DEAL IN FOCUS: BARÇA MEDIA – MOUNTAIN & CO. I ACQUISITION CORP. (MCAA)

|

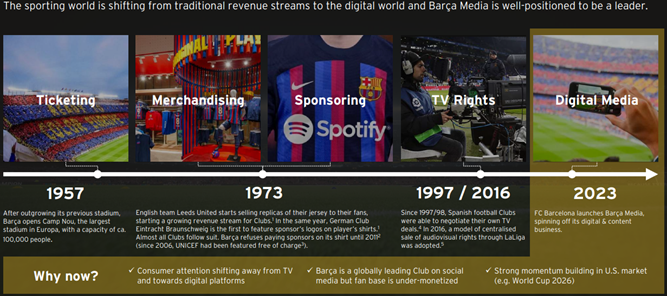

Chart 1: Barça Media is the Final Frontier in the Monetization of Sports |

|

|

Source: Intro-act, Mountain & Co. I Acquisition Corp./Company Investor Presentation

Barça Media holds a

strategic advantage and potential leadership role in digital media monetization

which allows the company to meet its core objective of creating captivating

content that fuels FC Barcelona's diverse distribution channels. Leveraging

FC Barcelona's solid global brand and favorable market trends, Barça Media

focuses on crafting unique digital content that fosters fan engagement and

facilitates sustainable, profitable expansion. This involves generating dynamic

content for the club's distribution channels and promoting it across FC

Barcelona's social media channels, generating almost 2.5 billion interactions

in the 2021/2022 season. Barça Media collaborates with top-tier content

platforms such as Disney+, DirecTV, Sony Pictures, Univision, DAZN, and more by

licensing and partnering. Every year, Barça Media creates numerous original

content pieces to enhance FC Barcelona's brand visibility. It aims to establish

itself as a global digital media and entertainment leader within a vast

worldwide market. The rise of digital assets marks a natural progression from

traditional collectables, holding historical value in sports. This evolution

presents an opportunity to enhance fan engagement by merging digital assets

with utilities like exclusive experiences, ownership, and artwork. This vision

births the "Barçaverse" – a digital community that binds fans

worldwide, nurturing a robust collective spirit.

|

Chart 2: Barça Media Centralizes the Creation, Production, and Commercialization of FC Barcelona’s Audiovisual, Digital, and eSports Output |

|

|

Source: Intro-act, Mountain & Co. I Acquisition Corp./Company Investor Presentation

Barça Media is a high-growth business with audiovisual and digital divisions that produce dynamic content to engage, reward, and build connections with the Club’s global fanbase. It adopts a highly scalable business model by concentrating on three distinct and lucrative segments. The first, Barça Studios, operates with subscription revenue and content licensing fees as primary revenue sources. Second, Barça Vision capitalizes on sales from NFTs, licensing fees, and capital gains through media ventures. And third, Barça eSports generates revenue through contracts like sponsorships and event-based income from prizes and merchandise. These business segments demonstrate swift scalability, with a clear route to profitability in the near term. The digital content enterprise is notably cash flow-positive and is anticipated to achieve profitability right from the first fiscal year.

|

Chart 3: Highly Scalable Business Model |

|

|

Source: Intro-act, Mountain & Co. I Acquisition Corp./Company Investor Presentation

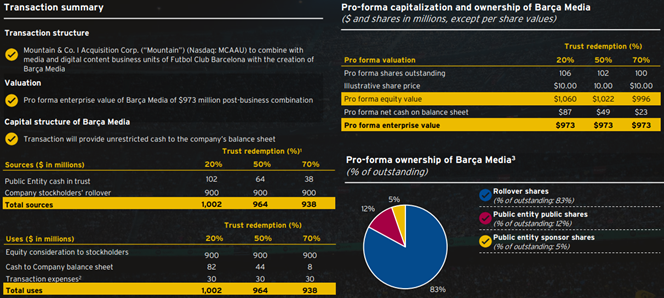

In August 2023, FC Barcelona announced a business combination with Mountain & Co. I Acquisition Corp. (Nasdaq: MCAA) to take Barça Media public in a deal that values Barça Media at ~$1 billion.

n The combination with Mountain & Co. I Acquisition Corp. will give Barça Media access to the U.S. capital markets to create an even stronger platform to accelerate its multi-pronged growth strategy and is a major strategic transaction for FC Barcelona, reinforcing the digital transformation of the Club, which was initiated by the onboarding of strategic partners in 2022. It is worth noting that FC Barcelona expects Barça Media to serve as an important source of revenue in the coming years and has assigned significant resources to support the business. Upon closing of the transaction, Barça Media will continue to be managed by a highly experienced team of sports, media and entertainment professionals headed by experienced Spanish media executive Toni Cruz as Chief Executive Officer.

n The transaction values the pro-forma company at an estimated enterprise value of approximately $973 million and will provide unrestricted cash on Barça Media’s balance sheet, depending on redemption levels. Assuming no redemptions and no further capital raised, it is expected that the closing of the transaction will result in around 83% of the outstanding shares being owned by Barça Media’s existing shareholders, including FC Barcelona, Blaugrana Invest, S.à.r.l., and Libero Football Finance AG. FC Barcelona is expected to own a majority of the combined company, contingent on redemption and warrant levels.

n Upon the closing of the transaction, the combined company will be named Barça Media. It is expected to be listed on Nasdaq under the ticker symbol BRME and close in 4Q23.

|

Chart 4: Transaction Summary |

|

|

Source: Intro-act, Mountain & Co. I Acquisition Corp./Company Investor Presentation

