Q&A OF THE MONTH – ZAPATA AI

Zapata AI is an Industrial Generative AI software company. In this month’s Q&A, we learn about its products and services, differentiators, the market opportunity for Generative AI, Zapata’s growth strategy, and the proposed business combination with Andretti Acquisition Corp.

Q: Can you describe your business and what differentiates Zapata AI from other AI-focused companies?

A: Zapata AI is an Industrial Generative AI software company that develops generative AI applications and provides accompanying services to solve complex industrial-scale problems. Our computational approaches leverage the statistical advantages of math based on quantum physics.

We offer Industrial Generative AI solutions designed to address common computational challenges faced by enterprise customers — large businesses that have the size and resources to dominate a specific market, high revenue and a significant number of employees. Our subscription-based solutions combine software and services to develop custom Industrial Generative AI Applications designed to resolve the highly complex business challenges of these enterprises arising from the size and scope of their global operations.

Some of our customers, which span multiple industries across multiple countries, include or have included BASF, BBVA, BP, DARPA and Andretti Autosport. We also have relationships with third party vendors and service providers such as IBM, NVIDIA and IonQ, which we refer to as the “Zapata AI partner ecosystem.” The products and services provided by these partners extend and complement our Industrial Generative AI solutions and facilitate their development and deployment.

We expect to be the first publicly traded, pure-play Industrial Generative AI software company that is focused on the technically challenging industrial problems of enterprise organizations.

Unlike other vendors in the much broader AI market category, we focus on generative AI while using both quantum and classical techniques in our work. Specifically, our specialized generative AI software category, which we refer to as “Industrial Generative AI,” takes generative models similar to those behind popular generative AI tools, such as OpenAI’s ChatGPT and Google’s Bard, and tailors them to domain-specific applications, with a focus on computationally complex problems found across industries.

We refer to these computationally complex problems as industrial problems. They are found in every industry, not just those typically considered “industrial,” and are defined by several common challenges, including: data disarray, large solution spaces, unpredictability, time sensitivity, compute constraints, a demand for accuracy and reliability, and enterprise security requirements.

Q: Please tell us more about Zapata AI’s products and services.

A: We have a suite of three subscription-based Industrial Generative AI offerings that include software and software tools supported by services. Our software offers our customers flexibility in selecting computing resources, including classical, high performance, and quantum computing hardware, as well as deployment environment options, cloud, private cloud, and on-premise. Using techniques based on the math of quantum physics, we can apply our software tools to specific industrial applications and tailor those applications to our customer’s relevant hardware. These offerings consist of:

· Zapata AI Sense: A suite of algorithms and complex mathematical models to enhance analytics and other data-driven applications. Virtual sensors are one such use case.

· Zapata AI Prose: Our set of generative AI solutions based on large language models (LLMs), similar to widely used generic chatbot applications but customized to an enterprise, its industry, and its unique problems.

· Orquestra®: Our Industrial Generative AI application development platform on which we provide Sense and Prose to customers.

The Industrial Generative AI applications we can build and operate with these tools securely address customers’ problems with both numerical and text processing capabilities.

We envision opportunities for Zapata AI to utilize its software tools in almost any industry. Some examples of problems for which we believe our Industrial Generative AI applications could be designed to address include helping a banking institution optimize its financial portfolio or helping a pharmaceutical company with drug discovery. In November 2023, we announced a collaboration with Sumitomo Mitsui Trust Bank (SMTB) to model financial time series data using generative AI enhanced with quantum science. The generative AI applications that Zapata AI and SMTB research and develop will serve to simulate financial scenarios and more accurately price derivatives and value adjustments.

We believe our Industrial Generative AI solutions can drive better data understanding, create more accurate predictions, reduce risk, shorten time to value, and optimize decision-making. In short, our expertise helps our customers to formulate a problem correctly, apply the right mathematical tools to solve it, and stand up the correct data and computing infrastructure to match the needs of the problem. Additionally, with our platform in place, our customers upgrade their computational agility and are in a position to continuously adopt the latest advances in hardware (both quantum and classical computing), generative AI and machine learning due to the Orquestra platform’s flexible, modular framework that allows for interchangeable components.

Q: What is the market opportunity for Generative AI?

A: The potential impact of generative AI on productivity is substantial. A McKinsey & Company report has estimated that generative AI could eventually add $2.6 trillion to $4.4 trillion in economic benefits annually across a set of 63 selected use cases. Additionally, a Bloomberg study has found that the generative AI market could grow to $1.3 trillion by 2032, including about $280 billion of new software revenue.

The total addressable market described above includes all forms of generative AI. However, we have found that public attention tends to focus on foundational model LLMs such as GPT-4. Such focus overlooks that opportunities for generative AI may also include:

· The applications of generative AI modeling to a wider range of problems in industrial settings, which involve mostly numerical data; and

· The ability to enhance human interactions and language-based tasks with customer-specific AI models leveraging LLM capabilities.

We believe that a substantial portion of this broader market – including industrial use cases involving numerical data as well as customer-specific LLMs – will be accessible only to companies that possess:

· The internal generative AI expertise required to formulate use cases in terms of a problem that generative AI can solve;

· The ability to apply generative AI to their numerical data;

· The ability to deploy models within the constraints (e.g., time, accuracy, security, monetary cost of running models) of their infrastructure and performance requirements; and

· The tools to quickly stand-up applications of generative AI and other types of AI to leverage customer data.

In summary, we believe that the market opportunity is broader than the LLM applications typically associated with generative AI and includes an opportunity for applications involving numerical data, and offering both Prose and Sense gives us the flexibility to develop applications for Industrial Generative AI in both of these markets.

Q: What is Zapata AI’s growth strategy?

A: Our business model is to provide subscription-based offering that combines Zapata AI software —specifically the Orquestra platform and any Prose or Sense solutions delivered on top of it — as well as services to develop custom Industrial Generative AI applications designed to resolve our enterprise customers’ specific problems. Our growth strategy involves two major routes to market:

· Direct Sales: Sales to large accounts with multi-year agreements and land-and-expand account strategies.

· Partners: Sales via formal and informal partnerships with system integrators and consulting services firms.

As part of our growth plans, we expect to sell to, with, and through partners, deepening the potential impact of the Zapata AI partner ecosystem. Repeatable solutions built with services firms are a major part of our growth strategy. By repeatable solutions, we mean solutions for industry use cases that can be resold to other companies within the same industry.

We expect that working with service firms will enable us to grow faster by delivering these repeatable solutions to our partners’ existing client ecosystems and leveraging our partners’ sales and post-sales resources. We believe partners will assume an active role in the sales and post-sales cycles, such as project management, strategy and transformation, change management, and data management.

Today, we have a global presence, centered mostly around North America, but with several active business development activities in Asia, including Japan and Singapore, and Europe, including the United Kingdom, Spain and Denmark.

Q: Why does it make sense to go public?

A: Through the proposed business combination with Andretti Acquisition Corp., we can become what we believe would be the first publicly traded, pure-play, industrial generative AI company. This move reflects the next phase of Zapata AI’s evolution and would provide the company with access to the public capital markets to fund our future growth. Any net proceeds from our business combination will also help strengthen our balance sheet and fuel continued innovation, drive enterprise customer acquisition and advance our growth strategy.

In a large and rapidly growing total addressable market, we have proprietary, Industrial Generative AI techniques and algorithms that we believe are at the leading edge of these new frontiers. Based on our data, we have determined that these techniques are capable of demonstrating a 10X to 1000X improvement in modeling performance depending on the use case, and Zapata AI leverages its proprietary, full-stack software platform to bring these improvements to enterprise use cases.

We believe we have substantial near-term enterprise revenue opportunities with our LLM capabilities and other AI models for synthetic data, simulation and optimization, in addition to our pioneering, founder-led, and visionary management team and board with a track record of execution and growth.

Q&A Of The Month – Ian Chan, CEO & Co-Founder Abpro Corporation

Abpro is a cutting-edge company developing next-generation antibody therapeutics. In this month’s Q&A, Abpro CEO & Co-Founder Ian Chan discusses the company’s proprietary platforms, pipeline, market potential, vision, and the proposed business combination with Atlantic Costal Acquisition Corp. II

Q: Can you introduce us to Abpro?

A: Abpro is a cutting-edge company developing next-generation antibody therapeutics. We founded the company with the sole goal of improving the lives of patients with severe and, quite often, life-threatening diseases. We started our business over 10 years ago out of Kendall Square in Cambridge, MA and we are positioned for growth.

Q: Tell us about your proprietary platforms? How were they evaluated?

