: Yeah, sure. They're very, very different markets. If you are to be an OEM supplier, you're dealing with very large sophisticated engineering organizations that have an extremely high risk aversion or sense of risk around any safety critical technology like this. The validation requirements for the product itself, to ensure that it's safe to be integrated onto a vehicle, and then the expectations and demands around quality, so the ability to keep producing at a level of quality that meets their expectations, and then to be able to grow volume to something very much larger than anything you ever see in the aftermarket, that creates an enormous barrier to entry.

The customer relationships and the ability to take a customer in this market, these very large, sophisticated global car makers, introduce a brand new technology in a safety critical part of the vehicle, get them comfortable enough to introduce it on a relatively small niche vehicle, as we've done in the initial stages of adoption, where it is high profile, but not particularly high volume. And then to be able to work through to offer it in higher volumes to larger vehicle platforms.

That creates a relationship, it creates a level of trust and understanding of the safety capability and the quality capability of the technology in the company. And that represents a very high entry barrier. Aftermarket does not have those sorts of entry barriers. It's far easier to introduce products into the aftermarket, and the market is much smaller and more fragmented. That's why going back over a decade, we set out to be an OEM supplier. The way we've structured the business, the way we've targeted our technology, our technology strategy and the evolution of both the product and the processes that make the product, they've all been directed towards high volumes, high levels of quality, meeting the OEM’s requirements in those regards and ensuring that we have strong customer relationships.

And that's really a huge blocker, it's a very, very strong entry barrier, because whilst our customers love the idea of this technology and wanted to see it introduced and continue to want to see it proliferate, particularly as they shift to EVs, they are very, very risk averse, so they invested heavily to make sure that the supply of it was going to meet all of those requirements, and they partnered with us very strongly. It's unlikely that they would invest that much again to bring somebody up to this stage. They would expect anybody else coming to them with an alternative version of this to be effectively comparable, and that makes it very difficult for anyone to follow.

Question: Lighter is better with EVs but we also know that those cars and those builds are getting heavier and heavier. Can you walk through just how that translates into value, both in terms of the EV's performance and then also in terms of value for the OEM and onto the end customer?

Jake Dingle: Yeah, sure. There are a number of different ways that this adds significant value. The first, most obvious is in range. As a significant weight saving technology, it directly contributes to range, and that can be anywhere between 5% and 10% extension. 5% if you're just purely adding the wheels and being able to replace that weight save with additional battery. You can see it more than 5% directly in terms of additional range. But if it's fully integrated into the vehicle and you take advantage of other elements, like the ability to create more efficient aerodynamic shapes, the NVH or the noise transmission benefit, given that this is quite a damped material means that additional weight can be taken out.

Other knock-on benefits means that up to 10% is actually possible. And from a range point of view, that's a really, really big number. Anywhere between five and 10% with bolt-on technology that doesn't require investment in the plant that's manufacturing in the way that anything on the body of the vehicle would or in the chassis would. That's really meaningful. And there is obviously a significant competitive environment around range, trying to deal with consumers' range anxiety, given that these vehicles go a lot less far on a charge than they used to on a tank of fuel.

There's a couple of other important aspects though. One is around regulatory drivers. The car makers are still dealing with CAFE credits and the ability to meet the requirements of the regulator in terms of corporate average fuel economy. The ability to offer significant weight savings means that we can very meaningfully help them to keep these larger vehicles, particularly within weight class limits.

That means that they count towards their CAFE credits, and that's worth an enormous amount. It means that the EV continues to contribute to the corporate average fuel economy, and it means that they can continue to sell the ICE or internal combustion engine vehicles alongside the EVs and continue with that business model. The point at which they're too heavy to do that means that there are penalties and things that could otherwise be avoided if you can take weight out. Being able to offer this much weight, up to 150 pounds of weight saving is a very meaningful way to hit those targets.

And the final one is just around structure. You've probably noticed in the last 30 years, wheels have continued to get bigger and bigger. That's really been driven by the studios and the designers and requirements of the aesthetics of vehicles. And that won't change. The designers within the car makers tend to have a very significant impact on what the engineers then have to go and engineer into vehicles. And so as wheels get up to 23 and 24 inches, and the one that we've just launched with JLR is a 23-inch wheel, in aluminum, they're incredibly heavy.

And as you add more weight for the strength required to take the even heavier EV versions of these vehicles, you're starting to see structural problems. Having that much weight on the corners of the vehicle or the ends of the axles creates really significant structural issues. And so rather than having to redesign, retool the connecting structures, the suspension, those sorts of things, which is high investment cost, you can replace those very heavy aluminum wheels with much lighter carbon fiber wheels that are half the weight. They're the weight of a much, much smaller aluminum wheel, and you avoid a lot of other engineering challenges that may add weight.

And so those three areas. Really, range is the obvious one. Regulatory drivers are of significant importance, particularly at the moment through this transition period. And then just structural performance, which is avoiding that knock-on additional weight issue by having to engineer stronger and heavier structures. We're helping in all of those ways. And in the future, aerodynamics for more range, NVH for less sound deadening material, they're the sort of next level or the next tier of benefit that we're starting to get to. Because frankly, what we are designing and what you've seen on the road are not really... They're not aerodynamically or geometrically really optimized for the material. They're really rendering much more traditional wheel designs in carbon fiber. There's still a long way to go in terms of getting the full benefit of this technology.

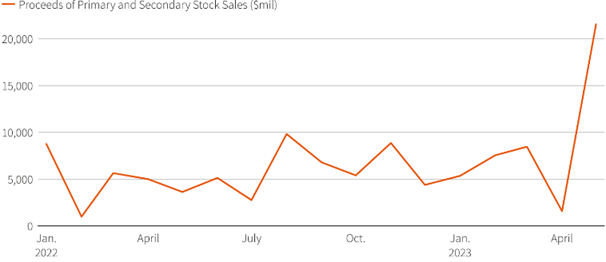

Stock sale frenzy foretells U.S. IPO market comeback. A flurry of stock sales by companies points to a likely wave of initial public offerings launching come September, potentially marking the end of a weak market for debuts that has persisted for a year and a half. Publicly listed companies and their backers, such as private equity firms, have sold stock worth more than $28 billion in the U.S. since the end of April through follow-on and secondary sales, according to data provider LSEG Deals Intelligence. That compares with $7.3 billion over the corresponding period a year ago. This spike bodes well for the IPO market, bankers say, because both new listings and secondary stock sales rely on strong demand from equity investors. The IPO market has been in the doldrums since the start of 2022, when Russia's invasion of Ukraine and a spike in inflation fueled a bout of market volatility as investors fretted over U.S. interest rate hikes. IPOs excluding special purpose acquisition vehicles raised $154 billion globally in 2022, a 65% decrease from a record breaking 2021, according to data provider Dealogic. Read More (Reuters)

|

Chart 1: U.S. – Listed Stock Sales |

|

|

Source: Intro-act, Reuters

Public M&A: Global overview. Following the record year of 2021, global M&A activity in 2022 fell back down to Earth. Transactions amounting to $3.6 trillion were announced in 2022, a 37% decline from the $5.9 trillion of transactions announced in 2021. Nearly 55,000 deals were announced in 2022, down 17% from the over 63,000 announced in 2021. The story, however, is not complete without noting the large shift in activity levels from the first half of 2022 as compared to the second half of the year. In the first two quarters of 2022, global M&A activity reached over $1 trillion of transactions announced in each quarter – marking a new record of eight consecutive quarters with over $1 trillion of transactions announced. This consecutive winning streak then came to an abrupt end, as the second half of 2022 saw global M&A activity fall precipitously. Read More (Lexology)