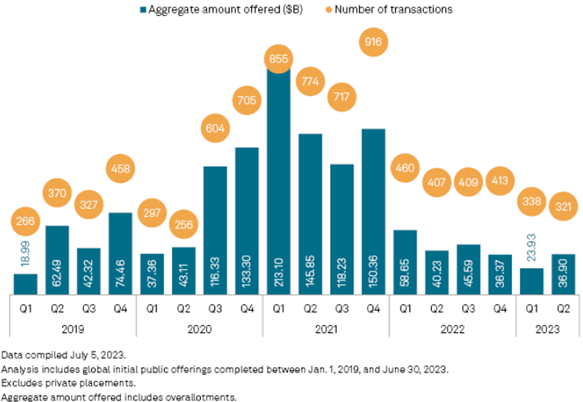

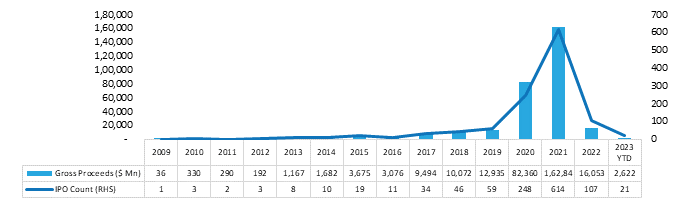

Global IPOs in Q2 2023 hit lowest level since 2020 as interest rates soar. The pace of initial public offerings hit a new low in the second quarter as central banks around the world tightened monetary policies, pushing costs to unattractive levels for potential investors. There were 321 IPOs launched globally in the second quarter, down from 338 in the prior three months and the worst quarter for IPOs since the second quarter of 2020, according to the latest data from S&P Global Market Intelligence. The cumulative worth of the securities sold in those IPOs was $36.90 billion, up from $23.93 billion in the first quarter. The $60.83 billion offered in the first half of the year was down 38.5% from the amount offered in the first two quarters of 2022 and down 83.1% from the first two quarters of 2021, when IPO activity peaked. Read More (S&P Global Market Intelligence)

|

Chart 5: Global IPO activity since 2019 |

|

|

Source: Intro-act, S&P Global Market Intelligence

The modern De-SPAC and a way forward. Many of the SPACs that went public in 2021 and 2022 are now nearing the end of their hunting period to identify and complete an IBC prior to the time that they are required to wind-down the SPAC and return the IPO proceeds to investors. Around 300 SPACs have deadlines to merge with an operating company by the end of 2023, making this small window of time opportunistic for de-SPAC transactions. Additionally, the economics of the SPAC structure, which provides significant incentives to SPAC sponsors to consummate an IBC, result in the SPAC sponsors being highly incentivized to negotiate terms of an IBC that are favorable to the target. While the volume of SPAC’s has and may continue to decline, there are still opportunities for highly motivated SPAC’s and strong target companies looking to come to market. Despite its decline in volume, SPACs have been around for decades and provide an important function in capital markets, providing an alternative form of venture capital financing that still have advantages over traditional IPOs to bring private companies public. Read More (JD Supra)

Top 10 practice tips: PIPE transactions by SPACs. Law firm Mayer Brown discusses 10 practice points that can SPAC counsel to execute a PIPE transaction alongside a business combination deal. Redemption options inherently create uncertainty as to the amount of cash available to the combined company following the initial business combination. SPACs often seek to mitigate the redemption concern by issuing new securities to institutional accredited investors in a PIPE transaction that is contingent upon the closing of the deal. As the SPAC market has cooled, PIPE transactions have also encountered difficulties. A changing landscape for SPACs calls for an extra measure of flexibility and a willingness to consider alternatives in connection with structuring the accompanying SPAC PIPE transaction. Read More (Mondaq)

Unraveling SPAC stock redemption taxes. SPACs face many tax challenges. A current issue is whether a SPAC’s redemption of shareholder stock is subject to the new 1% excise tax. The short answer is yes, but there are exceptions, according to the Alston & Bird law firm. Under Section 4501(a), a “covered corporation” (any U.S. corporation whose shares are publicly traded) must pay a tax equal to 1% of the fair market value of any stock of the corporation that is repurchased by the corporation during the taxable year. Section 4501(c)(3) provides that the amount taken into account under Section 4501(a) is reduced by the fair market value of any stock issued by the covered corporation during the taxable year, including the fair market value of any stock issued or provided to employees of the corporation or employees of a specified affiliate of the corporation during the taxable year. This is known as the “netting rule.” Read More (JD Supra)

Ask an advisor: Are SPACs ever a good investment? In the first years of the COVID pandemic, investment in SPACs skyrocketed. In 2019, there were only 59 SPAC IPOs, according to the website SPAC Insider. Then, in 2020, there were 248, and in 2021 there were a record-breaking 613, raising a total of $265 million. Soon afterward, the SPAC boom began to bust. A number of high-profile acquisitions failed to pan out. So, are SPACs a bad investment? Good for the sponsor, not the investor. The incentives of the SPAC sponsors are among the most important pieces when evaluating a SPAC and likely explain a lot of the optimism around SPACs in 2020-2021. SPAC sponsors receive a disproportionate amount of equity in the SPAC if they are able to close a deal. Generally, a SPAC sponsor contributes about 2% of the capital and receives about 20% of the SPAC (and usually some free or discounted options, too). SPACs have a limited amount of time to close a deal, and if the deal does not close, the sponsor loses their 2%. Read More (Yahoo! Finance)

Universal Entertainment executives blamed for failed SPAC merger as lawsuit gets underway. Executives at Japan’s Universal Entertainment Corp. spent much of the past year coming up with creative ways to scuttle the $2.6 billion merger of their Okada Manila casino resort unit with a blank-check company, a former partner in the deal told a U.S. judge. Jason Ader founded 26 Capital Acquisition, which agreed to combine with the Okada resort to give it a Nasdaq stock listing. But Ader, whose firm sued to revive the failed deal, testified Monday that Universal started working to sabotage the Philippines casino transaction starting in 2022. Universal declared the merger dead on June 30. “We got zero cooperation” in closing the deal, Ader told Delaware Chancery Judge Travis Laster during the first day of trial testimony. Ader is a veteran gaming-industry analyst and on the board of the Las Vegas Sands Corp. He’s now chief executive officer of SpringOwl Asset Management LLC. Read More (Bloomberg)