A: We have two antibody discovery and engineering platforms, DiversImmune® and MultiMab™ and we are working to develop best in class antibodies, which have been validated by over 300 companies including global pharmaceutical companies and big biotech. Data supporting our antibodies has also been published in leading publications like Nature and New England Journal of Medicine.

Q: What can you tell us about Abpro’s pipeline?

A: We have a lot going on. Abpro’s pipeline is positioned in three areas for best in class antibodies. Immuno-oncology is the largest effort in our pipeline, where we have a lead molecule that we’ve developed in breast cancer and gastro cancer. In eye care, we are targeting diabetic macular edema and Wet AMD, which like oncology, is a blockbuster indication. We also put quite a bit of effort into advancing in the Covid arena, because there was and remains a huge unmet medical need there for immune-compromised individuals

Q: I also noticed you have a strong management team, what can you tell me about them?

A: We are fortunate to have a stellar team and advisors. We are directed by a team with extensive experience, who have all had highly successful careers including: Dr. Bob Langer, who is the co-founder of Moderna, Laurie Glimcher, President and CEO of The Dana-Farber Cancer Institute, and Ronald Levy, MD from Stanford, California who was instrumental in the overall success of Biogen-Idec.

Q: Ian tell me about your background and how you got into running a life sciences company?

A: I studied Pre-Med at Brown as an undergraduate student, but I also was drawn to economics as well. I started my career working on Wall Street at Bear Stearns and Morgan Stanley for three years, but I wanted to combine science with business. I didn’t go straight into the medical space because I thought that if we delivered advance therapies to the many people who need it, through a company, that would help a lot of patients around the world. I knew I needed to learn more about how successful companies operate in order to build a company that could do this. Now that I had gained experience in both fields, I felt that I could combine my knowledge from the two areas and create this vision. The first company came about because of my brother, who is a Harvard MD graduate. At age 23 and age 25, we created a company with Craig Venter focusing on high speed sequencing. Along the way, I completed my MBA at Harvard, as well, which, coupled with my professional experience, gave me the tools to start Abpro.

Q: And then Abpro?

A: Yes, then Abpro was founded a little bit over 10 years ago so we’ve been able to gain a lot of experience in the antibody field.

Q: What’s your international business market look like?

A: It’s very promising right now. There have been many inbound inquiries and discussions. I think everybody's interested in new, innovative therapies to better treat patients. Essentially, there are opportunities really to help many people around the world.

Q: Do you do have some work going on with Korea. Correct?

A: Yes, we have a great partnership with the leading South Korean biopharmaceutical company, Celltrion, and with some well-known, highly respected South Korean investors. Last year we signed a $1.8 billion partnership with them to advance our ABP 102 antibody, which targets HER2 + tumors, including breast and gastric cancers. We are very excited about this treatment and this continued partnership.

Q: What's your vision for? Abpro moving forward?

A: First and foremost, we want to help patients. So that's always been our primary goal, since the beginning. We will try to help as many people as possible. Early on, we realized there was a major bottleneck at the discovery stage. We found that it was too slow, which led us to creating our platform. Abpro recognized antibodies as a very natural modality that is safe and effective – innovative antibodies are the overall foundation of our company. This has also led us to our long-term goal, which is to build the leading next generation antibody company. Antibodies have been the largest treatment for oncology patients over the last 30 years. Even during the Covid pandemic, it was antibodies that were the number one modality for treatment. This highlights the importance and effectiveness of antibodies, and why Abpro has chosen to utilize this method as its foundation. We strongly believe that antibodies are the key to helping the most patients who suffer from critical illnesses.

Q: What lead your management team to pursue a SPAC as opposed to a traditional IPO?

A: We had options on both sides and, fortunately, we have very supportive investors. Even though SPACs are out of favor right now the markets are starting to pick up. I would say the flexibility of the SPAC is actually what appealed to us. We went in with our eyes wide open. We knew that there was going to be public sentiment about pursing a SPAC. Our investors have embraced this opportunity. Our partner Atlantic Costal Acquisition Corp. II, is a very sophisticated and informed group in the biotech space. We were introduced to Atlantic Costal Acquisition Corp. II by our investment bankers and it was an ideal match. The deal has an implied pre-money equity valuation at $500 million and will propel the company forward and help us move our molecules deep into the clinic.

Q: Anything else you would like to share Ian?

A: Our number one focus is our overall mission, which was to help as many patients as possible. Right now, Abpro is at an inflection point. We are putting all our attention on advancing our pipeline, creating new therapies, supporting our team, and helping advance long-term shareholder value, and with these components we can look forward to a successful future.

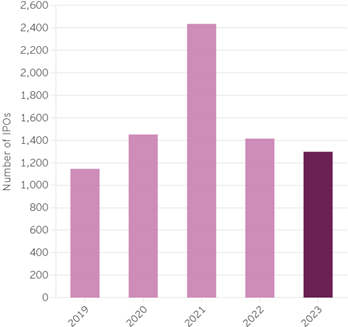

Multiple crosswinds superseded global IPOs despite market rally in 2023. The global IPO market closed 2023 with 1,298 IPO raising US$123.2b. Overall the global IPO market in 2023 has experienced shifting landscapes with improved Western market sentiment counterbalanced by China's cool-down, as well as a contrast between hot developing market small-cap deals and lackluster large offerings. When comparing to 2022, IPO proceeds in 2023 lagged last year's tepid pace by roughly a third, although deal volumes have picked up in both the Americas and EMEIA regions. Despite a strong market rally and low volatility index on the back of positive economic data, public offerings have remained subdued in many developed markets, with the exception of a brief September window in the U.S. Read More (EY)

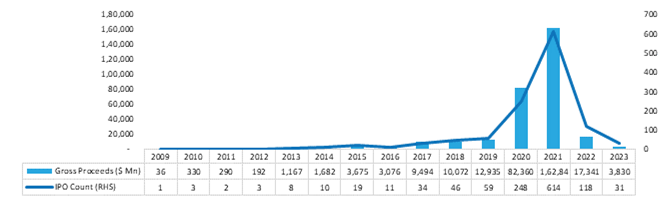

Chart 1: Global IPO activity by number of IPOs |

|

|

Source: Intro-act, EY

SPAC companies accounted for at least 21 bankruptcies in 2023 and a staggering $46 billion in lost investor value. Wall Street’s affair with blank-check firms, the finance fad that pushed companies onto the stock market during the Covid-19 pandemic, ended this year with a string of big bankruptcies and even bigger losses for shareholders. At least 21 firms that went public by merging with special purpose acquisition companies, or SPACs, went bankrupt this year, according to data compiled by Bloomberg. Measured from their peak market capitalizations, the insolvencies bookend the loss of more than $46 billion of total equity value. The failures span money-losing electric vehicle startups and forward-thinking farming companies. Blank-check firms were good at propelling their targets to the public market even when they lacked well-formed financials, said Gary Broadbent, an executive guiding former SPAC AppHarvest Inc. through its liquidation. Many weren’t “ready for primetime,” he said. Read More (Fortune)

SPACs flop in 2023 as 40% of IPOs fail to find a target. The craze for blank-cheque companies in 2021 is coming home to roost, with nearly $79 billion in capital raised by SPACs two years ago failing to find a target and falling into liquidation. The flurry of Spacs reached a peak in 2021, with a frenzy of launches raising a record $172 billion. But 40% of the 690 Spacs launched that year have now been liquidated, according to data provider Dealogic. Read More (Financial News)

What to look for in the IPO market in 2024. The IPO landscape in 2024 is shaping up to be a dynamic one, with several high-profile companies expected to go public. However, market conditions and investor sentiment will play a significant role in determining the success of these IPOs. Companies considering going public should be prepared to demonstrate their financial health and potential for value creation to attract investors in this challenging market. Several high-profile companies are expected to make their market debut in 2024. Among the most anticipated are Stripe, Databricks, and Reddit. These companies have been on the radar of investors for years, and their potential IPOs represent some of the most significant market events to watch for in 2024. Read More (The CFO)

Tepid IPO market shows little sign of strengthening heading into 2024. Stock market volatility, rising interest rates, and balance-sheet losses roiling the banking sector kept the market for initial public offerings (IPOs) chilly this year, and it shows little signs of warming in 2024. As of Dec. 19, 108 companies have priced IPOs in U.S. markets, a 52% increase from the same time last year. That's the third-fewest in the past decade and 73% lower than the record highs of two years ago. Javier Avalos, co-founder and CEO of Caplight, which tracks trading in shares of private companies that comprise the breeding ground for IPOs, said it doesn't appear the market will thaw soon. "The pre-IPO market is not really expecting a flurry of IPO activity in early 2024," Avalos said, adding that most investment banks have mostly clear IPO calendars in the first half of the new year. Read More (Investopedia)