Liquidation season: SPACs have sent back nearly $30 billion to investors. The SPAC sector has been a major source of corporate finance in the U.S. So far in 2023, nearly $30 billion from Special Acquisition Companies have already been given back to investors. Wall Street firms including KKR and TPG have all liquidated their SPACs and returned money to investors, as the number of available companies to buy continues to plummet. CultureBanx reports that a SPACs main goal is to raise capital and its major downfall is that there are too many blank check companies willing to do this work. According to the De-SPAC index, out of all the companies that have completed their deals, the returns are down by 67% with another 22% below the 2% mark. Companies that went public this way have lost more than $100 billion in market value. Read More (Forbes)

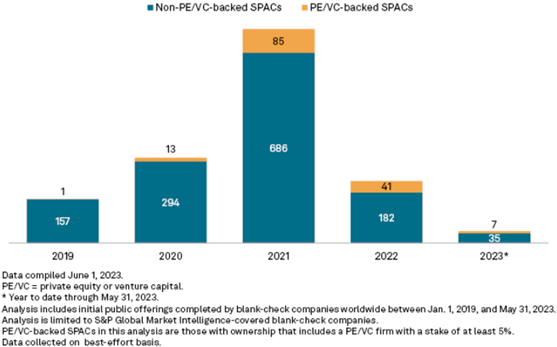

Private equity's role in SPACs grows as market shrinks. Private equity took on a larger role in the market for special purpose acquisition companies even as the number of so-called blank-check companies contracted sharply in the wake of the 2021 SPAC boom. More than 18% of SPACs that held an initial public offering in 2022 were backed by private equity, up 7 percentage points from 2021 and 14 percentage points from 2020, according to an S&P Global Market Intelligence analysis that tracked SPACs with at least 5% ownership by a private equity or venture capital firm. In the first five months of 2023, as some SPAC activity shifted to Asia from North America, nearly 17% of all SPAC IPOs globally were private equity-backed SPACs. Read More (S&P Global)

|

Chart 2: PE/VC-backed SPAC IPO activity worldwide, 2019-2023 |

|

|

Source: Intro-act, S&P Global Market Intelligence

SPAC-squared is Wall Street’s latest wheeze. Just when you think you’ve seen it all in SPAC-land, along comes a money-losing company that only recently went public via a blank-cheque firm announcing a merger with a second special purpose acquisition company (SPAC) to save its skin. SPAC-squared, if you like. Wejo Group, a British connected-vehicle data company, became a public company in November 2021 after combining with Virtuoso Acquisition, a SPAC. Wejo said it plans to merge with another blank-cheque firm, TKB Critical Technologies I, to secure up to $100 million in cash. While this isn’t the first time a SPAC has announced a deal with an already-public company, such transactions are unusual. Typically, these listed cash-shells are used to bring private companies onto the stock exchange, circumventing the regular initial public offering process. Read More (The Business Times)

The great SPAC robbery. SPACs, or special-purpose acquisition companies, are shell firms that go public for the sole purpose of merging with a hot startup, which then replaces the SPAC in the stock market. SPAC creators are given a unique incentive: They are allowed to buy 20% of the company at a deep discount. A review of SEC filings found 232 SPACs with insider sales, and "on average, insiders sold about $22 million of shares each" – for a total of $22 billion in sales. Some of the biggest winners, like Virgin Galactic founder Richard Branson and convicted Nikola founder Trevor Milton, made hundreds of millions of dollars before shares in their companies plummeted. Branson sold 75% of his holdings for more than $1.4 billion; Virgin Galactic shares are down more than 90% from their high. Read More (The Week)

Why dealmaker Betsy Cohen believes SPACs will make a comeback. During the Covid-19 years, investors flocked to SPACs. These reverse merger vehicles – better known as SPACs – have fallen out of flavor amid rising interest rates and slumping stock valuations. But one prominent dealmaker, Betsy Cohen, says they’re due for a comeback, Forbes reports. “It will come back, because it serves a need,” says Cohen, who helped take seven companies public through SPACs between 2015 and 2021, making her one of the industry’s more prolific sponsors. These deals helped Cohen, age 81, build her estimated $245 million fortune, which puts her at No. 98 on Forbes’ just-published annual list of America’s Richest Self-Made Women. Read More (Forbes)

SPACs in limbo: Looming deal deadlines and avoiding liquidation. A special purpose acquisition company (SPAC) is a blank check company that is formed and listed in the public markets specifically to acquire other companies. Overall, I and others, even with stricter laws since their formation in the '80s, have found the laws surrounding the use, ownership and management of SPACs to be inadequate with a great possibility for misuse. What is currently more pressing concerning SPACS, though, is the many shell corporations that face liquidation as deal deadlines loom. The year 2021 saw the highest number of SPACS formed. This is the post-Covid period when businesses were recovering from the effects of the pandemic. Over 700 SPACs were created in 2021, but only 467 acquisitions were completed during the year. This meant that there were hundreds of other blank check companies that were formed and listed in 2021 that did not have any transactions. In addition to that, other SPACs were formed in 2022, but they have not had any action. Read More (Forbes)

Are D&O insurance rates ‘Bottoming Out’ this year? Directors and officers insurance rates will start to “bottom out” for legacy firms and public companies that did not go public in the last three years, according to one D&O insurance analyst. Mike Tomasulo, senior managing partner and national management liability practice leader at BRP Group, said that older firms aren’t likely to get similar rate reductions again this year. But firms that were in recent initial public offerings might still have room for their rates to lower, reports Insurance Business. “We’re seeing (the rate decreases) start to level off,” Tomasulo said. “I do not think we’ve seen the bottom, or do I think we’re going see the bottom in 2023 for companies that have gone public in the last year or two, because their ceiling is so much higher than a lot of their counterparts that have been public (for some time).” Read More (Insurance Business)

Fairness opinions and SPAC reform. A Washington University professor examines the emerging regulatory framework for SPACs, noting that de-SPACs, must be “fair” to public (or unaffiliated) SPAC shareholders, and transaction participants face heightened liability risk for disclosure errors. This framework is a product of the SEC’s reform proposal for SPACs and recent decisions of the Delaware Court of Chancery, writes law professor Andrew Tuch. In this environment, third-party fairness opinions have been regarded as a de facto requirement for de-SPACs. Tuch analyzes the significance of third-party fairness opinions and the proposed disclosure-oriented reforms. Read More (Harvard Law School Forum)