Hyzon Motors, SPAC merger complaint may proceed, judge says. Leaders and backers of a blank-check company that merged with Hyzon Motors in 2021 must face an investor’s claims they overstated the hydrogen-fuel-cell vehicle maker’s customer base and financial health, a Delaware judge ruled. “At this stage, the plaintiff has stated a claim for breach of fiduciary duty based on materially misleading disclosures and omissions,” Vice Chancellor Paul Fioravanti Jr. of Delaware’s Chancery Court said, ruling from the bench. Bloomberg reports that news releases and presentations about Hyzon’s customers may have given investors the wrong impression about potential vehicle orders and about business relationships with blue-chip companies, he said. Decarbonization Plus Acquisition stockholders approved the business combination with Hyzon Motors two years ago this week. Hyzon is a global supplier of zero-emissions hydrogen fuel cell powered commercial vehicles. The pro forma implied enterprise value of the combined company was $2.1 billion at the time. Read More (Bloomberg Law)

Sunlight Financial investors sue Apollo Global over 2021 SPAC deal. Sunlight Financial Holdings investors sued Apollo Global Management and other architects of its blank-check merger, claiming shareholders were duped into participating in a disastrous deal that made millions for insiders. The lawsuit accuses the private equity giant of engineering a lopsided transaction that wiped out public stockholders while handing a windfall to its own affiliates and Sunlight’s senior leaders, Bloomberg reports. The deal took Sunlight public in July 2021 by combining it with Spartan Acquisition II, backed by Apollo. Sunlight is a U.S. residential solar-power financing platform. Read More (Bloomberg Law)

Sam Altman explains why he’s helping to take nuclear microreactor company Oklo public via SPAC. The advanced nuclear fission startup, Oklo, announced it will go public via merger with AltC Acquisition Corp., a special purpose acquisition company that was co-founded by OpenAI CEO Sam Altman, who is also the chairman of Oklo’s board. When the SPAC closes by early 2024, it will raise as much as $500 million for Oklo, which the company will use to scale up development of its supply chains and pilot manufacturing facilities. Altman best known for his work with artificial intelligence after Microsoft invested billions of dollars in OpenAI and the company’s ChatGPT chatbot caught the public’s imagination late last year. But Altman’s philosophical vision for a better future is dependent on two technologies developing in in parallel: AI and energy. Read More (CNBC)

Three firms lead Chinese med-device company’s SPAC Merger in the U.S. At least three law firms are advising in Chinese medical technology firm Baird Medical Investment Holdings Limited’s go-public merger with a special purpose acquisition company in a deal valuing the post-merger company at $370 million. Dechert LLP is advising Guangzhou, China-headquartered Baird Medical, while Shearman & Sterling is counseling the San Francisco-based SPAC, ExcelFin Acquisition Corp. ExcelFin’s sponsors include private equity firm Grand Fortune Capital, LLC, an affiliate of a Hong Kong investment firm, and Fin Venture Capital, a San Francisco-based private equity firm. Read More (Bloomberg Law)

ATFX expands its global reach with acquisition of Rakuten Securities Australia. ATFX, a global leading online trading CFDs broker, has announced its acquisition of Rakuten Securities Australia Pty Ltd ("RSA"), a subsidiary of Rakuten Securities, Inc., further strengthening its position in the Australian market and expanding its global footprint. This strategic move marks a significant milestone for ATFX as it continues to solidify its position as a global trusted online broker with innovative trading solutions. By acquiring RSA, ATFX gains access to a well-established customer base and a talented team of industry professionals. The acquisition of RSA aligns with ATFX's core mission of providing clients with a comprehensive suite of trading services, backed by advanced technology and superior customer support. The company remains committed to delivering a seamless trading experience, robust platforms, and a wide range of trading instruments, including forex, indices, commodities, and more. Read More (Yahoo! Finance)

Glencore and Stellantis back $1 billion SPAC deal for nickel and copper mines in Brazil. Global mining company Glencore, automaker Stellantis, and Volkswagen’s battery unit PowerCo are supporting a $1 billion acquisition by ACG Acquisition to purchase two Brazilian mines. ACG will acquire the Santa Rita nickel sulfide and Serrote copper mines from private equity funds with the help of Appian Capital. After the purchase, the nickel will be refined at Glencore’s facilities in Western Europe and North America and used in EV batteries by Stellantis, PowerCo, and other manufacturers. To finance the deal, Glencore, Stellantis, and La Mancha Resource Capital will each invest $100 million in ACG equity, while PowerCo will provide a $100 million nickel prepayment. Subsequently, ACG will rebrand as ACG Electric Metals and issue new shares, with Glencore, Stellantis, and La Mancha taking a 51% ownership, leaving the remaining 49% for free float, The Deep Dive reports. Read More (The Deep Dive)

VinFast’s SPAC partner for U.S. listing extends lifespan by 12 months. Shareholders of Black Spade Acquisition, which planned to merge with Vietnam’s electric automaker VinFast by this month to begin a U.S. listing, voted today to extend its deadline by a year. The vote gives the Hong Kong-based SPAC until July 20, 2024 to merge with a target company. Its shareholders have not yet voted on the merger with VinFast. At announcement in May, the deal had an equity value of over $23 billion. The SPAC has approximately $169 million of cash in trust, which will go to VinFast, less any redemptions. Following a July 2021 IPO, Black Spade was initially targeting the entertainment industry, with a focus on enabling technology, lifestyle brands, products, or services and entertainment media, primarily in Asia. Read More (Reuters)

Ex-CFO’s shocking $5 million crypto heist: The scandal that rocked the SPAC world! Securities and Exchange Commission announced that it has successfully obtained a judgment against Morgenthau. He was convicted of a scheme in which he stole more than $5 million dollars from his company and its investors. The SEC complaint filed in U.S. District Court, Southern District of New York alleged that Morgenthau used the funds of the company as his own piggy bank. He used the money for personal expenses, and traded in crypto assets and securities. Read More (AlphaBetaStock.com)