What is the outlook for IPOs in 2024? Here's the companies to watch. With 2023 being somewhat disappointing in terms of initial public offerings, investors are looking ahead to see what’s in store for the IPO market in 2024. This year saw about 968 initial public offerings (IPOs) around the world in the first three quarters of the year. This was a fall of about 8% compared to 2022. However, 2024 offers a glimmer of hope for the IPO market. This is due to investors anticipating several major central banks, such as the US Federal Reserve and the European Central Bank, to start cutting interest rates. Several companies which went public this year have had lacklustre beginnings, trading just around or below their offering prices. These include semi-conductor company Arm Holdings, healthcare company Kenvue, footwear manufacturer Birkenstock - and delivery company Instacart, among others. Read More (EuroNews)

IPOs in 2024 could bring over $100 billion to stock markets – but which ones will win the race? Experts the world over have anticipated a ‘soft landing’ end to 2023 and a much milder, more dovish 2024 as inflation and interest rates progressively lower. And so it is that investors’ eyes have turned more and more away from bearish asset classes and started eyeing up equities again. The stock market has noticed it too, with several of 2023’s most anticipated IPOs having delayed their launches to 2024. Now, with 2024 in sight, these titan stock market debuts could collectively be worth more than $100 billion – Stripe alone accounts for about half of that by all accounts – and the year promises to be one for the books when it comes to hot newly minted public companies. With so much to choose from, it can be hard to keep track. Which is why we’ve rounded up the six top IPOs expected for 2024 right here. Read More (Investors Observer)

The Fed watcher who called the 2007 housing bubble expects interest rates to stay high for ‘much, much, much longer.’ It’s payback for the unsustainable ‘free money era’. Jim Grant has been tracking the ins and outs of Federal Reserve policy and its effects on the economy and markets in his famed newsletter, Grant’s Interest Rate Observer, for over 40 years. The always bow-tied and often staunchly skeptical economic historian has made a name for himself with some pretty prophetic forecasts ahead of past financial calamities, including the Global Financial Crisis. Read More (Fortune)

De-SPAC audits fall short on revenue and controls, review finds. U.S. auditors struggled with verifying revenues for newly minted public companies that had merged with a SPAC, according to audit inspections that targeted the complex transactions. The Public Company Accounting Oversight Board looked at how the six largest US firms handled 20 inaugural audits after clients went public either through a traditional IPO or by merging with a special purpose acquisition company. Inspectors found fault with four of the post-mergers, or de-SPAC, audits, according to a report. Read More (Bloomberg Tax)

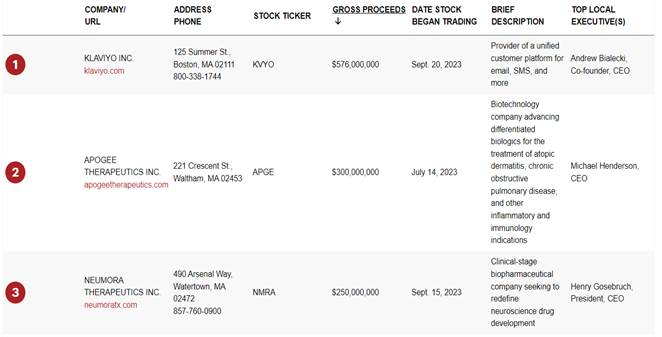

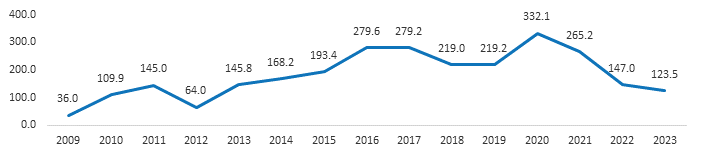

The largest IPOs and SPAC deals in Massachusetts of 2023. This list is based on data concerning the largest initial public offerings of Massachusetts-based/co-headquartered companies, as obtained from public filings and BBJ research, as of Nov. 1, 2023. This year's list includes companies that have begun trading publicly after combining with a special purpose acquisition company (SPAC). "Amount raised" refers to the gross proceeds from the offering at the time the pricing of the company's IPO/SPAC deal was announced. Read More (Boston Business Journal)

Chart 2: The Largest IPOs and SPAC deals in Massachusetts of 2023 (Ranked by Gross proceeds) |

|

|

Source: Intro-act, Boston Business Journal

Innovation in SPAC market is challenging. The SPAC sector has seen two notable attempts at innovation since 2021, one offered by serial SPAC sponsor Eagle Equity Partners, the other by Pershing Square Capital Management LP. But neither had attracted imitators, The Deal reports. In January 2021, Eagle Equity registered Spinning Eagle Acquisition Corp., a SPAC that aimed to raise $2 billion with Goldman Sachs & Co. LLC as sole underwriter. While the size of the raise and the single underwriter were notable, what set the registration apart was the SPAC’s structure. Eagle Equity proposed that if it didn’t need all of its capital for an acquisition, it would spin off a second SPAC with the remaining capital. That SPAC could then do a second transaction. The proposed structure would give the SPAC the option of merging with a large target company or doing multiple deals. Any spinoff transaction would have to be completed under the timeline for the first SPAC. Read More (DealFlow’s SPAC News)

SPAC mania’s ugly end yields $46 billion of investor losses. Wall Street’s affair with blank-check firms, the finance fad that pushed companies onto the stock market during the Covid-19 pandemic, ended this year with a string of big bankruptcies and even bigger losses for shareholders. At least 21 firms that went public by merging with special purpose acquisition companies, or SPACs, went bankrupt this year, according to data compiled by Bloomberg. Measured from their peak market capitalizations, the insolvencies bookend the loss of more than $46 billion of total equity value. The failures span money-losing electric vehicle startups and forward-thinking farming companies. Read More (Bloomberg Law)

SPACs stumble on accounting rules for backup financing deals. Thorny accounting issues continue to dog some de-SPACs. The latest: how to account for certain types of backup funding arrangements used by SPACs to ensure their deals to take companies public go through even if investors bail. Three companies that went public via SPAC merger in the past month have flagged errors serious enough to require restating, or redoing, their past financial statements, recent filings show. The companies – hearing loss device maker Envoy Medical, renewable energy technology firm Electriq Power Holdings Inc., and biopharmaceutical company Ocean Biomedical Inc.– said they tripped up in accounting for backstop financing arrangements, Bloomberg reports. Read More (Bloomberg Tax)

Is it SPAC to basics in the British Virgin Islands? The special purpose acquisition company (SPAC) boom is over, but not the SPAC market, as it enjoys a "return to mean" and very possibly a soft landing in this part of the Caribbean. The mood among influential market participants remains cautiously optimistic. After all, the SPAC remains a more efficient, quicker and price-certain route to market than most alternatives. Even in the current market, SPACs and de-SPACs still accounted for over 50% of US public market entries in 2023. Read More (Lexology)

Global venture funding in November slows at early stage. Global venture funding reached $19.2 billion in November 2023, down marginally month over month, Crunchbase data shows. Funding fell around 16% from the $23 billion invested in November 2022, which was already down by two-thirds from November 2021. Early-stage funding declined the most year over year – falling 34% – an indication that venture investors continue to scale back even when investing in younger startups. Seed funding slowed more than 15%. In contrast, late-stage funding increased by around 7% compared to November 2022. All told, venture funding to U.S. companies in November reached close to $9 billion – slightly less than 50% of total global funding. Read More (Crunchbase)

SEC enforcement activity: Public companies and subsidiaries – FY 2023 key trends. The SEC noted cooperation by 69% of public companies and subsidiaries that settled in FY 2023, the third highest of any fiscal year in the Securities Enforcement Empirical Database (SEED). Of the cooperating defendants that settled, 13% had no monetary settlements imposed. Of the new actions filed against public companies and subsidiaries in FY 2023, more than two-thirds (69%) included at least one cooperating public company or subsidiary. Of the 70 cooperating defendants, 14 were charged as part of the SEC’s sweep for recordkeeping failures related to off-channel communications. Read More (JD Supra)

Former Nikola CEO Trevor Milton sentenced to 4 years in prison for fraud. Trevor Milton, the founder and former CEO of the electric carmaker Nikola, was found guilty last year of defrauding investors, CNBC reports. His trial, and that of Elizabeth Holmes of Theranos, were seen as tests for whether start-up founders could be held liable for exaggerated claims to promote their company’s prospects. Nikola in December 2021 agreed to pay $125 million to settle a lawsuit by the SEC. The truck-maker, which was founded by entrepreneur Milton, went public via a SPAC reverse merger in June 2020 with VectorIQ Acquisition. Shares in the company took off that summer, riding investor enthusiasm for all things EV. Investors pushed the value at one point to above $34 billion – a market cap greater than Ford and Stellantis – even though Nikola had never made an automobile for sale. Read More (CNBC)