SEC spring rulemaking agenda published. The Office of Information and Regulatory Affairs published the Spring 2023 Unified Agenda of Regulatory and Deregulatory Actions. This includes the SEC’s spring rulemaking agenda, notes Mayer Brown. The commission proposed rules and rule amendments intended to enhance investor protections in IPOs by SPACs and in subsequent business combination transactions between SPACs and private operating companies. Specifically, the Commission proposed specialized disclosure requirements with respect to, among other things, compensation paid to sponsors, conflicts of interest, dilution, and the fairness of these business combination transactions. Read More (Mayer Brown)

SEC continues SPAC crackdown as founder trading profits generate scrutiny. Despite the frothy market for special purpose acquisition companies (SPACs) in 2021, companies considering such a transaction have been met recently with significant market headwinds, a short supply of suitable targets, the onset of a highly anticipated SEC rule and, in recent weeks, new SEC enforcement actions targeting alleged investment adviser disclosure failures involving alleged conflicts of interest. When considering these cases along with a recent article highlighting the billions of dollars that SPAC founders and insiders reaped from de-SPAC transactions before share prices of the new public companies collapsed, rough waters may still lie ahead for SPAC participants. Holland & Knight provides an overview of one of the SEC’s enforcement actions and additional color on the magnitude of SPAC founder share trading, while offering some key takeaways. Read More (JD Supra)

SEC continues to focus on SPAC market. In recent years, the U.S. SEC has had its eye on the SPAC market – warning investors against putting money into SPACs, expressing skepticism about their performance, and taking affirmative steps to corral SPACs, including direct prosecution of investment firms. Now its gaze has turned upon a market gatekeeper. On June 21, the SEC brought an enforcement action against Marcum LLP, one of the largest public accounting companies, for widespread quality control failures and violations of audit standards in connection with the firm’s audit work over the past few years, including audits for hundreds of SPAC clients. Without admitting or denying the SEC’s findings, Marcum has agreed to pay a $10 million penalty, as well as pay for an independent consultant to review and evaluate its quality control policies and procedures for (potentially) the next two years, among other remedial actions. Read More (JD Supra)

SEC settles charges with accounting firm for quality control deficiencies. The SEC recently settled charges against an accounting firm for alleged systemic quality control failures and violations of audit standards, primarily in connection with audit work performed for hundreds of special purpose acquisition companies (SPACs). The SEC Order details the rapid growth of the accounting firm over a three-year period in which it more than tripled its number of public company clients, the majority of which were SPACs. According to the SEC Order, the “exponential growth” of the accounting firm’s public company practice, primarily for SPACs, revealed “substantial, widespread, and pre-existing deficiencies” in quality control processes, which the firm failed to remediate. Read More (JD Supra)

Circle’s public listing plans undeterred by latest SEC actions. The latest SEC action against publicly traded company Coinbase has not deterred crypto payments tech company Circle – or others – from continuing its quest to go public. Still, the path for most companies mulling a public listing is likely to be tough in the current environment, an industry executive said. After revealing a plan to become a public company by merging with a special purpose acquisition company (SPAC) in 2021, Circle CEO Jeremy Allaire said in a December 2022 tweet that his company “did not complete SEC qualification in time.” Executives said earlier this year going public remained a key part of Circle’s strategy – a plan confirmed again this week by a company spokesperson and a recent job posting. Read More (Blockworks)

Sen. Kennedy (R-LA) introduces SPAC Act to increase transparency of blank-check firms. Sen. John Kennedy (R-La.) introduced the Sponsor Promote and Compensation (SPAC) Act, which he said would provide greater transparency for investors involved with SPACs. Within 120 days of its enactment, the SPAC Act would require the SEC to issue rules on enhanced disclosures for SPACs during the initial public offering stage and the pre-merger stage to make those disclosures more transparent to investors, especially main street investors. These measures would help investors make more informed decisions about a company’s shares. Read More (Kennedy Senate)

Fizzling SPAC wave leads to rash of lawsuits. First came the SPACs. Now come the legal actions. Special purpose acquisition companies (SPACs) were a super-popular method of going public in recent years. But as Bloomberg News reported Thursday (June 1), those listings have now triggered a wave of litigation from investors who say they got a raw deal. According to the report, these suits allege SPAC executives made millions on deals that let them cash in founder shares, which were marked-down equity stakes that would pay off if they could find a company to purchase. A report by The Wall Street Journal found that some of 2022’s largest goodwill impairments were from companies that went public via SPACs, with many of them having pretax impairments last year greater than $1 billion. Read More (PYMNTS)

Class action lawsuits filed against Trident Acquisitions founders, financial advisor. The architects of an ill-fated 2021 merger between Lottery.com owner AutoLotto and Trident Acquisitions are facing class action lawsuits in the Chancery Court of Delaware. The deal made Lottery.com a publicly-traded entity, but share values for the lottery courier service began to plummet almost immediately. Revelations of financial deception, executive resignations, and shareholder lawsuits followed, reports Bonus.com. The plaintiffs in the three cases are Tim Weishipl, Jared Polisher and Edward Knolls. Weishipl filed a class action complaint “on behalf of himself and similarly situated current and former stockholders” in April 2023. Polisher and Knolls followed suit in May. If the cases advance, they would likely be consolidated. Read More (Bonus.com)

SPAC-mongers face mounting lawsuits. SPACs may have gone splat, but the SPAC kings made a killing. Now comes the legal SPAC attack. According to a new Bloomberg report, a wave of lawsuits backed by scorned investors are hitting SPAC-happy executives like Chamath Palihapitiya and Alec Gores, who, more often than not, made out with small fortunes even as newly public companies crashed and burned. Read More (The Motley Fool)

Billionaire SPAC kings get taken to court. The unwinding of the blank-check stock frenzy, one of the hottest pandemic-era trends on Wall Street, is now playing out on a different stage: the courtroom. The raucous boom in SPACs has also spawned a wave of litigation, with dozens of cases filed by burned investors working their way through court. In the last few months alone, they’ve taken aim at some of the most well-known operators: Chamath Palihapitiya,the former Facebook executive who became the public face of the SPAC mania; billionaire Alec Gores; Bill Foley, owner of the NHL’s Las Vegas Golden Knights hockey team; and British entrepreneur Richard Branson. Read More (Bloomberg Law)

U.S. electric vehicle start-up Lordstown Motors files for bankruptcy protection. Lordstown Motors has filed for bankruptcy protection, marking the end of the road for an ailing electric truck manufacturer that promised a corner of the U.S. Rust Belt hundreds of jobs tied to the auto industry’s green transition. The company said the move followed the unravelling of a deal with Taiwan’s Foxconn, which in 2021 agreed to partner with Lordstown and help produce its flagship pick-up truck, the Endurance, and last year purchased its plant. Lordstown accused Foxconn of failing to “execute on the agreed-upon strategy, leaving us with Chapter 11 as the only viable option to maximize the value of Lordstown’s assets for the benefit of our stakeholders”. Read More (Financial Times)