Trump-linked SPAC stock soars 30% after striking fraud charges deal. The stock of Digital World Acquisition Corp.—a special purpose acquisition company that had plans to merge with the company behind former President Donald Trump’s Truth Social— jumped more than 30% after details about its $18 million settlement with the Securities and Exchange Commission were released. In a release Thursday, the SEC said the company had misled investors by “failing to disclose” that it had a plan and was working to acquire Trump Media & Technology Group Corp., the parent company of Truth Social. The SEC said DWAC’s chief executive had been working on a plan to acquire Trump Media since February 2021, solicited investors ahead of an initial public opening, and failed to disclose his potential conflict of interest based on an agreement he had made with the Trump group. Read More (Forbes)

The biggest restaurant IPO news of H1 2023. When Cava said it was going public, analysts were surprised. Compressed margins and profitability struggles made restaurants a tough sell for investors at the start of the year. But Cava defied expectations, raising a $318 million IPO last month. Two weeks later, Gen Restaurant Group gained over $43 million in capital, higher than initially expected. More restaurants are expected to go public this year, too. Panera Brands revamped its executive suite to prepare for an IPO. Originally, it planned to go public through Danny Meyer’s special purpose acquisition company, but that deal fell through last year due to unfavorable market conditions. Panera Brands is now planning a traditional IPO. Pinstripes, however, is taking the SPAC route and plans to use its partnership with Banyan Acquisition Corp. to make its public debut. Read More (Restaurant Drive)

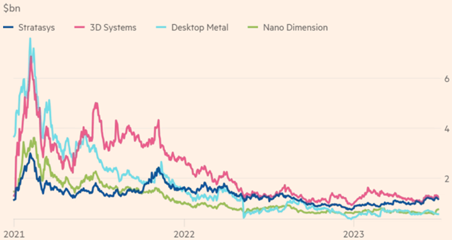

3D printing industry gripped by intrigue, litigation and churn. 3D printing promised to revolutionize production of everything from toys to biomedical implants through “additive manufacturing”. Now the hype has worn off and four leading manufacturers are in the middle of merger machinations that could slice them down to two or three. Stratasys, 3D Systems, Nano Dimension and Desktop Metal rode a wave of investor interest in 3D printing, in which machines controlled by software build up products layer by layer. Among those buying their shares was an exchange traded fund run by high-profile tech stock picker Cathie Wood’s Ark Investment Management – ticker symbol PRNT. But their valuations have plummeted since early 2021 as they confront stubborn barriers to using the technology for mass-produced goods. Losing money and struggling to raise cash, they are pursuing tie-ups. The dealmaking stands out for its corporate intrigue, however, with litigation involving companies and their shareholders now playing out in the courts. Read More (Financial Times)

|

Chart 6: Equity valuation among listed 3D printers have collapsed since peaking in 2021 |

|

|

Source: Intro-act, Financial Times

Asia-Pacific M&A deal value drops 37.5% in H1 2023. Asia-Pacific ex-Japan merger and acquisition (M&A) activities reached US$340.6 billion in the first half of 2023, a 37.5% drop in deal value from 2022, marking it as the lowest first-half period in a decade, according to Refinitiv’s Asia-Pacific Investment Banking Review, mainly due to declines in M&A activity in China, Australia and South Korea. However, in China, the easing of Covid restrictions is expected to lead to a recovery in the Chinese economy and a pick-up in second-half M&A activity. The Australia and South Korea M&A markets, notes PwC’s Global M&A Industry Trends report, have been negatively affected by broader macroeconomic challenges. Most of the deal making activity in the Asia-Pacific region occurred in the industrials sector, which accounted for a 21.1% market share worth $71.9 billion in H1 2023, according to the Refinitiv report, up 11.5% from the same period of 2022. Read More (The Asset)

London SPAC Financials Acquisition loses 87% of trust to redemptions ahead of extension vote. Financials Acquisition said shareholders backed its new business combination deadline at a general meeting. The SPAC focused on insurance technology now has until Dec. 31 to complete a deal. Financials Acquisition raised £150 million from an April 2022 IPO. However, Insurance Insider reports that £130 million of shareholder capital was redeemed ahead of the extension vote. While the SPAC has said a targeted has been identified, the company has not been named. The business combination involves raising additional capital and becoming a listed operating company, as well as deploying funds into the Lloyds of London insurance market for reinvestment purposes. Read More (Insurance Insider)

SPAC IPOs in

Switzerland. SPAC IPOs in Switzerland have been possible since the new

SIX rules on SPACs entered into force on 6 December 2021. The reason is

probably that the Swiss regulator (FINMA) was uncertain whether it had to qualify

SPACs as collective investment schemes – which they are clearly not. The

collective investment scheme act exempts Swiss corporations listed at a Swiss

stock exchange from the act. The only corporate purpose of a SPAC is the direct

or indirect acquisition of a target or, if occurring at the same time, several

targets or the merger with a target or several targets (article 89h(1) LR).

This De-SPAC needs to occur within three years from the first day of trading at

SIX (article 89h(1) LR). The target needs to be an operating company or a

holding company of an operating company. Pure real estate holding companies

would therefore not be a proper target. However, given that the track-record

requirement does not apply to real estate companies, a real-estate SPAC would

not be sensible in any event. Nothing in the rules prohibits a SPAC from

merging with an already listed company, although that was not necessarily the

intention of the new rules. Read More (Lexology)

Abacus Life, Inc. (ABL) and East Resources Acquisition Company complete business combination. East Resources Acquisition Company (NASDAQ: ERES) has completed its business combination with Abacus Life, a leading buyer of life insurance policies and a vertically integrated alternative asset manager specializing in specialty insurance products. In connection with the completion of the business combination, ERES has been renamed “Abacus Life, Inc.”, and its common stock and warrants started trading on the Nasdaq Capital Market on July 5, 2023, under the ticker symbols “ABL” and “ABLLW”, respectively. The company’s common stock and warrants started trading under the ticker symbols “ERES” and “ERESW,” respectively, on July 3, 2023. Read More (Business Wire)