SEC charges SPAC, sponsor, merger target, and CEOs for misleading disclosures ahead of proposed business combination. The Securities and Exchange Commission today announced charges against special purpose acquisition corporation Stable Road Acquisition Company, its sponsor SRC-NI, its CEO Brian Kabot, the SPAC’s proposed merger target Momentus Inc., and Momentus’s founder and former CEO Mikhail Kokorich for misleading claims about Momentus’s technology and about national security risks associated with Kokorich. The SEC’s litigation is proceeding against Kokorich, against whom the SEC filed a complaint in the U.S. District Court for the District of Columbia. All other parties are settling with the SEC, with terms including total penalties of more than $8 million, tailored investor protection undertakings, and the SPAC sponsor’s forfeiture of founder’s shares it stands to receive if the merger, currently scheduled for August 2021, is approved. Read More (SEC)

Is Richard Branson giving up on Virgin Galactic (SPCE) stock? Space is the final frontier – and it looks to stay that way after Richard Branson ruled out further investment in Virgin Galactic (NYSE: SPCE), his troubled space tourism company. Shares of SPCE stock have fallen more than 15% today after Branson, who helped found Virgin Galactic and take it public in an early special purpose acquisition company (SPAC) deal, said he was tapped out. Virgin Galactic came public in 2019 as one of the first SPAC deals of the recent SPAC craze. The company partnered up with Chamath Palihapitiya’s Social Capital Hedosophia. SPCE stock enjoyed support in 2021, rising to well over $50 per share. Once the Federal Reserve began raising interest rates, however, capital became harder to come by. Equity investment now must compete for capital with bonds that offer a solid return. This is as true for Branson’s empire as it is for anything else. Branson told Financial Times that he no longer has the “deepest pockets” but that Virgin Galactic can succeed on its own. Read More (Investor Place)

Ex-SPAC Nogin goes bankrupt, plans sale to B. Riley Unit. Nogin Inc., provider of e-commerce services for the likes of Kenneth Cole, bebe, Scotch & Soda and other retail brands, filed bankruptcy with a plan to sell the business to a subsidiary of B. Riley Financial Inc. Nogin, which went public via merger with a blank-check company just last year, filed Chapter 11 late Tuesday in Delaware. It plans to implement a restructuring deal that would see B. Riley’s investment unit provide $24.7 million of new financing and ultimately take over the company, court papers show. Tustin, California-based Nogin blamed its bankruptcy primarily on deals with some of its retail partners that required the business to purchase their inventory. Read More (Bloomberg Law)

X-energy adds $80 million to Series C round after SPAC pull. Nuclear reactor developer X-energy said it completed a Series C financing round with an additional $80 million from its founder and from investment firm Ares Management. Why it's the BFD: The added sum brings the total raised in the round to $235 million and comes just weeks after X-energy canceled its SPAC with Ares. Details: In addition to Ares and X-energy founder Kam Ghaffarian, investors in the round included Ontario Power Generation, Curtiss-Wright Corporation, DL E&C, and Doosan Enerbility. What they're saying: "X-energy is developing the Xe-100, a high-temperature gas-cooled advanced small modular reactor, its proprietary TRISO-X fuel, and a mobile microreactor to safely and efficiently deliver affordable zero-carbon energy to people around the world," the company said in a press release. Read More (Axios)

Data firm Near Intelligence files for bankruptcy months after going public via SPAC. Near Intelligence Inc., a publicly traded software firm that provides data insights to major companies including Wendy’s Co. and Ford Motor Co., filed for bankruptcy with plans to sell itself. The Pasadena, California-based company listed estimated assets of at least $50 million and liabilities of $100 million, according to court papers. The bankruptcy filing lets Near Intelligence continue operating while it pursues a court-supervised sales process, according to a statement. Blue Torch Capital, a private credit firm that focuses on middle-market companies, has provided an opening offer of at least $50 million for its assets. Blue Torch Finance will lend the company $16 million to help it keep operating, the statement said. Read More (Bloomberg)

Houston Natural Resources Corporation (OTC: HNRC) thrives with SPAC launch, property acquisitions, and financial milestones. Houston Natural Resources Corporation (OTC: HNRC), engaged in oil and natural gas exploration along with energy transition resources, recently launched its own Special Purpose Acquisition Company (SPAC) known as HNR Acquisition Corp. SPACs are recognized as special purpose entities designed to expedite the process of taking private companies public. Lately, these entities have gained significant popularity, facilitating swift business combination transactions such as mergers, share exchanges, share purchases, and asset acquisitions involving one or more businesses. Operating independently, HNR Acquisition Corp. is engaged in the development, exploration, acquisition, and production of oil and gas properties situated in the Permian Basin. Read More (Market Screener)

SoundHound AI: Awesome tech, but 45 million reasons for caution. SoundHound AI deals in conversational intelligence. Its products include Smart Answering, Smart Ordering, and Dynamic Interaction. The technology is incredible and a quantum leap from voice recognition currently used by many companies. For instance, if you have recently filled a prescription over the phone, or dealt with an automated customer service, the phrases it understands are pretty limited - "yes," "no," and "main menu." And most of us end up yelling "operator" to get to a human for anything important. But the future looks different. SoundHound's demo shows that a customer at a fast-food-type restaurant can create a complex order smoothly in real time. "Give me two cheeseburgers, no onion, a diet coke, and medium fries. Make that a small fry. What deserts do you have"? And the kiosk understands, updates, and offers options. Read More (Seeking Alpha)

Digital World provides update on PIPE elimination. Digital World Acquisition, the SPAC that has been trying for more than two years to take Donald Trump’s social media company public, today updated the status of its PIPE reduction. The private investment originally stood at $1 billion, although delays in closing the merger caused some investors to pull out more than a year ago. Then, in October, the SPAC announced it was working to eliminate the PIPE altogether. Both Digital World and Trump Media & Technology Group presented this news as a positive development, which raised eyebrows among many observers. The PIPE investors had the right to terminate their subscription agreements at any time if the deal had not closed by Sept. 20, 2022. Some of the original PIPE investors pulled out a year ago, taking $138.5 million with them out of the initial $1 billion. Read More (SEC)

Lucid Motors stock: What went wrong with this ‘Tesla Killer’? In June 2021, shortly after its mega listing, Lucid Motors (LCID) CEO Peter Rawlinson said in an interview that the company was looking to make the electric vehicle (EV) industry into a “two-horse race” – with Tesla (TSLA), of course, being the other horse in the race. Cut to 2023, and Lucid is looking to produce only 8,000-8,500 cars this year – which is even below the 12,000 that it projected at the beginning of the year, and a tiny fraction of the 49,000 that it predicted in 2021 ahead of the SPAC merger. Far from being a potential “Tesla killer,” as it was labeled by some, Lucid is now looking like an “also ran” - and many fear whether the company will even survive the current EV industry slump. The recent departure of its CFO Sherry House is not building any confidence, either. Read More (The Globe and Mail)

Apex Plans to go public following scrapped SPAC. Apex FinTech has reportedly filed confidentially for an initial public offering (IPO). The Dallas-based clearing company had planned to go public through a special purpose acquisition company (SPAC) merger in 2021, but that $4.7 billion deal fell through. The planned IPO was the subject of a recent Axios report, which notes that there hasn’t been a major American FinTech IPO since 2021, a year that saw 41 companies raise $22.3 billion. The Axios report notes that Apex could end up being a bellwether for IPOs following a year that saw a number of lukewarm public debuts. “We were going to come out as part of the SPAC at $4.7 billion pre-money. That’s pretty frothy,” Apex CEO Bill Capuzzi told Axios earlier this year. Read More (PYMNTS)

How SoftBank’s bet on the U.S. mortgage lender Better backfired. In April 2021, SoftBank was so eager to back the U.S. mortgage lender Better Home & Finance that it wrote a $500 million cheque and was prepared to hand its newly acquired voting rights to Vishal Garg, the start-up’s founder and chief executive. The investment followed months of talks between Better and SoftBank’s Vision Fund, led by Rajeev Misra, a top lieutenant of the Japanese group’s founder and chief executive Masayoshi Son. At the suggestion of SoftBank executives, Better soon after cut a deal to go public via a special purpose acquisition company, choosing one set up by Icelandic billionaire Thor Björgólfsson. As part of the transaction, which valued Better at $7 billion, SoftBank said it would invest a further $1.3 billion. Read More (Financial Times)