EV SPAC frenzy fizzles as startups fall into burning zone. The electric vehicle SPAC frenzy that swept through 2020 and 2021 has come crashing down, dashing hopes of investors. During this period, SPACs turned out to be the most popular course of action for EV startups to go public, helping them to avoid the complexity and strenuous paperwork associated with the traditional IPO. But, in 2022, EV SPAC deals slowed as investors were let down by the missed deadlines, unmet milestones and meager profits of the startups. SEC investigations into some of the deals have made it difficult for these EV startups to secure funding, resulting in SPAC financing losing its allure. Read More (Zacks)

Stellantis SPAC deal has suitably decent airbags. Carmakers are in a race to lock in battery metals like lithium. For shareholders, the risk is that they tie up capital in expensive supply deals, or mines in far-flung locations with poor governance. Stellantis’s investment in a London-based special purpose acquisition company deal looks like a neat fix to those challenges. Investing in London SPACs isn’t a surefire bet. The sector has an uneven record, tainted by dogs like Nat Rothschild’s Vallar a decade ago. ACG Acquisition, created by former EN+ Group boss Artem Volynets, at least came to market last year, after the recent SPAC boom had peaked. Read More (Reuters)

VW, Glencore back $1 billion SPAC mine deal to secure EV metals. Russian metal industry veteran Artem Volynets’ blank check firm agreed to acquire two Brazilian mines for $1 billion including debt in a bid to tap demand from electric-vehicle makers. London-listed ACG Acquisition is buying the assets from private equity firm Appian Capital Advisory. Volkswagen AG’s battery arm will support the deal with a $100 million prepayment for future nickel deliveries, while commodities trader Glencore Plc will buy $100 million of ACG stock. The transaction includes a nickel sulphide mine in Santa Rita, known as Atlantic Nickel, as well as the Mineraçao Vale Verde copper mine in Serrote. Chrysler owner Stellantis NV and La Mancha Resource Capital have agreed to buy $100 million of ACG stock apiece. Read More (Bloomberg)

Trump SPAC investors charged in $22 million scheme. Three investors in the SPAC that has agreed to take Trump Media & Technology Group public were indicted on charges they used inside information about the deal to make $22 million in illegal trades. Digital World Acquisition (DWAC) is the SPAC that has signed a deal to merge with Trump Media, which runs Donald Trump’s “Truth Social” network, and take it public. Michael Shvartsman, the CEO of Rocket One Capital. and his brother Gerald Shvartsman, were named in a federal indictment unsealed Thursday in Manhattan federal court. Bruce Garelick, chief investment officer of Rocket and a former member of the DWAC board, was also named. The defendants allegedly tipped off friends and colleagues, who also purchased securities in Digital World before the blank-check firm’s Trump Media deal became public. All three have surrendered to authorities and are expected to appear in federal court in Miami later today, a law enforcement official said. Read More (Bloomberg)

Digital World and Trump Media should call off their deal. When former President Trump in October 2021 agreed to merge his fledgling social media company with a SPAC, it made tons of sense. Fifteen months later, with the deal mired in legal and regulatory limbo, it would make sense for both sides to walk away. Truth Social is the presumptive Republican nominee’s primary medium for written communication, as he hasn’t returned to Twitter despite being reinstated by Elon Musk. There’s also been a lot of money at stake. Read More (DealFlow’s SPAC News)

Grindr CEO keeps the faith in SPACs despite his disappointments. George Arison, CEO of Grindr Inc., is a steadfast believer in special-purpose acquisition companies, despite the recent uninspiring performances of the vehicles after they go public. Shares in the dating app that specializes in connections for the LGBTQ+ community have slumped 47% since it merged with a SPAC in November. Shift Technologies Inc., the auto e-commerce marketplace Arison is chairman of after co-founding, saw an even more spectacular slump, wiping out 98% of its value from an October 2020 blank-check tie-up. Read More (Bloomberg Law)

Insurtech Hippo Holdings has ‘SPAC Remorse’. In 2021, about 200 businesses merged with special purpose acquisition companies as a way to go public. hippo Holdings, an insurtech, now wishes it hadn't taken part in the so-called SPAC euphoria, Fortune reports. Hippo was valued at $5 billion in March 2021 when it announced its combination with Reinvent Technology Partners Z, a SPAC backed by Reid Hoffman, cofounder of LinkedIn, and Mark Pincus, founder of Zynga. SPACs, at the time, were wildly popular due to the advantages promised by blank-check companies. Merging with a SPAC was believed to be a quicker, and cheaper, route to public markets compared with a traditional IPO. Companies using SPACs could also provide future guidance, which is not allowed with traditional offerings. Read More (Fortune)

Drained of cash, Buffalo Bills owner’s SPAC closes in on a deal. The cachet of Terry Pegula, owner of the National Football League’s Buffalo Bills, is such that even after his blank-check company returned the bulk of its cash to shareholders, it’s still an attractive deal partner. Abacus Life is pushing ahead with a merger with Pegula’s East Resources Acquisition despite the fact that 92% of shareholders in the SPAC have swapped their stock for their money back. While the smaller amount of shares available for trading may cause Abacus to be volatile and will bring in less cash, at a time when many de-SPACs are tanking, it’s not a big enough concern to deter the life insurance asset manager. That’s because a pact with Pegula’s SPAC would raise awareness around the company, said Abacus’s chief executive Jay Jackson. Read More (Yahoo! Finance)

$1 billion SPAC deal shows how mining supply chains are breaking up. Appian Capital Advisory bought the Santa Rita nickel mine out of bankruptcy for $68 million and the Serrote copper-gold project for $40 million in 2018. The previous owners of the Santa Rita had already spent $1 billion building the mine and Appian splashed another $400m on both properties bringing them into production. The London-HQ company sold the two Brazilian properties for $1.065 billion, $65m of which is associated with a contemplated gold royalty on Serrote. Few metals give nickel a run for its money when it comes to volatility. When Appian bought Atlantic Nickel in 2018 the price averaged just over $13,000 a tonne and on its way to today’s $25k the devil’s copper briefly topped $100k. And if someone said in 2018 that not one, but two automakers would fund the investment to buy the mines, few would have called that rational. Read More (Mining.com)

Larger SPAC listings gain momentum in Korea. The Korean SPAC market with typical offerings of around 10 billion won ($800,000) is now witnessing consecutive listings of large-scale SPACs with over 30 billion won. Pulse reports that KB Securities Co. is conducting book building for KB SPAC No. 24, which has a public offering size of around 32 billion won. KB Securities recently completed the merger of KB SPAC No. 20 and Opticore within the past six months and submitted two merger applications for other SPACs. NH Investment & Securities conducted public subscriptions for NH SPAC No. 29 with a public offering size of 25.5 billion won following a two-day book building. Read More (Pulse)