Lifezone Metals Limited (LZM) and GoGreen Investments Corp. complete business combination. Lifezone Metals Limited (NYSE: LZM), a modern metals company creating value across the battery metals supply chain from resource to metals production and recycling, announced that on July 6, 2023, Lifezone Holdings Limited completed the business combination with GoGreen Investments Corp., formerly a blank check company listed on the New York Stock Exchange. Lifezone Metals' ordinary shares and warrants started trading on the NYSE under the ticker symbols "LZM" and "LZMW", respectively. The business combination was implemented through a newly created holding company, Lifezone Metals. Upon completion of the business combination, GoGreen merged into a wholly-owned subsidiary of Lifezone Metals, after which GoGreen ceased to exist and the shareholders of GoGreen received shares in Lifezone Metals, and LHL was acquired by Lifezone Metals, after which LHL became an operating wholly-owned subsidiary of Lifezone Metals and the shareholders of LHL received shares in Lifezone Metals. The completion of the business combination establishes the first pure-play nickel resource and cleaner technology company listed on the NYSE. Read More (PR Newswire)

Marti Technologies Inc. (MRT) and Galata Acquisition Corp. complete business combination. Galata Acquisition Corp. closed its business combination with Marti Technologies Inc. The combined company, Marti Technologies, Inc. (formerly known as Galata Acquisition Corp., Pubco), started trading of its Class A Ordinary Shares and warrants on the NYSE American Stock Exchange under the ticker symbols “MRT” and “MRTW”, respectively, on July 11, 2023. Founded in 2018, Marti is Türkiye’s leading mobility app, offering multiple transportation services to its riders. Marti has launched a ride hailing service that matches riders with drivers traveling in the same direction and operates a large fleet of e-mopeds, e-bikes, and e-scooters. All of Marti’s offerings are serviced by proprietary software systems and IoT infrastructure. Read More (Business Wire)

Carmell Therapeutics Corp. (CTCX) and Alpha Healthcare Acquisition Corp. III complete business combination. Alpha Healthcare Acquisition Corp. III (Nasdaq: ALPA), a special purpose acquisition company led by Mr. Rajiv Shukla, completed its business combination with Carmell Therapeutics Corporation, a Phase 2 stage regenerative medicine platform company developing allogeneic plasma-based biomaterials for active soft tissue repair, aesthetics and orthopedic indications. The resulting combined company, Carmell Therapeutics Corporation, started trading its shares of common stock and warrants on the Nasdaq Capital Market under the ticker symbols “CTCX” and “CTCXW,” respectively, on July 17, 2023. Mr. Shukla will serve as Executive Chairman and Mr. Randy Hubbell will serve as Chief Executive Officer of the combined company. Read More (Business Wire)

Complete Solaria (CSLR) and Freedom Acquisition I Corp. complete business combination. Complete Solaria, Inc., a leading solar technology, services, and installation company, has completed its business combination with Freedom Acquisition I Corp., effective July 18, 2023. The combined company will operate under the name Complete Solaria, Inc. Commencing July 18, 2023, Complete Solaria’s common stock and warrants started trading on The Nasdaq Stock Market under the symbols “CSLR” and “CSLRW”, respectively. The company will continue to be led by Will Anderson, Chief Executive Officer, and Brian Wuebbels, Chief Financial Officer, alongside the rest of the current Complete Solaria management team. Read More (Business Wire)

PSQ Holdings, Inc. (PSQH) and Colombier Acquisition Corp. complete business combination. PSQ Holdings, Inc., a leading marketplace of patriotic businesses and consumers, and Colombier Acquisition Corp. (NYSE: CLBR) (“Colombier”), completed its business combination. In connection with the closing of the business combination, a wholly-owned subsidiary of Colombier merged with and into PSQ Holdings, Inc., with PSQ Holdings, Inc. continuing as a wholly-owned subsidiary of Colombier, and was renamed “PublicSq. Inc.,” and Colombier was renamed “PSQ Holdings, Inc.” (“PublicSq.”). PublicSq.’s shares of Class A common stock and warrants started trading on the New York Stock Exchange (NYSE) under the symbols “PSQH” and “PSQH WS,” respectively, beginning July 20, 2023. The transaction provides PublicSq. with approximately $34.9 million, after giving effect to Colombier stockholder redemptions and before payment of transaction expenses. Read More (Business Wire)

AEON Biopharma, Inc. (AEON) and Priveterra Acquisition Corp. complete business combination. Priveterra Acquisition Corp. (Nasdaq: PMGM), completed its business combination with AEON Biopharma, Inc. (AEON), a Phase 3 stage-ready biopharmaceutical company developing a proprietary neurotoxin with initial focus on preventive treatments for episodic and chronic migraines along with other debilitating medical conditions. The resulting combined company changed its name to AEON Biopharma, Inc. and started trading its shares of common stock and warrants on NYSE American LLC under the ticker symbols AEON and AEON WS, respectively, on July 24, 2023. Read More (Business Wire)

Electriq Power, Inc. (ELIQ) and TLG Acquisition One Corp. complete business combination. Electriq Power, Inc., a provider of intelligent energy storage and management for homes and small businesses, and TLG Acquisition One Corp, completed their previously announced merger. The combined company will operate as Electriq Power Holdings, Inc. and its common stock and warrants started trading the New York Stock Exchange and NYSE American, respectively, under the ticker symbols “ELIQ” and “ELIQ WS,” respectively. The transaction (including pre-closing financings) generated over $45 million in equity for Electriq through private placements, PIPEs, loan conversions and non-redemptions, in addition to the previously announced project equity financing in excess of $300 million that was secured prior to the transaction. Read More (Business Wire)