Chamath Palihapitiya says venture capitalists also face disruption from AI – and startup founders stand to benefit. Artificial intelligence has been inescapable this year. After OpenAI released ChatGPT some 13 months ago, attention turned to how such tools will disrupt careers and industries – and eager venture capitalists poured billions into AI startups that might do the disrupting. But VCs themselves could get disrupted, according to billionaire investor Chamath Palihapitiya, a former Facebook executive and the CEO of VC firm Social Capital. “We talk about AI as a big disruptor to the big companies and this and that, but AI may be the biggest disruptor to VC in the end,” Palihapitiya said on the All-In Podcast. A “world where AI proliferates,” he said, is “positive for founders,” who will be able to own more of their companies rather than give away too much equity to VCs. Read More (Fortune)

ThinkMarkets IPO scrapped as SPAC merger falls through. Canada-listed blank check company, FG Acquisition Corp., and Melbourne-based broker ThinkMarkets have jointly decided to call off their previously announced merger plan. Following this mutual termination, FG Corp said it is actively exploring other potential opportunities to complete potential acquisitions. According to the timeline set by the its shareholders during a special meeting held in June, the company has until July 5, 2024, to finalize such a transaction. “We wish ThinkMarkets well in their future endeavors. With our robust merchant banking activities in both Canada and the United States, we look forward to pursuing a new target for the Corporation in the days and weeks ahead,” stated Kyle Cerminara, Chair of the Corporation’s board, and Larry Swets, Chief Executive Officer. Read More (Finance Feeds)

Singapore’s first Despac merger gets nod from shareholders. Singapore’s first special purpose acquisition company (SPAC) Vertex Technology Acquisition Corp (VTAC) has received shareholders’ approval for the business combination with pure-play live-streaming platform 17LIVE. A resounding 95.53% of the spac’s shareholders voted for the proposed merger. Upon completion of the business combination, VTAC will be renamed 17LIVE Group, trading under the new name from Dec 8 onwards. Trading of VTAC’s shares will be resumed on Dec 4. Read More (The Edge)

Singapore SPAC Pegasus Asia gives up on finding merger, acquisition target. Pegasus Asia PEGA.SI, a Singapore-based special purpose acquisition company (SPAC) backed by alternative asset manager Tikehau Capital TKOO.PA, it would not make an acquisition by a Jan. 20 deadline and would close down. The shell company, which was listed on the Singapore bourse in January 2022, had two years to acquire or merge with another business but said its board of directors had ruled against a deal "after considering macroeconomic and market conditions". It said it will make an announcement in due course on its next steps, which would involve the redemption of its issued outstanding shares, and then proceed to cease operations and wind up its business. There will be no redemption rights nor liquidating distributions regarding its warrants, Pegasus said. Read More (Nasdaq)

Volato, Inc. (SOAR) and PROOF Acquisition Corp. I complete business combination. Volato, Inc., a leading private aviation company in the United States, and PROOF Acquisition Corp I (NYSE: PACI) completed its business combination. The combined company will now operate under the Volato brand, and its common stock and warrants started trading on December 4, 2023 on the New York Stock Exchange American under the new ticker symbols “SOAR” and “SOAR.WS.” The Business Combination was approved at a Special Meeting of PACI shareholders held on November 28, 2023. Concurrent with the closing of the Business Combination, PACI also announced the closing of an additional $12 million of private investments, which, along with the $14 million in Series A Preferred Equity financing completed since July 2023, were converted to common stock at the time of the closing of the Business Combination. Including these transactions and the conversion of Volato convertible debt, the total capital raised exceeds $60 million. Read More (Business Wire)

African Agriculture, Inc. (AAGR) and 10X Capital Venture Acquisition Corp. II complete business combination. 10X Capital Venture Acquisition Corp. II (NASDAQ: VCXA), a publicly traded special purpose acquisition company, has completed its merger with African Agriculture, Inc., a global food security company operating a commercial-scale alfalfa farm on the African continent. The transaction was approved by 10X II’s shareholders at an extraordinary general meeting held on December 5, 2023. In connection with the closing, 10X II changed its name to “African Agriculture Holdings Inc.” (“African Agriculture”). Commencing December 7, 2023, African Agriculture’s common stock and warrants are expected to begin trading on the Nasdaq Global Market under the ticker symbols “AAGR” and “AAGRW”. Read More (Globe Newswire)

SRIVARU Holding Limited (SVH) and Mobiv Acquisition Corp. complete business combination. Mobiv Acquisition Corp. consummated business combination with SRIVARU Holding Limited, a Cayman Islands exempted company, and Pegasus Merger Sub Inc., a Delaware corporation and wholly owned subsidiary of the SVH, pursuant to the business combination agreement which was initially entered into on March 13, 2023, among the Company, SVH and Merger Sub, as amended by the first amendment to agreement and plan of merger, dated August 4, 2023. Pursuant to the Merger Agreement, several transactions will occur, and in connection therewith, SVH will be the parent company of the Company. In connection with the closing, stockholders of the Company will receive 3.572479901 shares of the Company’s Class A common stock, as incentive shares pursuant to the Business Combination Agreement. Accordingly, in connection with the consummation of the Business Combination, upon exchange of the Company’s Class A common stock, stockholders will receive an aggregate of 4.572479901 ordinary shares of SVH. No fractional securities will be issued. Read More (Globe Newswire)

ECD Automotive Design Inc. (ECDA) and EF Hutton Acquisition Corp. I complete business combination. ECD Automotive Design Inc., the industry leader in delivering restored, modified and electrified Land Rover Defenders, Jaguars, and other classic and collectible automobiles, closed its business combination between Humble Imports, Inc. d/b/a ECD Auto Design and EF Hutton Acquisition Corporation I (NASDAQ: EFHT), a special purpose acquisition company formed by affiliates of EF Hutton. The common shares of the combined company, which will operate as ECD Automotive Design Inc., started trading on the Nasdaq Global Market under the ticker symbol “ECDA” on Wednesday, December 13, 2023. Founded in 2013 by three British gear heads, ECD has become the leader in the restoration, modification and electrification of classic automobiles. E.C.D specializes in “restomods” (restoration and modification) and is dedicated to fully restoring classic autos from the ground up, returning the nostalgic experience to the road and ensuring their timelessness with modification touches, performance, and quality upgrades. Read More (E.C.D. Automotive Design)

Vast Renewables Limited (VSTE) and Vast and Nabors Energy Transition Corp. complete business combination. Vast Renewables Limited, a renewable energy company specializing in concentrated solar thermal power (“CSP”) energy systems that generate zero-carbon, utility-scale electricity and industrial process heat, completed its business combination with Nabors Energy Transition Corp. (NETC), an affiliate of Nabors Industries Ltd. (NYSE: NBR). In connection with the closing of the Business Combination, NETC merged with and into a wholly owned subsidiary of Vast, and NETC’s shares of Class A common stock, warrants to purchase shares of Class A common stock and units consisting of one share of Class A common stock and one-half of one redeemable warrant will cease trading on and be delisted from the New York Stock Exchange as of market open on Tuesday, December 19, 2023. Also on December 19, 2023, Vast’s ordinary shares are expected to begin trading on Nasdaq under the ticker symbol “VSTE” and its public warrants to purchase ordinary shares are also expected to begin trading on Nasdaq under the ticker symbol “VSTEW”. Read More (Business Wire)

Infrared Cameras Holdings, Inc. (MSAI) and SportsMap Tech Acquisition Corp. complete business combination. Infrared Cameras Holdings, Inc., a privately-held transformational solutions provider of a suite of thermal imaging and sensing platforms, paired with edge and cloud software, closed its business combination with SportsMap Tech Acquisition Corp. (NASDAQ: SMAP), a publicly-traded special purpose acquisition company. The business combination was approved by SMAP's stockholders at a special meeting of stockholders held on December 8, 2023. In connection with the consummation of the business combination, the combined company was renamed "Infrared Cameras Holdings, Inc." Infrared Cameras has developed a patented single pane-of-glass view that allows customers to monitor and analyze live imaging and sensing data for all of their critical operating assets in one place. Read More (Infrared Cameras Holdings, Inc.)