Chijet Motor Company Inc. (CJET) and Jupiter Wellness Acquisition Corp. complete business combination. Jupiter Wellness Acquisition Corp. completed its business combination with Chijet, Inc., a high-tech enterprise engaged in the development, production and sales of new energy vehicles, and their newly formed holding company, Chijet Motor Company, Inc. Chijet’s ordinary shares started trading on The Nasdaq Global Market under the new ticker symbol “CJET” on June 2, 2023. The Business Combination was approved at a special meeting of JWAC’s stockholders on May 2, 2022. Upon the closing of the Business Combination, the previously-trading Class A common stock, and rights, of JWAC ceased to trade with such rights being by their terms exchangeable for one-eighth of one share of such Class A common stock upon the closing of the Business Combination. Read More (Globe Newswire)

The Beneficient Company Group, L.P. (BENF) and Avalon Acquisition Inc. complete business combination. Avalon Acquisition Inc., a publicly traded special purpose acquisition company closed its business combination with The Beneficient Company Group, L.P., a technology-enabled platform providing liquidity, data, custody and trust services to holders of alternative assets. Pursuant to the business combination agreement, each share of Avalon Class A common stock, par value $0.0001, converts into one share of Beneficient Class A common stock, par value $0.001, and one share of Beneficient Convertible Series A preferred stock, par value $0.001, which is convertible into one-quarter (1/4) of a share of Beneficient Class A common stock. As the Beneficient Series A preferred stock is not expected to be listed on The Nasdaq Stock Market LLC, the Beneficient Series A preferred stock would automatically and immediately upon issuance convert into shares of Beneficient Class A common stock, which is expected to result in an effective exchange ratio of 1.25 shares of Beneficient Class A common stock for every one share of Avalon Class A common stock. Read More (Globe Newswire)

NET Power, LLC (NPWR) and Rice Acquisition Corp. II complete business combination. NET Power, LLC, an energy company whose proprietary technology delivers clean, affordable, reliable energy, and Rice Acquisition Corp. II (NYSE: RONI), a publicly traded special purpose acquisition company, completed its business combonation. The combined company operates as NET Power Inc. and its Class A common stock and warrants to purchase Class A common stock started trading on the New York Stock Exchange on June 9, 2023, under the ticker symbol NPWR and NPWR WS, respectively. NET Power has an initial enterprise value of approximately $1.5 billion and a market capitalization in excess of $2.0 billion. The proceeds from this transaction are expected to provide NET Power with ample capital to fully fund its corporate operations and grow its backlog of utility-scale power plant projects, with plant deliveries expected to begin in 2026. Read More (Business Wire)

Metals Acquisition Limited (MTAL) and Cobar Management Pty Ltd (CMPL) complete business combination. Metals Acquisition Limited (MAC) and Glencore have closed the purchase and sale of Glencore’s 100% interest in Cobar Management Pty Ltd (CMPL), the owner of the CSA copper mine in New South Wales, Australia. MAC’s ordinary shares and warrants will commence trading today, June 16, 2023, under the ticker symbols “MTAL” and “MTAL.W”, respectively, on the New York Stock Exchange. In connection with the closing of the business combination, Metals Acquisition Limited completed its previously-announced merger with Metals Acquisition Corp, a special purpose acquisition company. The purchase consideration to Glencore includes $775 million in cash and $100 million in ordinary shares of MAC. Glencore holds 20.6% of the ordinary shares in MAC post-closing. Read More (Business Wire)

Drilling Tools International Holdings, Inc. (DTI) and ROC Energy Acquisition Corp. complete business combination. Drilling Tools International Holdings, Inc., a leading oilfield services company that manufactures and provides a differentiated, rental-focused offering of tools for use in horizontal and directional drilling, completed its business combination with ROC Energy Acquisition Corp. The combined company operates under the name Drilling Tools International Corp. Commencing June 21, 2023, DTI's common stock started trading on the Nasdaq Capital Market under the symbol "DTI". The Company will continue to be led by Wayne Prejean, Chief Executive Officer, and David Johnson, Chief Financial Officer, alongside the rest of the current DTI management team. The transaction was approved by ROC's shareholders at a special meeting held on June 1, 2023. Read More (PR Newswire)

DiaCarta announces the termination of business combination agreement with HH&L Acquisition Co. DiaCarta, Ltd., a precision molecular diagnostics company, terminated its Business Combination Agreement with HH&L Acquisition Co. On June 26, 2023, the company received a notice from HH&L Acquisition Co. terminating the Business Combination Agreement dated October 14, 2022, by and among the Company, the SPAC, and Diamond Merger Sub Inc., as amended. The termination notice alleges wrongdoing by the Company which the Company vehemently denies. Adam (Aiguo) Zhang, DiaCarta’s Chief Executive Officer, expressed confidence in the Company’s future stating, “It is unfortunate that our arrangement with the SPAC has come to this, however, DiaCarta has a bright future, and we continue to be focused on realizing the full potential of our superior technology for the benefit of our partners and patient population.” Read More (Business Wire)

Force Pressure control terminates deal with Stratim Cloud Acquisition; SPAC to liquidate. Stratim Cloud Acquisition in an 8-K said it received a notice from Force Pressure Control that it would terminate their merger agreement. Force also agreed to pay the SPAC $250,000 for calling off the deal. The combination was announced in March at a $240 million valuation. Force is a vertically integrated provider of services to the oil & gas industry. As a result of the termination, Stratim Cloud management said in the filing they do not believe it will be possible to find and close another deal before the Sept. 16 deadline, so the SPAC intends to redeem shares and shut down. There was no mention of when the wind-up would begin or an estimated redemption price for Stratim Cloud stock. Read More (SEC)

Avila Energy Corporation announces Insight Acquisition Corp.’s decision to terminate the business combination. Avila Energy announced that Insight Acquisition has sent a notice of default, and that it intends to terminate the business combination agreement signed in April – if the alleged default is not cured by July 26. “Despite the successful negotiation and settlement executed and announced on June 26, between Avila Energy Corporation and MTT, Insight Acquisition Corp. has provided notice that it is not satisfied that Avila has cured its concerns and has chosen to put Avila on notice that it intends to terminate the business combination agreement (BCA),” Avila said. Avila said following internal discussions it feels that Insight’s decision is short sighted and does not change the company’s focus on its business plan and core businesses, “which are no different than what were presented to Insight at the time of the execution of the BCA,” the company said. Read More (Accesswire)

EdtechX II terminates zSpace deal. EdtechX Holdings Acquisition II in an 8-K disclosed it has terminated a merger agreement with zSpace, a provider of commercial augmented reality and virtual reality technology in the global education market. The SPAC said the decision to abandon the deal was “based upon certain breaches by zSpace of the terms of the merger agreement.” As announced in May 2022 the business combination implied a pro forma enterprise value of $195 million. EdtechX II has until Dec. 15 to secure and close another deal. Read More (SEC)

Kairous Acquisition and Wellous Group call off merger. Kairous Acquisition and Wellous Group Limited have mutually terminated their merger agreement, the SPAC disclosed in an 8-K filing. No reason was given for abandoning the deal. No termination fee or other payment is due to either party. The SPAC in December announced the deal with Malaysia-based Wellous Group, an Asia-based international nutrition company that develops, manufactures, markets and sells health and wellness products. Cash proceeds were to consist of Kairous’s approximately $21 million in trust. Read More (SEC)