Arrival and Kensington Capital Acquisition Corp. V agreed to terminate business combination agreement. Arrival (Nasdaq: ARVL), inventor of a unique new method of design and production of electric vehicles, and Kensington Capital Acquisition Corp. V (NYSE: KCGI.U), announced that both companies have agreed to terminate the business combination agreement initially signed April 6, 2023. Arrival intends to redirect its focus towards advancing other opportunities. The Company has engaged the services of TD Cowen and Teneo Financial Advisory to ensure the company's seamless transition and to pursue alternative avenues that will provide the company with additional liquidity. Read More (Globe Newswire)

NaturalShrimp Incorporated terminates merger agreement with Yotta Acquisition Corporation. NaturalShrimp Incorporated (OTCQB: SHMP), a Biotechnology Aquaculture Company that has developed and patented the first shrimp-focused commercially operational RAS (Recirculating Aquaculture System), has terminated its announced merger agreement with Yotta Acquisition Corporation and its wholly owned subsidiary, Yotta Merger Sub, Inc. The termination is based on Yotta’s inability to comply with the provision of its Amended and Restated Certificate of Incorporation that prohibits Yotta from consummating an initial business combination unless it has net tangible assets of at least $5,000,001 upon consummation of such initial business combination, in connection with the transactions contemplated with the Merger Agreement, which makes impossible the satisfaction of certain conditions to NaturalShrimp’s obligations to consummate, and the consummation of, such transactions. Read More (Business Wire)

|

Chart 7: SPAC Events – August 2023 (1/2) |

|

S. No |

Event Name |

Date |

Time |

|

1 |

ASPA Deadline extension vote |

8/7/2023 |

10AM EST |

|

2 |

GSD Deadline extension vote |

8/7/2023 |

10AM EST |

|

3 |

RRAC Deadline extension vote |

8/7/2023 |

11AM EST |

|

4 |

SZZL Deadline extension vote |

8/7/2023 |

12PM EST |

|

5 |

OXAC & Jet Token Merger Vote |

8/7/2023 |

4PM EST |

|

6 |

GBBK Deadline extension vote |

8/8/2023 |

10AM EST |

|

7 |

IRRX Deadline extension vote |

8/8/2023 |

10AM EST |

|

8 |

MTAC & TriSalus Life Sciences Merger Vote |

8/8/2023 |

11AM EST |

|

9 |

HHLA Deadline extension vote |

8/9/2023 |

9:30AM EST |

|

10 |

EMCG Deadline extension vote |

8/9/2023 |

11AM EST |

|

11 |

ENCP Deadline extension vote |

8/10/2023 |

8:30AM EST |

|

12 |

BSAQ & VinFast Merger Vote |

8/10/2023 |

9AM EST |

|

13 |

BYNO Deadline extension vote |

8/10/2023 |

10AM EST |

|

14 |

IVCA Deadline extension vote |

8/10/2023 |

10AM EST |

|

15 |

BITE Deadline extension vote |

8/10/2023 |

11AM EST |

|

16 |

FWAC & Mobile Infrastructure Merger Vote |

8/10/2023 |

11AM EST |

|

17 |

HAIA Deadline extension vote |

8/11/2023 |

9AM EST |

|

18 |

AURC & Better Merger Vote |

8/11/2023 |

9:30AM EST |

|

19 |

JGGC Deadline extension vote |

8/11/2023 |

10AM EST |

|

20 |

PICC Deadline extension vote |

8/11/2023 |

11AM EST |

|

21 |

DKDCA Deadline extension vote |

8/11/2023 |

1PM EST |

|

22 |

SGII Deadline extension vote |

8/14/2023 |

9:30AM EST |

|

23 |

PUCK Deadline extension vote |

8/14/2023 |

10AM EST |

|

24 |

PPHP Deadline extension vote |

8/15/2023 |

8AM EST |

|

25 |

PNAC & Noco-Noco Merger Vote |

8/15/2023 |

9AM EST |

|

26 |

KCGI Deadline extension vote |

8/15/2023 |

10AM EST |

|

27 |

MACA Deadline extension vote |

8/16/2023 |

9AM EST |

|

28 |

PPYA Deadline extension vote |

8/16/2023 |

11AM EST |

|

29 |

FTII Deadline extension vote |

8/17/2023 |

9AM EST |

|

30 |

DWAC Deadline extension vote |

8/17/2023 |

10AM EST |

|

31 |

KWAC Deadline extension vote |

8/17/2023 |

1PM EST |

|

32 |

FGMC & iCoreConnect Merger Vote |

8/18/2023 |

10AM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

Chart 7: SPAC Events – August 2023 (2/2)