Airship AI Holdings, Inc. (AISP) and BYTE Acquisition Corp. complete business combination. Airship AI Holdings, Inc., a robust AI-driven video, sensor and data management surveillance platform that provides complex automated monitoring, predictive event analysis and intelligence to large institutions operating in dynamic and mission-critical environments with rapidly increasing volumes of data and data sources, and BYTE Acquisition Corp. (NASDAQ: BYTS), a special purpose acquisition company (BYTE), have completed the previously announced business combination. BYTE’s shareholders approved the Business Combination at an extraordinary general meeting held on December 19, 2023. In connection with the Business Combination closing, the combined company has been renamed “Airship AI Holdings, Inc.”. Beginning at the open of trading on December 22, 2023, the Company’s common stock and warrants will trade on Nasdaq under the ticker symbols “AISP” and “AISPW,” respectively. Read More (Business Wire)

Mobix Labs, Inc. (MOBX) and Chavant Capital Acquisition Corp. complete business combination. Mobix Labs, Inc., a fabless semiconductor company developing disruptive next-generation connectivity technologies for 5G infrastructure, satellite communications and defense industries, completed its business combination with Chavant Capital Acquisition Corp. (Nasdaq: CLAY), resulting in Mobix Labs becoming a publicly traded company. The business combination and all other proposals presented were approved at an extraordinary general meeting of Chavant shareholders held on December 18, 2023. In connection with the completion of the business combination, Chavant was renamed Mobix Labs, Inc. and its common stock and warrants started trading on the Nasdaq Stock Market under the ticker symbols “MOBX” and “MOBXW,” respectively, on December 22, 2023. Mobix Labs’ current management team will continue to lead the Company. Read More (Globe Newswire)

Global Hydrogen Energy LLC (HGAS) and Dune Acquisition Corp. complete business combination. Global Hydrogen Energy LLC, which seeks to be a leader in the sustainable energy transition as a next-generation industrial gas supplier, and Dune Acquisition Corporation (Nasdaq: DUNE), a special purpose acquisition company, completed its business combination. The combined company is named Global Gas Corporation and its Class A common shares and warrants are expected to commence trading on the Nasdaq Capital Market under the new ticker symbols “HGAS” and “HGASW,” respectively, on or about December 22, 2023. Headquartered in New York, Global Gas is led by Founder and Chief Executive Officer William B. Nance, who has over a decade of hydrogen and industrial gas experience. Read More (Globe Newswire)

LeddarTech (LDTC) and Prospector Capital Corp. complete business combination. LeddarTech®, an automotive software company that provides patented disruptive AI-based low-level sensor fusion and perception software technology for advanced driver assistance systems (ADAS) and autonomous driving (AD), is pleased to announce the completion of its business combination, previously announced on June 13, 2023 with Prospector Capital Corp. (formerly Nasdaq: PRSR, PRSRU, PRSRW) today. Commencing at the opening of trading on December 22, 2023, LeddarTech common shares and warrants to purchase common shares listed on the Nasdaq Global Market under the ticker symbols “LDTC” and “LDTCW,” respectively. As an automotive pure software company, LeddarTech offers a very crucial piece of the software stack for ADAS and AD. LeddarTech’s technology provides vehicles with better environmental understanding models, i.e., a substantially enhanced real-time 3D view of the vehicle’s surroundings, which is at the core of making a vehicle intelligent. Read More (LeddarTech)

Nukkleus Inc. (NUKK) and Brilliant Acquisition Corp. complete business combination. Nukkleus Inc. (Nasdaq: NUKK) closed its strategic merger with Brilliant Acquisition Corporation. This merger, valuing Nukkleus at around $105 million, signifies a bold step into a future rich with digital asset opportunities for businesses and investors alike. The combined company has been domesticated to Delaware and its name has been change to Nukkleus Inc. The common stock and warrants of the combined company started trading on the Nasdaq Stock Market under the ticker symbols NUKK and NUKKW on December 26, 2023. Nukkleus has undergone a strategic evolution through a SPAC merger with Brilliant Acquisition Corporation, in which Nukkleus has been acquired by Brilliant. Following this merger, the ticker symbol BRLI will be transitioned to NUKK to maintain brand continuity and market presence. This development aligns with our overarching vision for expansive growth and underscores our commitment to customer-centric innovation and service excellence. Read More (PR Newswire)

Alternus Energy Group Plc (ALCE) and Clean Earth Acquisitions Corp. complete business combination. Transatlantic clean energy independent power producer (IPP) Alternus Energy Group Plc (OSE: ALT) completed its business combination with Clean Earth Acquisitions Corp. (NASDAQ: CLIN), a special purpose acquisition company. The business combination was approved by Clean Earth shareholders in a Special Meeting of Clean Earth shareholders on December 4, 2023. The newly combined company will operate under the name “Alternus Clean Energy Inc.” Under the terms of the amended business combination agreement, AEG owns approximately 80% of the Company with the remaining shares owned by Clean Earth sponsors and public shareholders. The Company has acquired a majority of AEG’s assets while AEG will continue to exist as a separate legal entity and will continue to trade on the Euronext Growth stock market in Oslo under the ticker (OSE: ALT). The assets acquired comprise 168 megawatts (MW) in operation, 98 MW under construction, over 300 MW in various stages of development and an acquisition pipeline of over 1 GW. Read More (Globe Newswire)

Zoomcar, Inc. (ZCAR) and Innovative International Acquisition Corp. complete business combination. Innovative International Acquisition Corporation (NASDAQ: IOAC), formerly a Cayman Island registered blank-check special purpose acquisition company, and Zoomcar, Inc., an emerging market focused peer2peer car sharing company, are pleased to announce the closing of their previously announced merger. Prior to Closing, IOAC transferred by way of continuation out of the Cayman Islands and into the State of Delaware, so as to become a Delaware corporation. The Combined Company resulting from the merger was, effective at Closing, renamed Zoomcar Holdings, Inc. and started trading on NASDAQ on December 29, 2023 under the ticker symbol “ZCAR” for its common stock and “ZCARW” for its publicly traded warrants. Read More (Globe Newswire)

GRIID Infrastructure Inc. (GRDI) and Adit EdTech Acquisition Corp. complete business combination. GRIID Infrastructure Inc., an American bitcoin mining company that leverages a low-cost, low-carbon energy mix to manage and operate vertically integrated bitcoin mining facilities, completed its business combination with Adit EdTech Acquisition Corp., a publicly traded special purpose acquisition company. Adit EdTech stockholders approved the business combination at a special meeting held on Nov. 30, 2023. Following the business combination, the surviving company was renamed GRIID Infrastructure Inc. Beginning on Tuesday, Jan. 2, 2024, GRIID’s common stock is expected to trade on Cboe Canada, the new business name of the NEO Exchange, under the ticker symbol “GRDI,” and GRIID is seeking to list its common stock and warrants on a U.S. exchange. Read More (Globe Newswire)

Pinstripes, Inc. (PNST)

and Banyan Acquisition Corp. complete business combination. Pinstripes,

Inc., a best-in-class experiential dining and entertainment brand combining

bistro, bowling, bocce and private event space, and Banyan Acquisition

Corporation (NYSE: BYN) have closed their business combination, which was

approved by Banyan’s stockholders at a meeting on December 27, 2023. Pursuant

to the business combination, Pinstripes has become a wholly-owned subsidiary of

Banyan, which has changed its name to Pinstripes Holdings, Inc. (together with

Pinstripes, Inc, “Pinstripes”). Pinstripes’ Class A common stock and warrants

will begin trading on NYSE under the ticker symbols “PNST” and “PNST WS,”

respectively, on January 2, 2024. Pinstripes’ Founder and Chief Executive

Officer, Dale Schwartz, and the rest of the current management team of

Pinstripes, will continue in their management roles. Read More (Business

Wire)

Vision Sensing acquisition scraps Newsight Imaging deal. Vision Sensing Acquisition in an 8-K announced the termination of its merger agreement with Newsight Imaging, an Israeli company that develops advanced CMOS image sensor chips for 3D machine vision and spectral analysis. The decision was mutual according to the filing and was based on “challenging global economic conditions.” The $380 million deal was announced in August 2022. The SPAC in October won shareholder approval for a deadline extension that would have given the parties until May 3, 2024 to complete the deal. Redemptions of 264,443 shares at that time further whittled away at the SPAC’s trust, which saw a loss of 65% ahead of the last extension vote in May. Read More (SEC)

Athena Technology II mutually terminates $300 million Air Water Ventures deal. Athena Technology Acquisition II in an 8-K said it has called off a deal with Air Water Ventures (AWV) by mutual agreement. No reason was given. The SPAC said it intends to identify another target business. Athena Technology II announced the $300 million deal in April. Headquartered in Abu Dhabi, AWV is a first mover in direct air-to-water technology, producing quality drinking water at a lower cost and environmental impact than bottled water. The SPAC raised $250 million in an IPO two years ago. Read More (SEC)