TKB Critical Technologies 1 terminates Wejo deal. TKB Critical Technologies 1 in an 8-K said it has terminated a merger agreement with Wejo Group Limited, a global company engaged in cloud and software analytics for connected, electric and autonomous mobility. Neither party will pay a termination fee as the decision was reportedly mutual. The SPAC said it also sold most of its sponsorship investment to Roth Capital Partners and Craig-Hallum Capital Group. The buyers will receive 4,312,500 ordinary shares consisting of 4,237,500 Class A and 75,000 Class B shares and 8,062,500 private placement warrants for $1. As part of the sponsor transfer, TKB’s management team will resign. Roth and Craig-Hallum will provide $31,000 to the sponsor to pay outstanding invoices plus $300,000 for certain liabilities. Read More (SEC)

Tastemaker Acquisition abandons Quality Gold deal. Tastemaker Acquisition in an 8-K said its merger agreement with Quality Gold was terminated. According to an 8-K filing at deal announcement, the acquisition was to be structured as a “double dummy” transaction with five sub mergers leading to Quality Gold becoming the surviving parent company. The aggregate consideration to be paid to Quality Gold equity holders was to consist of up to $35 million in cash, 83.1 million newly issued shares of the parent company and deferred company shares, including 2,070,000 shares deferred by the SPAC’s sponsor. Tastemaker raised $276 million in a January 2021 IPO with stated plans at the time to focus on the restaurant, hospitality, and related technology and services sectors. Redemptions since then have eroded the trust considerably. Read More (SEC)

Digerati terminates deal with Minority Equality opportunities acquisition. Minority Equality Opportunities Acquisition in an 8-K said Digerati has called off their merger agreement. Digerati is a Hispanic-led and founded provider of cloud services specializing in UCaaS (Unified Communications as a Service) solutions for the SME market. The SPAC had postponed a shareholder vote on the merger five times in the last month, saying it was working to satisfy the closing conditions. MEOA reported that of the 728,815 shares tendered for redemption, the holders of 60,455 shares have withdrawn their redemption requests. That increased the total outstanding shares to 112,468 and lowered the redemption rate to 83% from 93%. The redemptions do not take effect until the closing of a business combination. Read More (SEC)

Welsbach Technology Metals acquisition and WaveTech call off merger. Welsbach Technology Metals Acquisition and WaveTech Group have reached a mutual decision to discontinue merger plans. The parties in a statement said current unfavorable market conditions do not provide an optimal environment for the planned integration. “While we had hoped to create significant synergies through the proposed merger, based on the current climate, we believe that our independent paths offer a more favourable strategy to create value and growth,” said Daniel Mamadou, CEO and chairman of Welsbach. He also thanked stakeholders in both companies for their patience. WaveTech specializes in next-generation battery-enhancing technologies. Read More (GlobeNewswire)

Battery manufacturer Sakuu terminates deal with Plum Acquisition I. Plum Acquisition in an 8-K said it received a deal termination notice from merger partner Sakuu. As a result, the SPAC said its board has decided not to extend the termination deadline beyond June 18 and will redeem shares, instead. Silicon Valley-based Sakuu is an additive manufacturing and solid-state battery company. The deal with Plum was announced three months ago at an implied enterprise value of $705 million. Plum I raised $300 million in a March 2021 IPO. Read More (SEC)

AUM Biosciences terminates deal with Mountain Crest Acquisition V. AUM Biosciences called off its proposed merger with Mountain Crest V, the SPAC disclosed in an 8-K. Announced in October, the deal had a pre-money equity value of $400 million. Terms had called for the target to receive the approximately $69 million of cash held in Mountain Crest’s trust account at deal announcement, although the SPAC’s shareholders redeemed more than 92% of the trust on an extension vote last month. Mountain Crest V had no other financing in place for the deal. Read More (SEC)

Malacca Straits Acquisition terminates Indiev deal. Malacca Straits Acquisition in an 8-K said it called off a $600 million merger agreement with EV maker Indiev and now intends to redeem shares effective June 16. The termination was by mutual agreement, the SPAC said, although no reason was given for abandoning the deal. Announced in September, terms had also called for earn-outs of up to $200 million in stock. Indiev founder and CEO Hai Shi had signed a PIPE subscription agreement to purchase $15 million in Malacca shares at $10 per share. The SPAC’s per-share redemption price is expected to be approximately $10.53. Read More (SEC)

Artemis Strategic Investment terminates Novibet deal. Artemis Strategic Investment in an 8-K filing said it has terminated a merger agreement with British gametech company Novibet. The termination was made under terms of the merger agreement that allowed the deal to be called off it had not closed by Dec. 30, 2022, which did not state why the SPAC waited another 5 1/2 months before walking away from the deal. Artemis said intends to identify another target business for an acquisition. Its termination deadline is July 4. The SPAC last September cut the closing consideration from $625 million to $500 million, but with the proviso that if redemptions hit 85% or more, Novibet would get additional share consideration of $125 million. Artemis also clipped the amount of cash required to be available to Novibet at closing from $50 million (after any redemptions) to $12.5 million. Read More (SEC)

Credit Suisse SPAC head Stabinsky leaves for Santander. Credit Suisse Group AG’s departures continue with its head of blank-check companies leaving after the fortunes of both the bank and the product have changed. Niron Stabinsky, the head of SPACs and permanent capital, is leaving the Swiss bank to join Banco Santander SA. Ryan Kelley, a Credit Suisse director, will also join Stabinsky at the Spanish lender. Santander has snapped up top bankers from Credit Suisse as uncertainties loom around the UBS Group AG merger brokered by the Swiss government. Read More (Bloomberg)

London-Listed SPAC New Energy One in talks about Eni North Sea merger. A London-listed SPAC vehicle advised by Amber Rudd, the U.K.’s former home secretary, is in talks to merge with a portfolio of carbon capture and storage (CCS) projects part-owned by Eni, the Italian energy giant. Sky News reports that New Energy One Acquisition Corporation is in advanced discussions about a combination with the Bacton and HyNet projects, which together will be capable of storing 20 million tons of carbon annually by 2030. A formal deal remains some way off, according to the report. Key details, including a precise valuation and the composition of the assets to be included in the merger, have yet to emerge. However, one energy sector banker said on Thursday that if completed, the combination would result in the public listing in London of one of the most significant energy transition-focused companies to date. Read More (Sky News)