|

S. No |

Event Name |

Date |

Time |

|

33 |

IFIN Deadline extension vote |

8/18/2023 |

12PM EST |

|

34 |

ZING Deadline extension vote |

8/21/2023 |

11AM EST |

|

35 |

FTII Deadline extension vote |

8/21/2023 |

1PM EST |

|

36 |

NFNT Deadline extension vote |

8/22/2023 |

9:30AM EST |

|

37 |

GLST Deadline extension vote |

8/22/2023 |

10AM EST |

|

38 |

FLAG & Calidi Biotherapeutics Merger Vote |

8/22/2023 |

10:30AM EST |

|

39 |

VHNA Deadline extension vote |

8/22/2023 |

11AM EST |

|

40 |

PEPL Deadline extension vote |

8/22/2023 |

4PM EST |

|

41 |

GFGD & ZeroNox Merger Vote |

8/23/2023 |

10AM EST |

|

42 |

CFFE & XBP Europe Holdings Merger Vote |

8/24/2023 |

10AM EST |

|

43 |

SWSS Deadline extension vote |

8/24/2023 |

11AM EST |

|

44 |

FLME Deadline extension vote |

8/29/2023 |

9AM EST |

|

45 |

BOCN Deadline extension vote |

8/29/2023 |

11AM EST |

|

46 |

CNDA Deadline extension vote |

8/29/2023 |

11AM EST |

|

47 |

GFOR & NKGen Biotech Merger Vote |

8/30/2023 |

10AM EST |

|

48 |

PIAI & Cheche Technology Merger Vote |

8/30/2023 |

10AM EST |

|

49 |

GGAA Deadline extension vote |

8/31/2023 |

9AM EST |

|

50 |

NSTC Deadline extension vote |

8/31/2023 |

11AM EST |

|

51 |

NSTD Deadline extension vote |

8/31/2023 |

11:30AM EST |

Source: Intro-act, SPAC Track, Boardroom Alpha

|

Chart 8: SPAC Activity by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

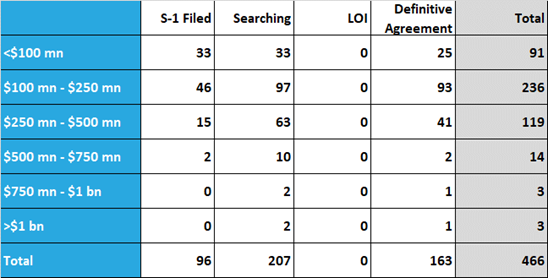

Chart 9: Current Status of the SPAC Universe |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 10: Current Status of SPAC Universe by Trust Size |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 11: SPAC Transactions by Year |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 12: Average SPAC IPO Size ($ Mn) |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 13: SPAC Transactions by Month (LTM) |

|

|

Source: Intro-act, Boardroom Alpha

|

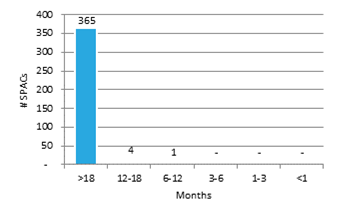

Chart 14: Time to Liquidation – By Volume |

|

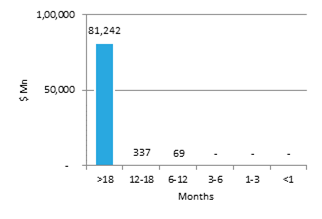

Chart 15: Time to Liquidation – By Trust Value |

|

|

|

|

Source: Intro-act, Boardroom Alpha

|

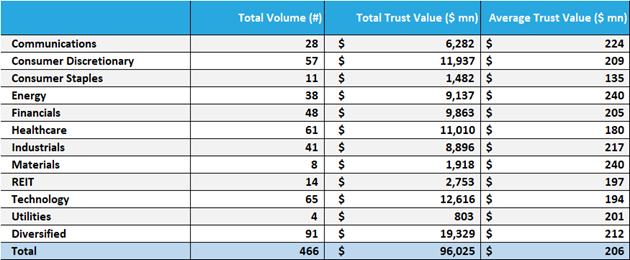

Chart 16: Active SPACs By Sector (As of Month Ending July 2023) |

|

|

Source: Intro-act, Boardroom Alpha

|

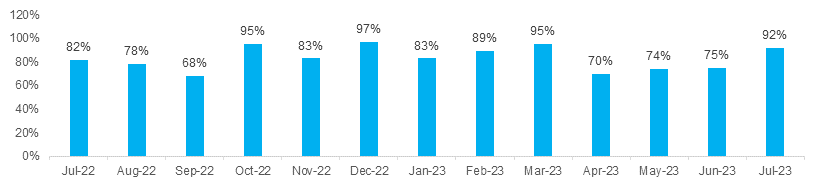

Chart 17: Average Redemption Rate by Month |

|

|

Source: Intro-act, Boardroom Alpha

|

Chart 18: SPAC Redemption Detail – July 2023 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 19: Monthly SPAC Activity – July 2023 |

|

|

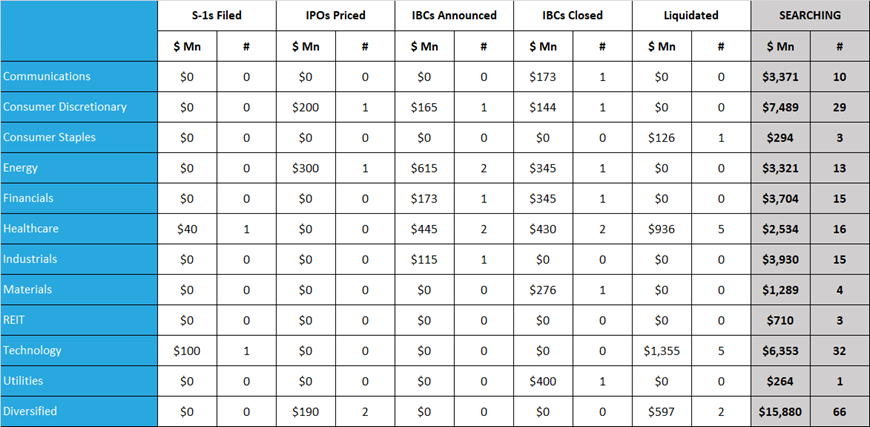

Source: Intro-act, Boardroom Alpha. Searching figures ($Mn and Count) are as of month end.

|

Chart 20: SPAC IBC Announcements by Target Sector – July 2023 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

The SPAC and New Issue ETF (SPCX). SPCX gives investors exposure to a broad portfolio of SPACs with the familiar attributes of an exchange traded fund’s diversity, tax efficiency and liquidity. SPCX is the first actively managed SPAC ETF. Why active? As the SPAC market is rapidly evolving, we believe that the portfolio management approach should equally reflect the dynamic nature of this burgeoning capital-raising alternative. This is no place for a rigid rules-based index strategy.

|

Chart 21: SPCX Summary Data |

|

Chart 22: SPCX Top 10 Holdings |

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

Source: Intro-act, ETF.com. Data as of 7/31/23.

|

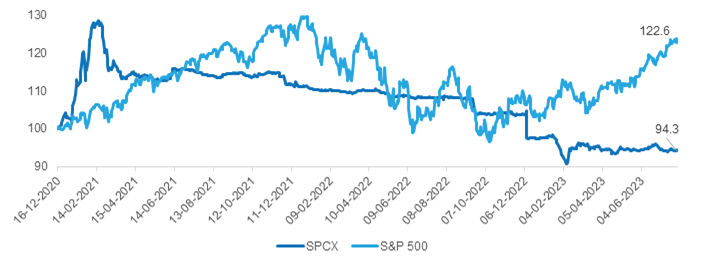

Chart 23: SPCX Performance |

|

|

Source: Intro-act, Yahoo! Finance. Data as of 7/31/23.