Jupiter Acquisition Corp. announces mutually agreed termination of business combination agreement with Filament Health Corp. Jupiter Acquisition Corporation (NASDAQ: JAQC) announced the mutually agreed termination of the previously announced business combination agreement with Filament Health Corp. The special meeting of stockholders of Jupiter scheduled to reconvene on Thursday, December 28, 2023, at 12:00 p.m. Eastern Time, at which stockholders of Jupiter were to be asked to vote to approve the Business Combination Agreement and the business combination contemplated thereby, among other related matters, has been cancelled. Jupiter will redeem all of the outstanding shares of its Class A common stock issued as part of the units sold in Jupiter’s initial public offering, effective as of the close of business on December 26, 2023, because Jupiter’s board of directors has determined that Jupiter will not be able to consummate an initial business combination within the time period set forth in Jupiter’s amended and restated certificate of incorporation, as amended. Read More (Globe Newswire)

The U.S. 'blank cheque' firm in talks to merge with South African gold mine. Rigel Resource Acquisition, a New York-listed blank-cheque company, is in talks to combine with a South African gold miner. The deal could value Blyvooruitzicht Gold Mining at as much as $425 million (R8 billion). The blank cheque company backed by Orion Resource Partners, a money manager with $8.5 billion of assets, hired Citigroup and Rand Merchant Bank to do a pre-sale and raise about $60 million early in 2024. Rigel previously said the company signed a non-binding letter of intent for a business combination with a company in the global metals sector without providing details of the target. Read More (News24)

Zeekr Intelligent Technology Holding Ltd. explores potential IPO in the U.S. Zeekr Intelligent Technology Holding Ltd., the luxury electric vehicle brand owned by Zhejiang Geely Holding Group Co., is considering a potential initial public offering (IPO) in the United States in February, according to sources. The company is evaluating the optimal timing for the stock sale, based on investor demand, with tentative plans to launch the IPO around the Lunar New Year, which begins on February 10. This strategic decision is based on the expectation of increased investor appetite during this period. Zeekr will become the third or fourth subsidiary of Geely to go public, following Lotus Technology Inc. and Polestar Automotive Holding. Lotus Technology intends to finalize its merger with a special purpose acquisition company (SPAC) and debut on the Nasdaq by the end of the year. This announcement follows Polestar’s successful SPAC deal in June 2022, approximately eight months after Volvo Car AB’s listing on the Stockholm Stock Exchange. Read More (Motorblog)

DoubleDragon eyes SPAC

deal for Hotel Hospitality Platform in 2024. DoubleDragon Corp. aims

to finalize a business combination agreement with a SPAC by the first half of

next year and list on the Nasdaq. “We confirm that DoubleDragon Corporation,

through its Singapore-registered subsidiary Hotel101 Global Pte. Ltd., is considering

the SPAC route as one of its options to accelerate the expansion of Hotel101

globally as we have duly disclosed last August 8, 2023. As for the latest

progress related to this, we expect and aim to sign the business combination

agreement with a SPAC company by the first half of 2024, instead of the

initially planned NASDAQ IPO in 2026,” the company said in response to the

Philippine Stock Exchange’s request for clarification of a report by

Bilyonaryo.com. Read More

(Bilyonaryo.com)

|

Chart 3: SPAC Events – January 2024 |

|

S. No |

Event Name |

Date |

Time |

|

1 |

AITR Unit Split |

1/2/2024 |

- |

|

2 |

ANSC Unit Split |

1/2/2024 |

- |

|

3 |

MBTC Deadline extension vote |

1/2/2024 |

9AM EST |

|

4 |

IMAQ Deadline extension vote |

1/2/2024 |

9:30AM EST |

|

5 |

DMYY Deadline extension vote |

1/2/2024 |

11AM EST |

|

6 |

PTHR & Horizon Aircraft Merger Vote |

1/4/2024 |

1PM EST |

|

7 |

PMGM Deadline extension vote |

1/4/2024 |

12PM EST |

|

8 |

BRAC Deadline extension vote |

1/8/2024 |

10AM EST |

|

9 |

ISRL Deadline extension vote |

1/8/2024 |

12PM EST |

|

10 |

DECA & Longevity Biomedical Merger Vote |

1/9/2024 |

9AM EST |

|

11 |

OCAX Deadline extension vote |

1/9/2024 |

9:30AM EST |

|

12 |

GHIX Deadline extension vote |

1/9/2024 |

10AM EST |

|

13 |

WAVS Deadline extension vote |

1/9/2024 |

10AM EST |

|

14 |

GPAC Deadline extension vote |

1/9/2024 |

12PM EST |

|

15 |

ALSA Deadline extension vote |

1/10/2024 |

10AM EST |

|

16 |

SVII Deadline extension vote |

1/10/2024 |

10AM EST |

|

17 |

HCVI Deadline extension vote |

1/10/2024 |

3PM EST |

|

18 |

TCOA Deadline extension vote |

1/12/2024 |

10AM EST |

|

19 |

EMLD Deadline extension vote |

1/16/2024 |

11AM EST |

|

20 |

CLOE Deadline extension vote |

1/17/2024 |

9AM EST |

|

21 |

HCMA Deadline extension vote |

1/18/2024 |

10AM EST |

|

22 |

DMAQ & TruGolf Merger Vote |

1/19/2024 |

10AM EST |

|

23 |

KYCH Deadline extension vote |

1/19/2024 |

9:30AM EST |

|

24 |

OTEC & Regentis Biomaterials Merger Vote |

1/22/2024 |

10:30AM EST |

|

25 |

SZZL & Critical Metals Merger Vote |

1/23/2024 |

10AM EST |

|

26 |

SEPA & SANUWAVE Health Merger Vote |

1/29/2024 |

10AM EST |

|

27 |

MBTC & Cognos Therapeutics Merger Vote |

1/30/2024 |

9AM EST |

|

28 |

CETU Deadline extension vote |

1/31/2024 |

10AM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

|

Chart 4: SPAC Activity by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 5: Current Status of the SPAC Universe |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 6: Current Status of SPAC Universe by Trust Size |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 7: SPAC Transactions by Year |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 8: Average SPAC IPO Size ($ Mn) |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 9: SPAC Transactions by Month (LTM) |

|

|

Source: Intro-act, Boardroom Alpha

|

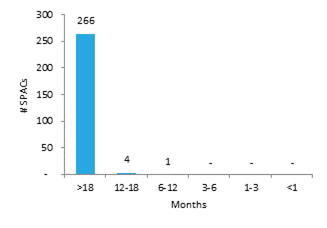

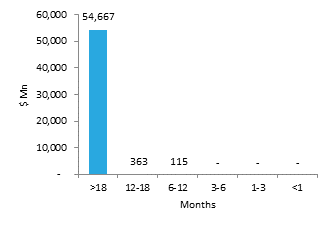

Chart 10: Time to Liquidation – By Volume |

|

Chart 11: Time to Liquidation – By Trust Value |

|

|

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 12: Active SPACs By Sector (As of Month Ending December 2023) |

|

|

Source: Intro-act, Boardroom Alpha

|

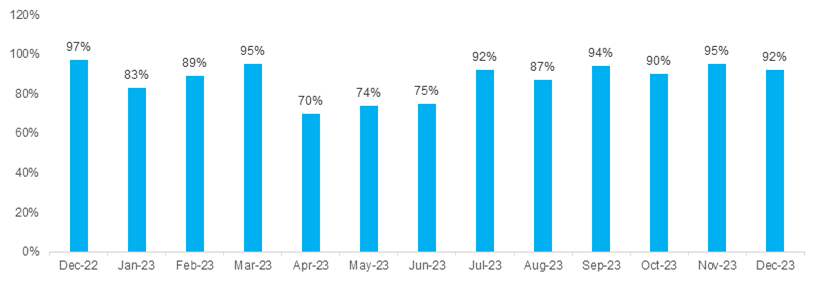

Chart 13: Average Redemption Rate by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 14: SPAC Redemption Detail – December 2023 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

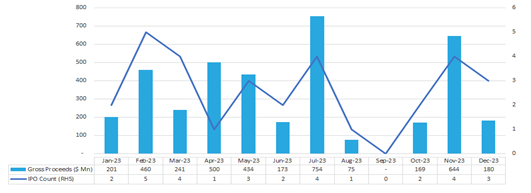

Chart 15: Monthly SPAC Activity – December 2023 |

|

|

Source: Intro-act, Boardroom Alpha. Searching figures ($Mn and Count) are as of month end.