|

Chart 3: SPAC Events – July 2023 (1/2) |

|

S. No |

Event Name |

Date |

Time |

|

1 |

PMGM & AEON Biopharma Merger Vote |

7/3/2023 |

4:30PM EST |

|

2 |

GLTA & Marti Merger Vote |

7/5/2023 |

10AM EST |

|

3 |

PBAX Deadline extension vote |

7/7/2023 |

11AM EST |

|

4 |

TMKR Deadline extension vote |

7/10/2023 |

12PM EST |

|

5 |

ADEX Deadline extension vote |

7/11/2023 |

9AM EST |

|

6 |

FACT & Complete Solaria Merger Vote |

7/11/2023 |

10AM EST |

|

7 |

ALPA & Carmell Therapeutics Merger Vote |

7/11/2023 |

11AM EST |

|

8 |

AVHI Deadline extension vote |

7/12/2023 |

10AM EST |

|

9 |

GLTA Deadline extension vote |

7/12/2023 |

10AM EST |

|

10 |

GAQ Deadline extension vote |

7/13/2023 |

8:30AM EST |

|

11 |

BSAQ Deadline extension vote |

7/13/2023 |

9AM EST |

|

12 |

ALSA Deadline extension vote |

7/13/2023 |

10AM EST |

|

13 |

CSLM Deadline extension vote |

7/13/2023 |

10AM EST |

|

14 |

DMAQ Deadline extension vote |

7/13/2023 |

10AM EST |

|

15 |

WNNR Deadline extension vote |

7/14/2023 |

10AM EST |

|

16 |

AFAR Deadline extension vote |

7/17/2023 |

8AM EST |

|

17 |

UPTD Deadline extension vote |

7/17/2023 |

9AM EST |

|

18 |

HUDA Deadline extension vote |

7/17/2023 |

10AM EST |

|

19 |

TRIS Deadline extension vote |

7/17/2023 |

10AM EST |

|

20 |

EVGR Deadline extension vote |

7/18/2023 |

9AM EST |

|

21 |

CLAY Deadline extension vote |

7/18/2023 |

10AM EST |

|

22 |

TETE Deadline extension vote |

7/18/2023 |

11AM EST |

|

23 |

CLBR & PublicSq. Merger Vote |

7/19/2023 |

10AM EST |

|

24 |

ACAQ Deadline extension vote |

7/19/2023 |

11AM EST |

|

25 |

KYCH Deadline extension vote |

7/20/2023 |

9AM EST |

|

26 |

BRLI Deadline extension vote |

7/20/2023 |

10AM EST |

|

27 |

KNSW Deadline extension vote |

7/20/2023 |

10AM EST |

|

28 |

ONYX Deadline extension vote |

7/21/2023 |

|

|

29 |

BLUA Deadline extension vote |

7/21/2023 |

11AM EST |

|

30 |

OPA Deadline extension vote |

7/24/2023 |

9:30AM EST |

|

31 |

APTM Deadline extension vote |

7/25/2023 |

11AM EST |

|

32 |

CHEA Deadline extension vote |

7/26/2023 |

9:30AM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

Chart 3: SPAC Events – July 2023 (2/2)

|

S. No |

Event Name |

Date |

Time |

|

33 |

HWEL Deadline extension vote |

7/26/2023 |

10:30AM EST |

|

34 |

GENQ & Environmental Solutions Group Merger Vote |

7/26/2023 |

11AM EST |

|

35 |

TLGA Deadline extension vote |

7/27/2023 |

10AM EST |

|

36 |

CPUH & Allurion Merger Vote |

7/28/2023 |

9AM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

|

Chart 4: SPAC Activity by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 5: Current Status of the SPAC Universe |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 6: Current Status of SPAC Universe by Trust Size |

|

|

Source: Intro-act, Boardroom Alpha

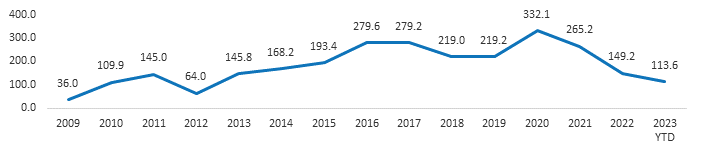

|

Chart 7: SPAC Transactions by Year |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 8: Average SPAC IPO Size ($ Mn) |

|

|

Source: Intro-act, Boardroom Alpha

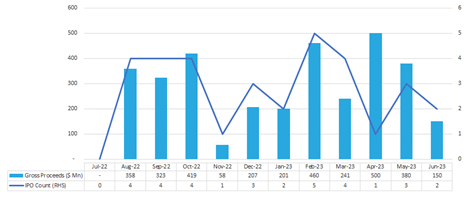

|

Chart 9: SPAC Transactions by Month (LTM) |

|

|

Source: Intro-act, Boardroom Alpha

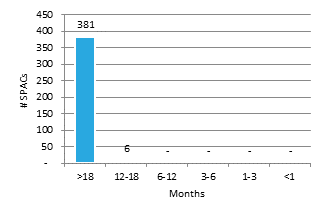

|

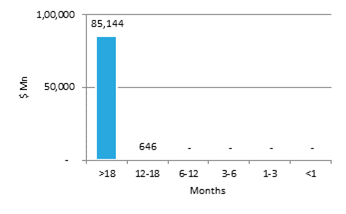

Chart 10: Time to Liquidation – By Volume |

|

Chart 11: Time to Liquidation – By Trust Value |

|

|

|

|

Source: Intro-act, Boardroom Alpha

|

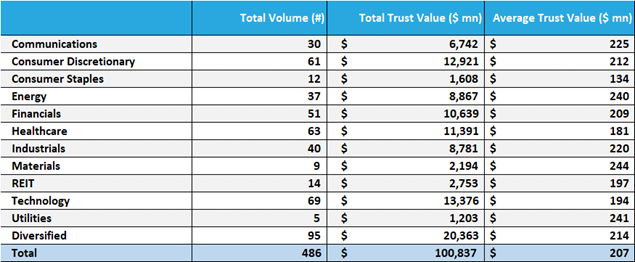

Chart 12: Active SPACs By Sector (As of Month Ending June 2023) |

|

|

Source: Intro-act, Boardroom Alpha

|

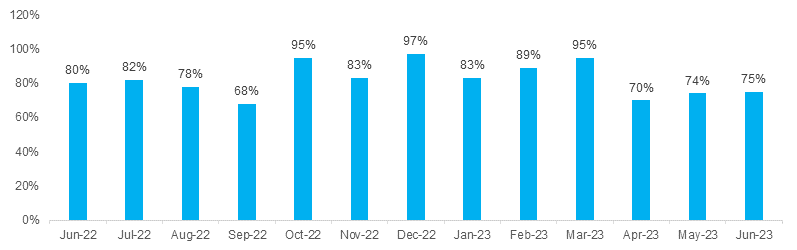

Chart 13: Average Redemption Rate by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 14: SPAC Redemption Detail – June 2023 |

||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 15: Monthly SPAC Activity – June 2023 |

|

|

Source: Intro-act, Boardroom Alpha. Searching figures ($Mn and Count) are as of month end.