|

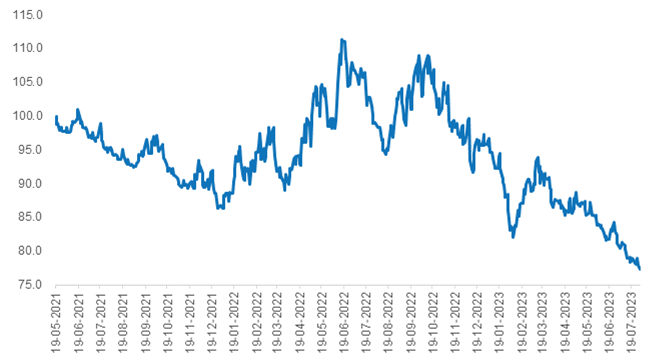

Chart 24: Relative-SPAC Index vs Russell 3000 |

|

|

Source: Intro-act, FactSet

|

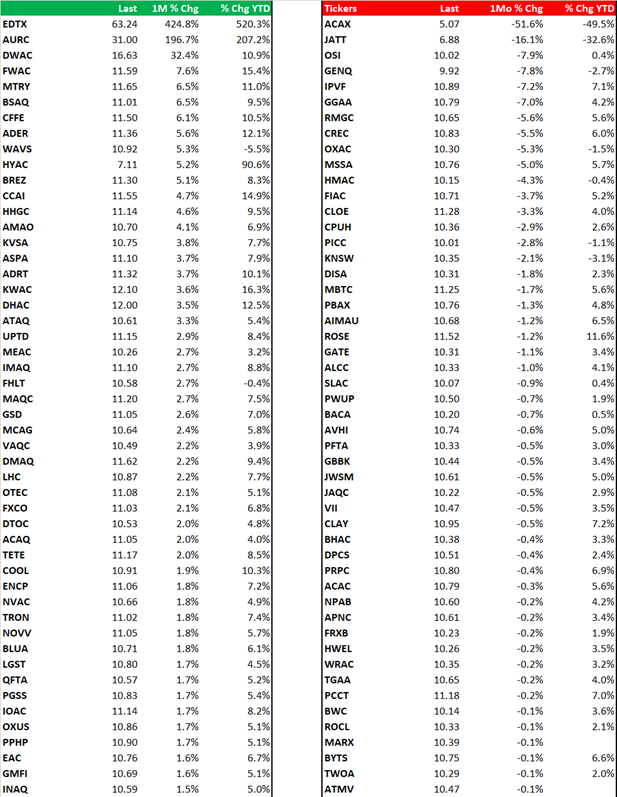

Chart 25: Gainers and Losers in the Broader SPAC Universe (% Change) |

|

|

Source: Intro-act, FactSet

|

Chart 26: SPAC IPO Pricings by Sector – July 2023 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 27: SPAC S-1 Filings by Sector – July 2023 |

||||||||||||||||||

|

Source: Intro-act, Boardroom Alpha

|

Chart 28: SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 29: DE-SPAC Institutional Owners League (Current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, 13F Filings

|

Chart 30: SPAC Underwriter League (YTD As of July 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Bookrunner Volume ($ Mn) is based on the total amount of the offering sold, including over-allotment. Full credit is awarded to the sole book-runner or split equally among joint book-runners.

|

Chart 31: Top De-SPAC Advisors (YTD As of July 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Advisor credit is shared equally among all advisors on a given deal, as a proportion of the enterprise value of the target company acquired by the SPAC. Firms with multiple advisory roles receive credit for each role.

|

Chart 32: SPAC Legal League (YTD As of July 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research. Note: Credit for Volume ($ Mn) is awarded to both Issuer and Underwriter Counsel.

|

Chart 33: SPAC Auditor League (YTD As of July 2023 End) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: Intro-act, SPAC Research

|

Chart 34: ICR – The Leading SPAC Communications and Capital Markets Advisor |

|

113 Transactions / $267 Billion in Transaction Value Since 2021

|

Source: Intro-act, ICR. Announced SPAC transactions since 2021, All Announcements not shown. Data as of April 2022.

Analyst Certification

I, Peter Wright, certify that the views expressed in the research report accurately reflect my personal views about the subject securities or issues. I also do not receive direct or indirect compensation based on my recommendations or views.

Intro-act, Inc. (Intro-act) issued this report and may seek fees for the assistance with investor targeting, access, and further investor preparation services. Intro-act, Inc. will not seek renumeration for any investment banking service or investment advice.

Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources who are believed to be reliable. However, the issuer and related parties, as well as Intro-act, do not guarantee the accuracy or completeness of this report, and have not sought for this information to be independently verified. Opinions contained in this report represent those of the Intro-act analysts at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, and estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties, and other factors that may cause the actual results, performance, or achievements of their subject matter to be materially different from current expectations.

Exclusion of Liability: To the fullest extent allowed by law, Intro-act, Inc. shall not be liable for any direct, indirect, or consequential losses, loss of profits, damages, or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this note.

No personalized advice: The information that we provide should not be construed in any manner whatsoever as personalized advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Intro-act’s solicitation to affect, or attempt to affect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors.

Investment in securities mentioned: Intro-act has a restrictive policy relating to personal dealing and conflicts of interest. Intro-act, Inc. does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees, and contractors of Intro-act may have a position in any or related securities mentioned in this report, subject to Intro-act’s policies on personal dealing and conflicts of interest.

Copyright: Copyright 2023 Intro-act, Inc. (Intro-act).

Intro-act is not registered as an investment adviser with the Securities and Exchange Commission. Intro-act relies upon the “publishers’ exclusion” from the definition of investment adviser under Section 202(a) (11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Intro-act does not offer or provide personal advice, and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell, or hold that or any security, or that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.