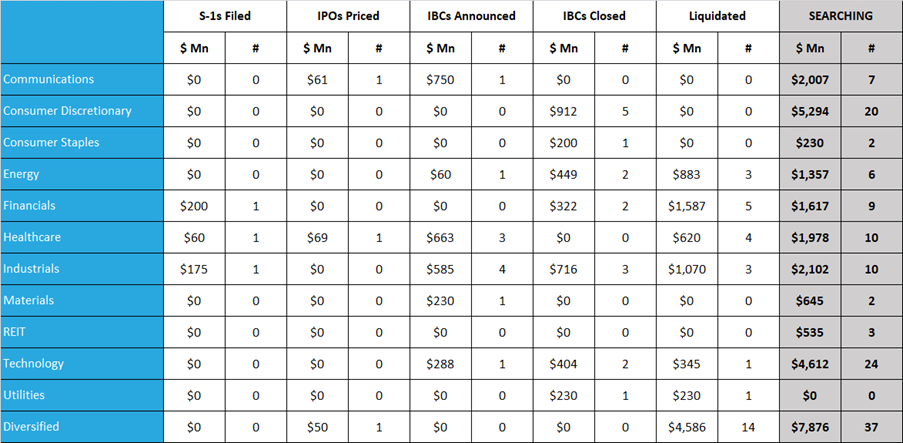

|

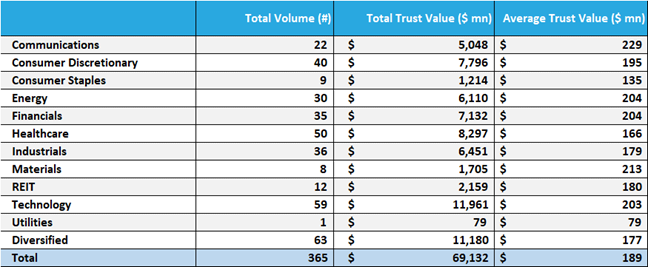

Chart 16: SPAC IBC Announcements by Target Sector – December 2023 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

The SPAC and New Issue ETF (SPCX). SPCX gives investors exposure to a broad portfolio of SPACs with the familiar attributes of an exchange traded fund’s diversity, tax efficiency and liquidity. SPCX is the first actively managed SPAC ETF. Why active? As the SPAC market is rapidly evolving, we believe that the portfolio management approach should equally reflect the dynamic nature of this burgeoning capital-raising alternative. This is no place for a rigid rules-based index strategy.

|

Chart 17: SPCX Summary Data |

|

Chart 18: SPCX Top 10 Holdings |

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

Source: Intro-act, ETF.com. Data as of 12/31/23.

|

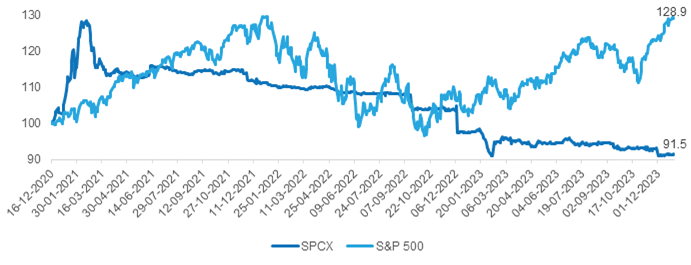

Chart 19: SPCX Performance |

|

|

Source: Intro-act, Yahoo! Finance. Data as of 12/31/23.

|

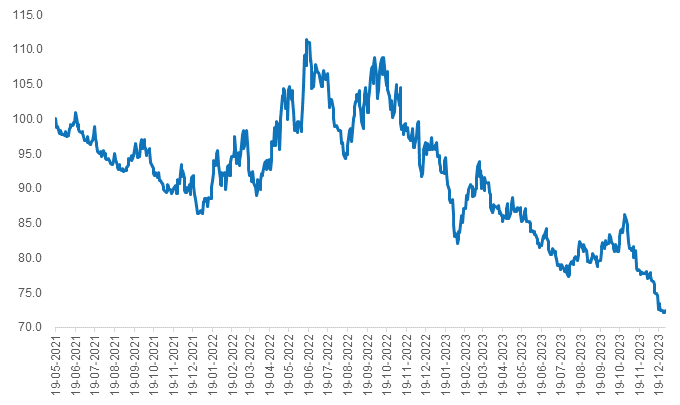

Chart 20: Relative-SPAC Index vs Russell 3000 |

|

|

Source: Intro-act, FactSet

|

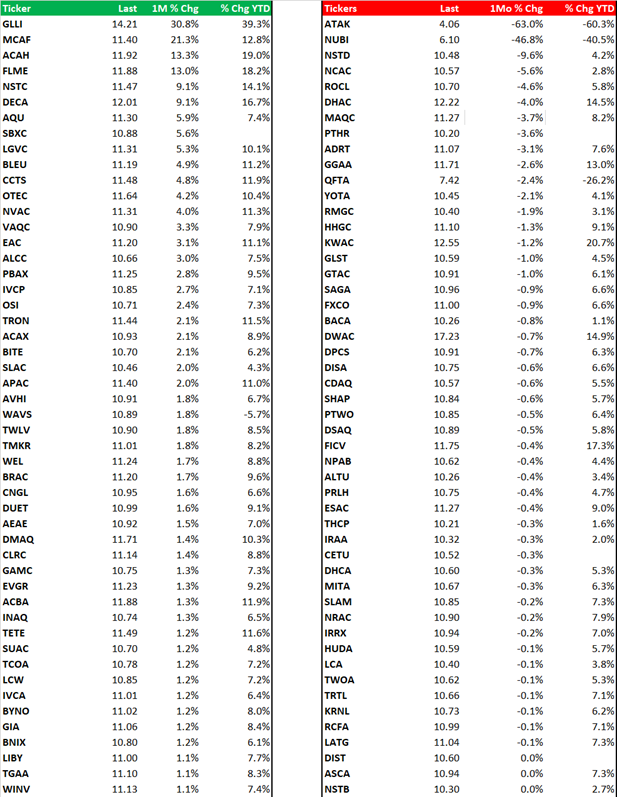

Chart 21: Gainers and Losers in the Broader SPAC Universe (% Change) |

|

|

Source: Intro-act, FactSet

|

Chart 22: SPAC IPO Pricings by Sector – December 2023 |

||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 23: SPAC S-1 Filings by Sector – December 2023 |

||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 24: SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 25: DE-SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 26: SPAC Underwriter League (YTD As of December 2023 End) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Bookrunner Volume ($ Mn) is based on the total amount of the offering sold, including over-allotment. Full credit is awarded to the sole book-runner or split equally among joint book-runners.

|

Chart 27: Top De-SPAC Advisors (YTD As of December 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Advisor credit is shared equally among all advisors on a given deal, as a proportion of the enterprise value of the target company acquired by the SPAC. Firms with multiple advisory roles receive credit for each role.

|

Chart 28: SPAC Legal League (YTD As of December 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Volume ($ Mn) is awarded to both Issuer and Underwriter Counsel.

|

Chart 29: SPAC Auditor League (YTD As of December 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research

|

Chart 30: ICR – The Leading SPAC Communications and Capital Markets Advisor |

|

113 Transactions / $267 Billion in Transaction Value Since 2021

|

Source: Intro-act, ICR. Announced SPAC transactions since 2021, All Announcements not shown. Data as of April 2022.

Analyst Certification

I, Peter Wright, certify that the views expressed in the research report accurately reflect my personal views about the subject securities or issues. I also do not receive direct or indirect compensation based on my recommendations or views.

Intro-act, Inc. (Intro-act) issued this report and may seek fees for the assistance with investor targeting, access, and further investor preparation services. Intro-act, Inc. will not seek renumeration for any investment banking service or investment advice.

Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources who are believed to be reliable. However, the issuer and related parties, as well as Intro-act, do not guarantee the accuracy or completeness of this report, and have not sought for this information to be independently verified. Opinions contained in this report represent those of the Intro-act analysts at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, and estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties, and other factors that may cause the actual results, performance, or achievements of their subject matter to be materially different from current expectations.

Exclusion of Liability: To the fullest extent allowed by law, Intro-act, Inc. shall not be liable for any direct, indirect, or consequential losses, loss of profits, damages, or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this note.

No personalized advice: The information that we provide should not be construed in any manner whatsoever as personalized advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Intro-act’s solicitation to affect, or attempt to affect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors.

Investment in securities mentioned: Intro-act has a restrictive policy relating to personal dealing and conflicts of interest. Intro-act, Inc. does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees, and contractors of Intro-act may have a position in any or related securities mentioned in this report, subject to Intro-act’s policies on personal dealing and conflicts of interest.

Copyright: Copyright 2024 Intro-act, Inc. (Intro-act).

Intro-act is not registered as an investment adviser with the Securities and Exchange Commission. Intro-act relies upon the “publishers’ exclusion” from the definition of investment adviser under Section 202(a) (11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Intro-act does not offer or provide personal advice, and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell, or hold that or any security, or that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.