|

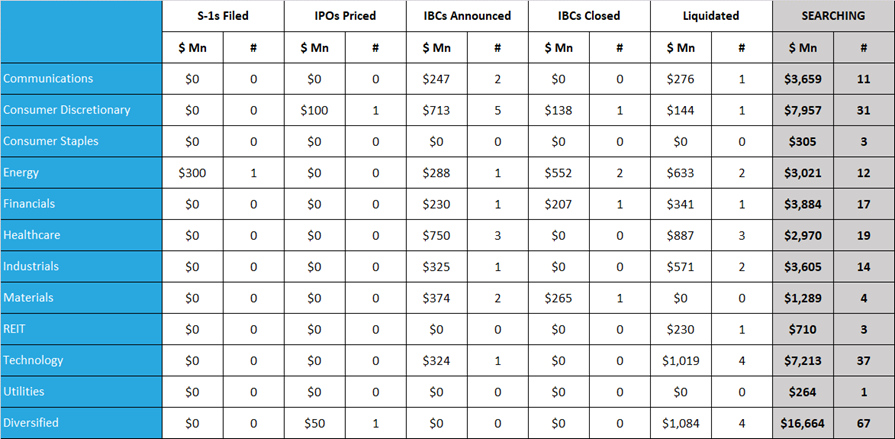

Chart 16: SPAC IBC Announcements by Target Sector – June 2023 (1/2) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

Chart 16: SPAC IBC Announcements by Target Sector – June 2023 (2/2) |

||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

The SPAC and New Issue ETF (SPCX). SPCX gives investors exposure to a broad portfolio of SPACs with the familiar attributes of an exchange traded fund’s diversity, tax efficiency and liquidity. SPCX is the first actively managed SPAC ETF. Why active? As the SPAC market is rapidly evolving, we believe that the portfolio management approach should equally reflect the dynamic nature of this burgeoning capital-raising alternative. This is no place for a rigid rules-based index strategy.

|

Chart 17: SPCX Summary Data |

|

Chart 18: SPCX Top 10 Holdings |

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

Source: Intro-act, ETF.com. Data as of 6/30/23.

|

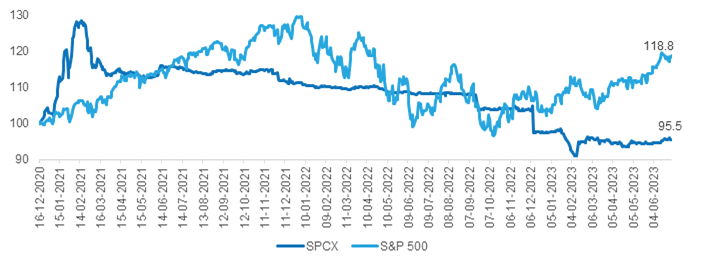

Chart 19: SPCX Performance |

|

|

Source: Intro-act, Yahoo! Finance. Data as of 6/30/23.

|

Chart 20: Relative-SPAC Index vs Russell 3000 |

|

|

Source: Intro-act, FactSet

|

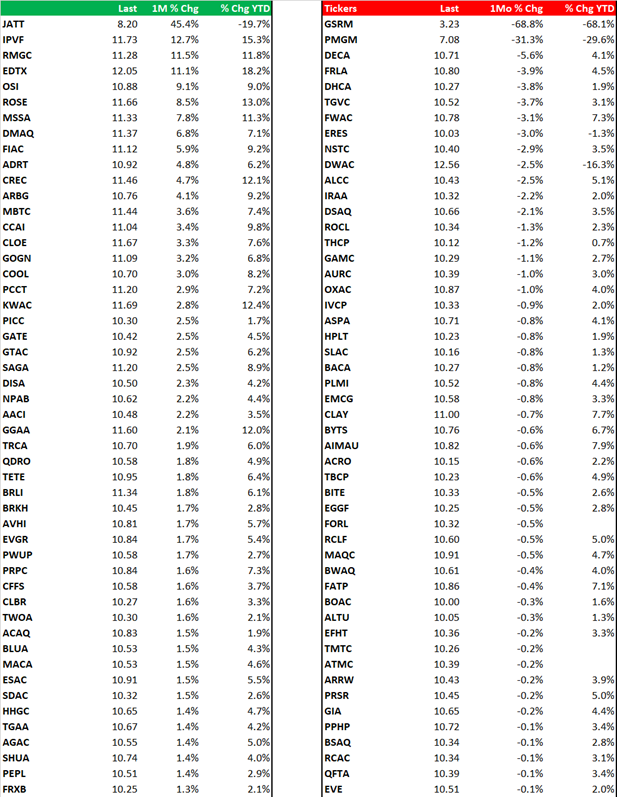

Chart 21: Gainers and Losers in the Broader SPAC Universe (% Change) |

|

|

Source: Intro-act, FactSet

|

Chart 22: SPAC IPO Pricings by Sector – June 2023 |

|||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 23: SPAC S-1 Filings by Sector – June 2023 |

||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 24: SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 25: DE-SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 26: SPAC Underwriter League (YTD As of June 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Bookrunner Volume ($ Mn) is based on the total amount of the offering sold, including over-allotment. Full credit is awarded to the sole book-runner or split equally among joint book-runners.

|

Chart 27: Top De-SPAC Advisors (YTD As of June 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Advisor credit is shared equally among all advisors on a given deal, as a proportion of the enterprise value of the target company acquired by the SPAC. Firms with multiple advisory roles receive credit for each role.

|

Chart 28: SPAC Legal League (YTD As of June 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Volume ($ Mn) is awarded to both Issuer and Underwriter Counsel.

|

Chart 29: SPAC Auditor League (YTD As of June 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research

|

Chart 30: ICR – The Leading SPAC Communications and Capital Markets Advisor |

|

113 Transactions / $267 Billion in Transaction Value Since 2021

|

Source: Intro-act, ICR. Announced SPAC transactions since 2021, All Announcements not shown. Data as of April 2022.

Analyst Certification

I, Peter Wright, certify that the views expressed in the research report accurately reflect my personal views about the subject securities or issues. I also do not receive direct or indirect compensation based on my recommendations or views.

Intro-act, Inc. (Intro-act) issued this report and may seek fees for the assistance with investor targeting, access, and further investor preparation services. Intro-act, Inc. will not seek renumeration for any investment banking service or investment advice.

Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources who are believed to be reliable. However, the issuer and related parties, as well as Intro-act, do not guarantee the accuracy or completeness of this report, and have not sought for this information to be independently verified. Opinions contained in this report represent those of the Intro-act analysts at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, and estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties, and other factors that may cause the actual results, performance, or achievements of their subject matter to be materially different from current expectations.

Exclusion of Liability: To the fullest extent allowed by law, Intro-act, Inc. shall not be liable for any direct, indirect, or consequential losses, loss of profits, damages, or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this note.

No personalized advice: The information that we provide should not be construed in any manner whatsoever as personalized advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Intro-act’s solicitation to affect, or attempt to affect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors.

Investment in securities mentioned: Intro-act has a restrictive policy relating to personal dealing and conflicts of interest. Intro-act, Inc. does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees, and contractors of Intro-act may have a position in any or related securities mentioned in this report, subject to Intro-act’s policies on personal dealing and conflicts of interest.

Copyright: Copyright 2023 Intro-act, Inc. (Intro-act).

Intro-act is not registered as an investment adviser with the Securities and Exchange Commission. Intro-act relies upon the “publishers’ exclusion” from the definition of investment adviser under Section 202(a) (11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Intro-act does not offer or provide personal advice, and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell, or hold that or any security, or that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.